Finance processes to automate in an SME: which to control first

Published on :

April 20, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

The conversation around finance automation for SMEs tends to start in the wrong place. Technology vendors lead with capability, here is everything you can automate, and finance leaders respond by trying to automate everything at once. Six months later, the automation is partially working, the team is managing new exception queues on top of old manual workflows, and the ROI is unclear.

The right question for an SME finance team is not "what can we automate?" It is "what should we control first?" These are different questions with different answers, and sequencing them correctly is what separates SMEs that generate real efficiency gains from those that add complexity without reducing effort.

This article maps the sequencing logic: which finance processes carry the most risk and the most immediate financial consequence, why control is a prerequisite for effective automation, and what the practical implementation sequence looks like for a finance team of two to ten people.

Why "automate everything" is the wrong starting point for SMEs

Large enterprises can afford to automate broadly and manage the transition gradually, because they have the teams, the IT resources, and the financial reserves to absorb the inefficiencies of a poorly sequenced rollout. SMEs typically have none of these buffers.

An SME finance team of three people managing 300 invoices per month and a multi-bank cash position does not have capacity to manage a failed automation implementation alongside its existing workload. When an automation project introduces more exception handling than it eliminates, because the underlying data wasn't controlled before automation was layered on top, the team faces a worse situation than before it started.

The root cause of most failed SME finance automation projects is not the technology. It is the absence of control. Automation amplifies what it processes. When the underlying processes are already accurate and consistently applied, automation reliably accelerates them. When they are inconsistent, error-prone, or reliant on tribal knowledge, automation amplifies those inconsistencies at machine speed, producing more errors, more exceptions, and more manual cleanup than the manual process it replaced.

Control before automation is not a sequencing preference, it is a technical requirement. An AI agent that validates invoices against contracted prices can only work reliably if the contracted prices are captured in a reference system, if the invoices arrive in a consistent format, and if the approval workflow has defined exception paths. None of those conditions are automatic. They are the product of controlled processes applied consistently over time.

For SMEs, the sequencing question matters more than for any other size of organisation, because the margin for error is narrower and the cost of a failed rollout is proportionally higher.

The SME finance risk map: where losses concentrate before any automation

Before identifying what to control and in what order, it is worth mapping where uncontrolled finance processes actually cost SMEs money. The losses are not evenly distributed, they concentrate in three areas.

Supplier invoicing errors account for the largest category of preventable financial loss for most SMEs. Price deviations against contracted rates, duplicate invoices, invoices without corresponding purchase orders, and invoices processed without delivery confirmation collectively represent a systematic overpayment risk that compounds with supplier count and transaction volume. A business processing 300 invoices per month from 40 active suppliers with average 3-5% error rates is leaking thousands of euros monthly in overcharges that no one is systematically catching.

La Nouvelle Garde, a multi-site hospitality group, intercepted €28,000 in fraudulent invoices within the first months after deploying systematic invoice control. Vivason identified €180,000 in annual supplier overcharges that had been passing undetected through a manual review process. These are not exceptional cases; they are what systematic measurement reveals in most businesses that have been relying on spot-check AP reviews.

Cash position inaccuracy is the second concentration point. When bank reconciliation runs monthly rather than daily, the cash position used for daily management decisions, payment timing, purchasing commitments, short-term financing decisions, is based on a balance that may be days or weeks out of date. For an SME where cash management directly affects growth decisions, operating on a stale cash position is a risk that is easy to underestimate until it produces a decision that damages the business.

Revenue and receivables gaps, the third area, represent money owed to the business that isn't being systematically collected. For businesses with recurring contracts, the gap between contracted revenue and actually invoiced amounts can accumulate silently over months. For businesses with high invoice volumes, the receivables position used for cash forecasting may not reflect recent customer payments that haven't yet been reconciled. These gaps don't produce immediate cash losses, but they distort the management data used to make investment and hiring decisions.

These three areas share a common characteristic: they are all worse than they appear to be before they are measured. The business that has never run systematic supplier invoice validation does not know its actual error rate. The business that reconciles bank accounts monthly does not know how often its intra-month cash position decisions were based on inaccurate data. Measurement and control are the prerequisite not just to fixing these problems, but to understanding their actual scale.

The control-first sequence: 5 processes in priority order

The following sequence applies the control-before-automation principle to the five finance processes where SMEs consistently generate the most immediate returns. Each process is ordered by the combination of: financial impact of errors, ease of establishing control, and the degree to which control enables subsequent automation.

Process 1: supplier invoice validation (highest priority, highest financial impact)

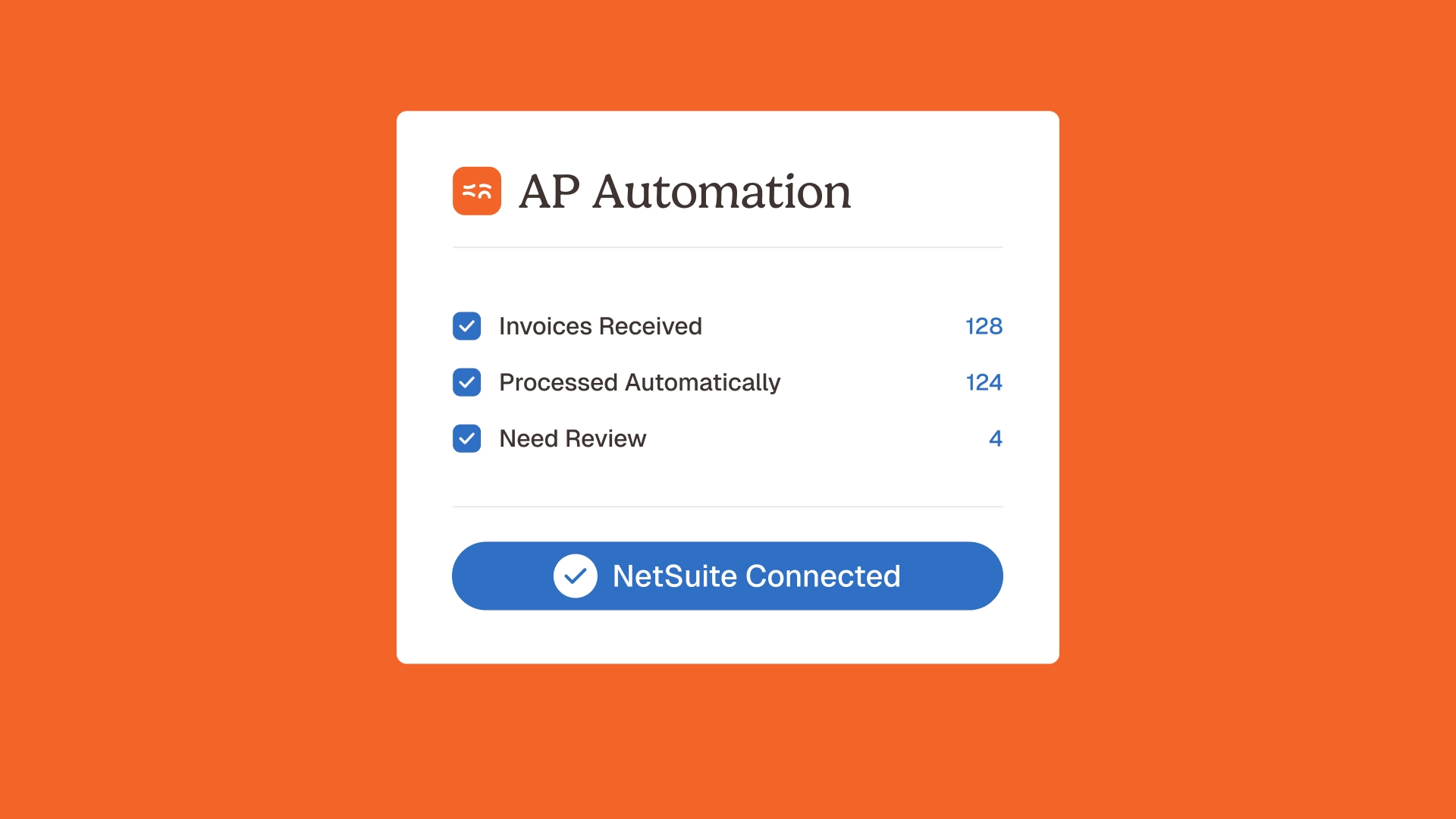

The first process to control is supplier invoice validation: the systematic check of every incoming invoice against contracted prices, purchase orders, and delivery confirmations before payment approval.

The reason this is the highest priority is direct: it is the process where uncontrolled errors translate most immediately into cash losses. A duplicate invoice paid, a price deviation not caught, an invoice approved without delivery confirmation, each produces a financial loss at the moment of payment that is expensive to recover.

Control means establishing three things before automation is considered: a reference system for contracted prices (not necessarily a sophisticated contract management tool, a maintained spreadsheet of supplier rates is sufficient as a starting point), a defined approval process for invoices that includes a price comparison step, and a documented exception path for invoices that don't match expected values.

Once those three foundations exist, supplier invoice automation can be deployed on top, with AI agents validating every invoice against the contracted price reference, detecting duplicates across the full population, and flagging exceptions for the approval workflow. Phacet's supplier billing control agent implements this layer. But the agent is more effective, and requires significantly less configuration, when the underlying contracted price reference is maintained and the approval workflow is defined before deployment.

For more on the specific controls that supplier invoice validation requires, see the invoice control before payment article and the detailed treatment of pre-payment controls that apply at each stage.

Process 2: bank reconciliation (highest frequency, fastest to control and automate)

The second process to control is bank reconciliation, the daily matching of bank transactions to the ERP or accounting system records. This should be the second priority not because it generates the largest absolute losses, but because it is the fastest to bring under control and the process where the transition from manual to automated delivers the most immediate time savings.

Control, in this context, means establishing a consistent daily routine: bank transactions are imported, matched against recorded transactions, and unmatched items are reviewed and resolved on the day they appear. This sounds simple and is, for most SMEs, achievable within days rather than weeks. The barrier is usually not the process itself but the habit, most SME finance teams have drifted into a monthly reconciliation cadence because they never had a tool that made daily reconciliation viable.

Once the daily reconciliation discipline exists, automation can take over the matching logic, identifying which bank transactions correspond to which ERP records, categorising the matches, and surfacing only the genuinely ambiguous items for human review. The bank reconciliation automation agent processes every transaction as it settles, maintaining a continuously validated cash position rather than one that is thirty days stale. The agent for reconciling bank transactions implements this pattern, processing the daily settlement window and surfacing unmatched items while context is still current.

The time saving is significant: for a typical SME finance team, daily bank reconciliation currently consumes two to four hours at month-end. With automated daily matching, that task reduces to fifteen to twenty minutes of reviewing genuinely ambiguous items, a 70-80% reduction in reconciliation time.

Process 3: accounting inbox management (highest volume of manual effort, first to automate from day one)

The third process, managing the accounting inbox — is distinctive because it is one of the few processes where automation does not require an existing control foundation to be effective. The accounting inbox (email receipts of supplier invoices, scanned documents, expense claims) is a volume problem, not a control problem: the manual work of reading, classifying, routing, and posting documents is simply high enough in volume that it consumes a disproportionate share of a lean finance team's time.

La Nouvelle Garde reduced their accounting inbox processing from 1,794 manual operations per year to near-zero after deploying Phacet's accounting inbox agent. For a team of two managing 300+ documents per month, this represents a meaningful capacity recovery, time that had been consumed by triage and data entry is available for higher-value work.

Control does apply here, but in a different sense: the relevant control question is not "are we catching errors?" but "are we routing documents consistently?" The automation works best when the routing rules are defined (which document types go to which workflow, which suppliers are in which approval tier) and when the exception paths are specified (what happens when a document arrives without a PO reference). Defining these rules before deployment is the "control first" requirement for this process, and it is achievable in a day or two, not weeks.

The accounting inbox agent handles extraction, classification, and routing automatically, with intelligent data extraction applied to every document regardless of format or source. The exception-based finance review model routes only the genuinely ambiguous documents for human review, typically 5-10% of total volume.

Process 4: cash flow labelling and treasury reporting (highest management decision value)

The fourth process to control and automate is cash flow labelling: the systematic classification of bank transactions into cash flow categories for treasury reporting and cash forecasting. For most SMEs, this is currently a manual task at month-end, someone works through the bank statement and assigns categories before the cash flow statement can be prepared.

The control question here is classification consistency: does "marketing spend" mean the same thing across all entities, all periods, and all people who do the classification? Inconsistent classification produces cash flow reports that are arithmetically accurate but economically misleading, the categories don't mean the same thing from one period to the next, so trends are unreliable.

Establishing a defined classification scheme, a maintained list of categories with clear rules for which transaction types belong in each, is the control foundation. Once the scheme is defined, cash flow automation through the cash movement labelling agent applies it consistently across every transaction, every period, producing a treasury dashboard that is both accurate and comparable over time. The agent learns from the classification rules and from the edge-case decisions made by the finance team, improving its accuracy progressively.

For SaaS and subscription businesses specifically, the supplier transaction labelling agent adds a further layer, systematically classifying supplier spend by cost category for margin tracking, addressing the specific pain point identified in sales calls: "we can never tell which supplier costs are in which category without spending half a day re-labelling."

Process 5: receivables and customer cash-in reconciliation (closing the revenue loop)

The fifth process is receivables management: the systematic tracking and reconciliation of customer payments against outstanding invoices. For businesses where the revenue side of the ledger is manually managed, matching incoming bank credits to specific customer invoices by hand — this is one of the largest time consumers in the finance function and one of the most common sources of revenue leakage (payments received but not correctly applied, disputed invoices not followed up, overdue invoices not escalated).

Control means establishing a defined receivables process: invoices are issued consistently, payment terms are tracked against specific due dates, and incoming customer payments are matched to the relevant invoice records on the day they arrive. For many SMEs, this process is managed informally, the finance team knows from memory which customers owe what — which is sustainable at low invoice volumes but breaks down as the business scales.

The customer cash-in reconciliation agent automates the matching logic: incoming bank credits are compared against outstanding invoice records, matched where possible, and flagged for manual review where the match is ambiguous (partial payments, consolidated remittances, disputed items). The tracking customer payments agent ensures that no payment is received without being applied to the correct invoice, closing the revenue loop that informal receivables management often leaves open.

For more on automating the full order-to-cash cycle, see the accounts receivable automation article, which covers the end-to-end workflow from invoice issuance to payment reconciliation.

The implementation reality: what SMEs need before starting

Beyond the five-process sequence, there are three practical preconditions that determine whether an SME finance automation rollout will succeed.

Supplier master data that is accurate and maintained. Invoice validation and supplier reconciliation both depend on a clean supplier reference: correct names, correct IBANs, current contracted prices. For most SMEs, this master data exists in fragmented form across the accounting system, a spreadsheet, and the collective memory of the finance team. Dedicating two to three days to cleaning and consolidating this reference before deploying invoice validation is not optional, it is what makes the validation logic work correctly from day one.

A defined chart of accounts with consistent classification rules. Cash flow labelling and accounting data standardisation both require a classification scheme that is consistently applied. If the current chart of accounts has categories that overlap or are applied inconsistently, defining a clean version before automation deployment prevents the automation from systematising the inconsistency rather than correcting it.

Defined exception paths for each process. Every automated process will produce exceptions, invoices that don't match, bank items that can't be automatically matched, documents that don't fit a known category. Defining what happens to each exception type before deployment, which team member reviews it, what information they need, what the resolution options are, is what prevents exception queues from accumulating into backlogs that consume more time than the automation saves.

None of these preconditions require months of preparation. Each can typically be addressed in one to two weeks of focused work before deployment begins. Phacet's no-code automation platform and the implementation support that comes with it are designed to make this preparation practical for a two-to-three person finance team without dedicated IT resource. The no-code finance automation article covers the implementation model in detail, and the AI automation ROI in finance piece covers how to measure the returns at each stage.

What the sequence produces: from controlled to automated in 4 months

Applied in order, the five-process sequence produces a predictable transformation arc for an SME finance team.

Month 1: Supplier invoice validation and bank reconciliation are deployed. The finance team begins measuring its actual invoice error rate for the first time, typically 3-7% across the supplier population. Duplicate invoices and price deviations are intercepted before payment. Bank reconciliation moves from a monthly two-hour task to a daily fifteen-minute review. Close preparation time begins to decrease as the bank reconciliation backlog disappears.

Month 2: The accounting inbox agent is deployed. Document triage and routing disappear from the finance team's daily workload. The team's available capacity increases by 20-30%, hours previously consumed by email management and manual document classification become available for exception resolution and analysis work.

Month 3: Cash flow labelling and treasury reporting are automated. The management cash flow dashboard becomes a daily tool rather than a monthly preparation exercise. Intra-month cash position decisions are based on a continuously validated position rather than a thirty-day-old snapshot.

Month 4: Receivables reconciliation is automated. The revenue loop closes: every customer payment is applied to the correct invoice on the day it arrives. The receivables position used for cash forecasting is accurate in real time, not assembled manually at month-end.

By month four, the finance team is spending its time on exception resolution, analysis, and strategic support, not on data entry, document triage, or reconciliation backlog management. The close cycle has shortened. The error rate has measurably decreased. The management data feeding business decisions is more accurate and more current than it has ever been.

This is the practical outcome of control before automation applied in the right sequence. Not a technology transformation, an operational upgrade, implemented in stages, producing compounding returns at each step.

FAQ

Which finance process should an SME automate first?

The first process to control, and then automate, is supplier invoice validation. It carries the highest immediate financial impact: uncontrolled errors produce cash losses at the point of payment, and those losses are expensive to recover. The control foundation (a maintained contracted price reference and a defined approval process) takes one to two weeks to establish. The automation layer, once deployed, validates every invoice before it reaches the payment queue, typically reducing the invoice error rate from 3-7% to under 2% within the first period.

Can SMEs automate finance processes without an IT team?

Yes. Phacet's no-code automation platform is specifically designed for finance teams without dedicated IT resource. Each agent connects to existing accounting systems, banking portals, and invoice management tools through standard integrations, configured via a no-code interface rather than custom development. Typical deployment time per process is one to three weeks. No ERP modifications or developer resource are required.

What is the difference between controlling a finance process and automating it?

Controlling a process means establishing that it produces consistent, accurate outputs under human management, with defined rules, maintained reference data, and documented exception paths. Automating a process means replacing or augmenting the human execution with software that applies the same rules at higher speed and volume. Control is a prerequisite for automation: an automated process without control foundations amplifies inconsistencies rather than eliminating them. For SMEs, the practical sequence is always control first, then automate, because the automation ROI depends on the quality of the underlying process.

How many invoices per month does it take to justify finance automation for an SME?

There is no minimum invoice volume that makes automation economically unjustifiable, the ROI calculation also includes the value of the errors prevented, not just the time saved on processing. An SME processing 100 invoices per month with a 5% error rate at an average invoice value of €500 is losing €2,500 per month to undetected errors. That is well above the cost of systematic invoice control, regardless of the processing time saved. At 300 invoices per month, both the error prevention and the time savings typically produce payback in the first quarter after deployment.

How does finance automation affect an SME finance team's daily work?

For a team of two to five people, finance automation shifts work from volume tasks (document triage, reconciliation scanning, manual posting) to judgment tasks (exception resolution, supplier dispute management, management analysis). The volume of work decreases; the complexity and value of the remaining work increases. Teams consistently report that the time previously consumed by invoice processing and bank reconciliation, typically 40-60% of total finance team hours, is freed for work that was previously crowded out by the operational backlog.

Does automation work differently for a hospitality SME versus a tech SME?

The process priorities are similar, but the specific configuration of the automation differs by industry. For hospitality groups (restaurants, hotels), supplier invoice validation is especially critical because of high invoice volumes, frequent price changes, and mercuriale pricing complexity. For tech/SaaS SMEs, the priority mix shifts: ARR reconciliation between billing system, CRM, and accounting system is typically the highest-value automation target, followed by supplier invoicing and bank reconciliation. Phacet's agents are configured to the specific data flows and reference systems relevant to each industry context, the underlying principles are the same, but the implementation details differ.

Control first, then automate, the sequence that makes returns permanent

The SMEs that generate sustained returns from finance automation share a consistent characteristic: they built control before they built automation. Their invoice error rates were measured before agents were deployed. Their bank reconciliation was running consistently before it was automated. Their classification schemes were defined before labelling was automated.

This sequencing produces automation that works reliably from day one, because the process it automates is already under control, and the automation is accelerating a known, consistent workflow rather than being asked to compensate for an inconsistent one.

Phacet's approach to SME finance automation starts from this principle. The five agents that address the highest-priority processes, supplier invoice control, bank reconciliation, accounting inbox management, cash flow labelling, and customer payment reconciliation, are deployed in sequence, with each stage building on the control foundations established by the previous one. The result is a finance function that is not just more automated but genuinely more reliable, one that can support the business decisions that determine whether the SME grows or stalls. Book a demo to map which of your processes are ready to automate today and which need a control foundation first.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.