Cost center invoice validation: how finance teams verify coding before ERP entry

Published on :

November 5, 2025

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

A finance team running a multi-site operation processes invoices through an AI-powered AP workflow. Every invoice gets a GL account, a cost center, and a project code assigned, often with high field-level accuracy. Yet a meaningful share of those invoices posts to the wrong cost center, and the corrections only surface during budget reviews weeks later, when a site director asks why their P&L is showing a charge they never approved.

The gap is not the coding step. The coding step works. The gap is that assigning a cost center is not the same as validating it. AP tools and modern OCR engines do the first job well, but most pipelines treat the second job as a manual review at approval time, by which point the coding is already in the ERP queue and a manual correction is the only recourse. Cost center invoice validation runs between the two: after the code is proposed, before the invoice is posted, and against criteria the coding engine does not check on its own.

This article maps the six controls that should run between cost-center assignment and ERP entry: existence in the analytical mapping table, status check (open, closed, restricted), authorization of the GL × cost-center × supplier combination, budget availability against current period spend, multi-line allocation consistency, and audit trail capture. Each control answers a different question. Together they turn cost-center assignment from a coding decision into a validated posting.

Why cost center coding is not cost center validation

The default AP pipeline treats cost-center assignment as a single step: an AI engine looks at the supplier, the line description, and the historical coding patterns, then proposes a cost center. The approver glances at it, approves the invoice, the entry posts to the ERP.

That sequence skips a critical layer. A cost center that is plausible (an AI engine can predict it from supplier history with high accuracy) is not necessarily valid (the cost center exists in the current chart, is open for the period, is authorized for this expense type, and has budget remaining). The plausibility check answers "what cost center would this normally be coded to?" The validity check answers "should this cost center receive this charge right now?"

Confusing the two has three downstream consequences. First, budget variances surface late, because the invoice has already posted before anyone checks if the cost center had budget left. Second, closed or restricted cost centers occasionally receive charges they shouldn't (an acquisition that's being wound down, a project that was budget-frozen). Third, the chart of accounts drifts over time: invoices keep flowing to a cost-center code that no longer reflects the current organizational structure, and reporting becomes progressively less reliable.

The shift this article proposes: stop treating cost-center coding as a "predict and post" loop. Treat it as a predict, validate, post loop, with the validation layer running on every invoice before it reaches the ERP.

The 6 controls that validate a cost center before posting

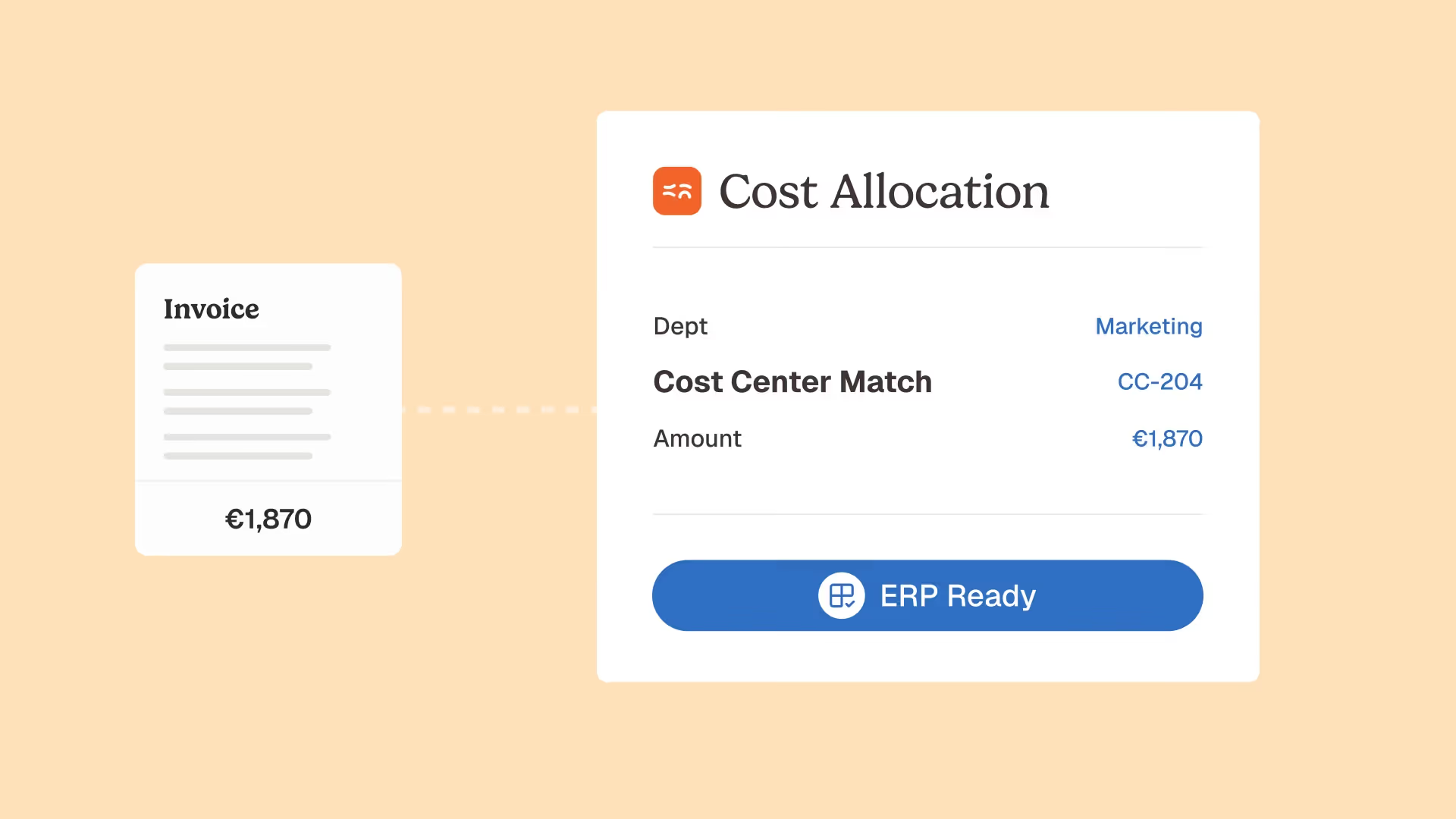

1. Existence check against the analytical mapping table

The first control is structural: does this cost center exist in the current chart of accounts? Most ERPs reject a posting with an unknown cost center, but the error surfaces at the ERP boundary, after the invoice has been approved and the rejection forces a manual rework. The right control runs earlier, against the analytical mapping table that holds the authoritative chart, so the invoice never leaves AP with a broken code.

The mapping table is not a static reference. It changes when entities are added, sites are reorganized, projects are closed. The validation control reads the current state of the table at the moment the invoice is built, not a cached version from last quarter.

2. Status check (open, closed, restricted)

The second control is temporal: is the cost center currently open to receive charges? A cost center can exist in the chart and still be closed for one of three reasons: the period is locked (typical at month-end), the project is finished and the code is being phased out, or the cost center is restricted to a specific budget owner or expense category.

This control catches the long tail of postings that ERPs allow but auditors flag later: charges to a closed-period cost center that should have been accrued instead, charges to a winding-down entity that should have been redirected. The status flag belongs in the cost-center master, and the validation control reads it before posting.

3. Authorization of the GL × cost-center × supplier combination

The third control is combinatorial: not every cost center can receive every type of charge. A marketing cost center should not be receiving raw-material invoices. A site-operations cost center should not be receiving consulting fees. The chart of accounts typically encodes these rules implicitly (through naming conventions or controller knowledge), but the validation layer needs to make them explicit.

The pattern: a matrix of allowed combinations (GL account × cost center × supplier category) lives alongside the mapping table. When the invoice arrives, the validation control checks the proposed combination against the matrix. A disallowed combination doesn't necessarily block the invoice. It routes it to a budget owner for explicit override, with the deviation logged in the audit trail. This is the difference between "the AI predicted this code" and "this code was approved for this charge."

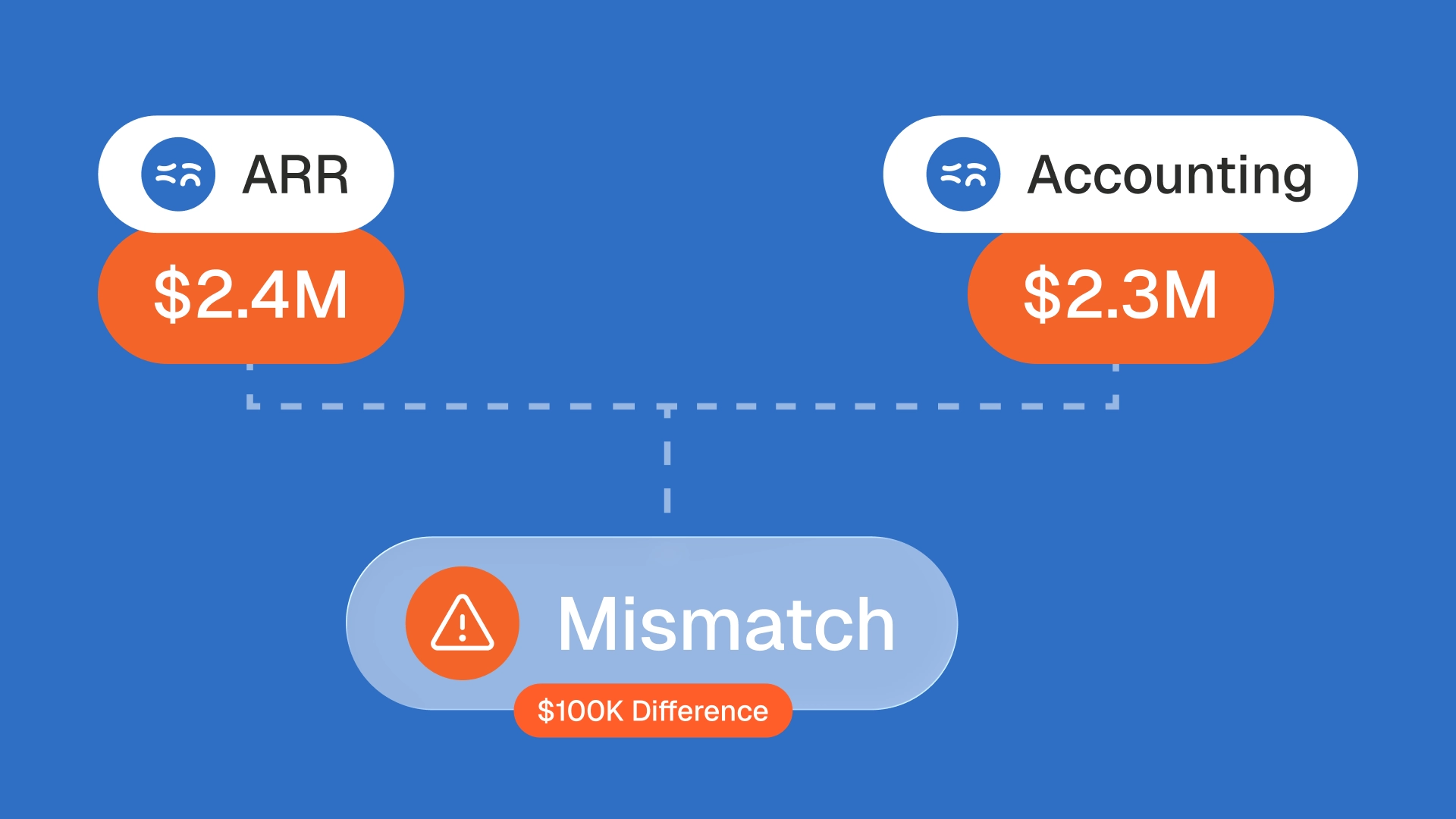

4. Budget availability against current period spend

The fourth control is the most operationally visible: does the cost center have budget remaining for this charge? Without this check, invoices flow into the ERP regardless of budget status, and overspend surfaces only when someone runs a budget-vs-actual report at month-end, by which point the money is already committed.

The right control runs at validation time: the track budget vs actual variances agent compares the invoiced amount against the remaining budget for the cost center, the period, and the GL category. If the invoice would push the cost center into overspend, the validation routes it to the budget owner for arbitration before posting. The invoice still gets paid if the owner approves the variance. But the variance is now an explicit decision, not a silent fact discovered later.

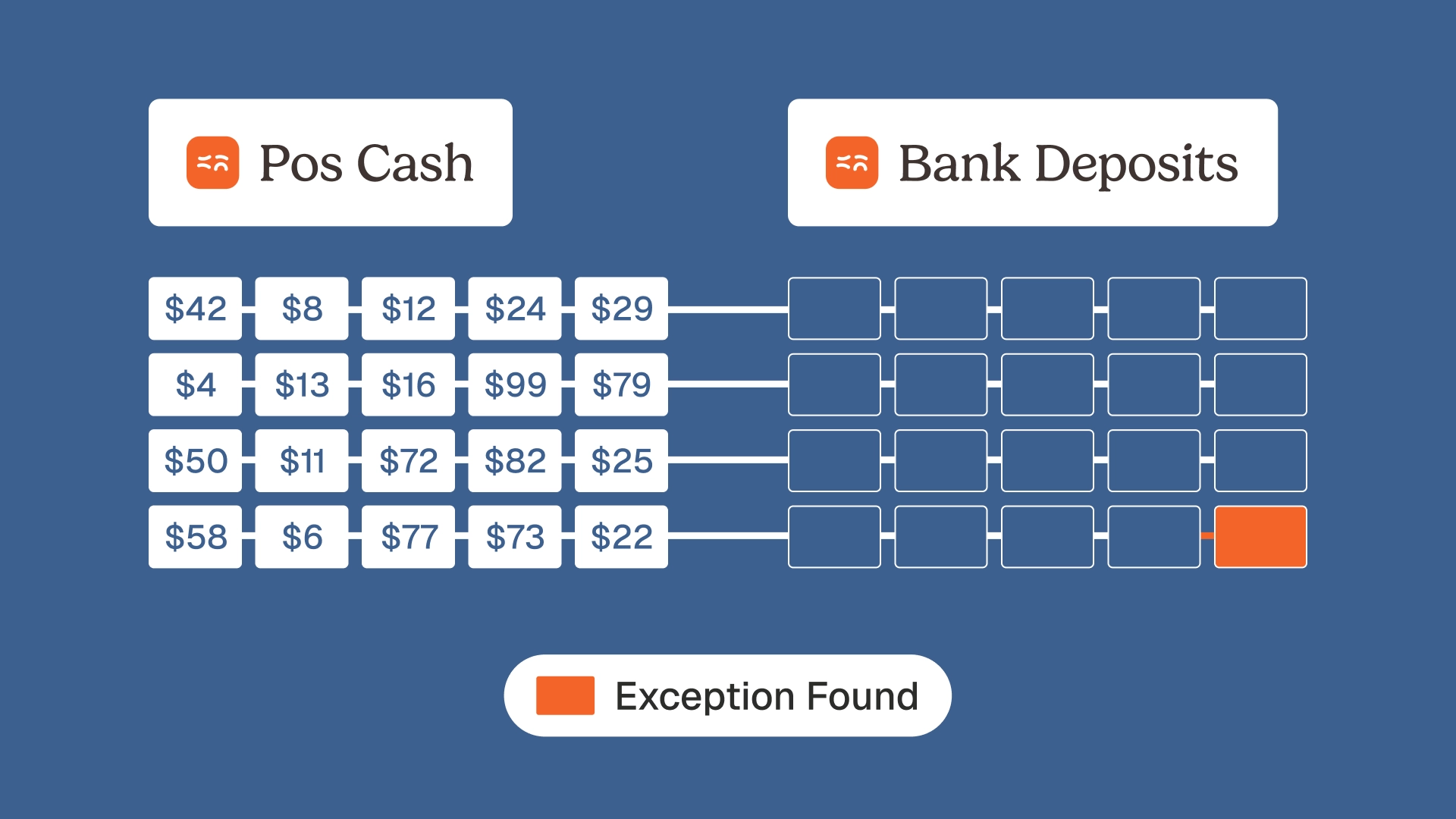

5. Multi-line allocation consistency

The fifth control applies to invoices that split across multiple cost centers (shared services invoices, multi-site invoices, project allocations). A single invoice for office rent may need to be allocated across three departments at fixed percentages. A consulting invoice may need to split across two projects based on hours worked.

The validation control checks two things: the allocation rules exist for this supplier or expense type, and the split percentages sum to 100% across the declared cost centers. Both checks fail in production more often than expected: a supplier was onboarded without an allocation rule, a rule was set up but the percentages were typed wrong (a common error: 33% + 33% + 33% = 99%, leaving 1% unallocated). The control catches both before the invoice posts.

6. Audit trail capture of every cost-center decision

The final control is meta: every cost-center assignment, every authorization override, every budget breach, every multi-line allocation must be timestamped and stored. The decisions themselves need to be inspectable, not just the postings.

This matters for three reasons. Auditors want evidence that controls ran, not just that the right code ended up in the ERP. Controllers need a paper trail when a budget owner contests a charge three months later. And the validation pipeline needs telemetry to improve: which cost centers fail validation most often, which suppliers generate the most overrides, which combinations should be added to the allowed matrix. A native audit trail is what makes the validation layer inspectable rather than opaque.

Why most pipelines skip cost-center validation

Every CFO recognizes the controls listed above. Most AP pipelines run two or three of them, rarely all six. Three structural reasons:

The coding step feels like the validation step. Modern AI coding engines (Rillion, HighRadius, Centime, AppZen, Hypatos) report 90%+ field-level accuracy on GL and cost-center assignment. That accuracy is real, but it answers "did the engine predict the right code?" not "should the invoice be allowed to post to that code?" Teams treat the accuracy metric as proof of validation, when it only proves prediction.

Budget data lives in a different system from AP. AP tools know the invoice. ERP tools know the budget. The integration between them is usually one-way (AP pushes the posting, ERP records it), so the AP layer doesn't have real-time budget visibility at the moment of coding. Budget checks happen at month-end, in a separate report, after the postings are already in. The right architecture pulls budget context into AP at coding time, not after.

The analytical mapping table is treated as a configuration, not a control. The chart of accounts and cost-center master are usually maintained as a setup artifact: someone updates them quarterly, the AP tool reads them, and that's the end of it. But cost-center authorization, status flags, and allowed combinations need active maintenance and active enforcement. Treating the mapping table as a controllable surface (with explicit rules, owners, and override logging) is what turns it from a reference list into a pre-ERP validation layer.

How AI agents make cost-center validation run on every invoice

Rule-based automation handles the first two controls (existence and status) reasonably well, since they are simple lookups. It struggles on the others. Authorization rules are usually semi-formal and hard to encode exhaustively. Budget checks require real-time integration. Multi-line allocations require context that rule engines don't carry across invoices.

AI agents close the gap with the Phacet architecture: each agent structures the input (extracts supplier, GL, cost center, amount, line allocations), controls against a reference (mapping table, allowed combinations, budget remaining), and exposes its reasoning with a confidence score. Every step is timestamped in a native audit trail, which makes the validation layer reliable, controllable, and auditable by design.

The most relevant agents for cost-center validation:

- The accounting inbox agent handles intake and proposes the initial coding.

- The standardize and reclassify agent encodes the GL × cost-center mapping rules and applies them consistently across entities.

- The analytical mapping table agent maintains the authoritative reference: which cost centers exist, which are open, which combinations are allowed, which owners receive overrides.

- The budget vs actual agent brings real-time budget context into the validation step, so the invoice gets validated against remaining budget before it posts.

- The control invoices against contract terms agent feeds the multi-line allocation logic for recurring contracts (rent splits, shared service allocations).

Each agent surfaces its results in Tables (a tabular view where each row is an invoice with its proposed coding, the validation outcomes per control, and any flagged exceptions). When the agent isn't certain, the AI Match component surfaces the proposed coding with its reasoning so a controller can validate in the Vue Détail view. The 40+ agents in the catalog were built across 100+ real deployments, which means each one reflects an actual control problem finance teams face at multi-entity scale.

What cost-center validation looks like in production

Three customer outcomes show what changes when the six controls run together:

The French Bastards, a Parisian artisanal bakery group, absorbed the doubling of their boutique count from 7 to 14 sites without adding finance headcount. Multi-site cost-center allocation is precisely the workflow that breaks first at this kind of scale: each new boutique adds a cost center, and rent, utilities, and shared services need to allocate consistently across them. As Marie-Céline, Head of Finance, puts it: "On voit Phacet comme un vrai partenaire. Vous nous poussez des idées auxquelles je n'aurais pas pensé." The cost-center validation layer is what allowed the team to scale entity count without scaling control effort proportionally.

Astotel operates across 18 hotels, each with its own cost-center structure and operational categories. The 5,000€ per year recovered on a single supplier through the supplier billing control agent is the headline number, but the underlying enabler is the validated cost-center coding that makes the comparison possible in the first place. Valérie, Directrice Achats: "Je gagne jusqu'à deux jours par mois, et je repère des erreurs que je n'aurais jamais vues seule." The errors she catches surface only because the cost-center coding is consistent and validated across all 18 sites.

La Nouvelle Garde, a group of 10 Parisian brasseries, eliminated roughly 1,800 manual operations per year and intercepted 28,000€ of attempted fraud. The cost-center validation contributes a less visible but equally important effect: when every invoice is validated against the mapping table, the chart of accounts stays clean, and the analytical reporting that the CFO uses to compare site performance remains reliable. Théo Richard, CFO: "Phacet est comme un membre de l'équipe, qui opère 24h/24."

The pattern across all three: cost-center validation is not the headline benefit, it is the structural enabler. Without it, the rest of the controls run on uncertain data. With it, the multi-site, multi-entity reporting that growth depends on stays trustworthy.

FAQ

What is cost center invoice validation, exactly?

Cost center invoice validation is the set of controls that run between cost-center assignment and ERP posting. It checks that the cost center exists in the current chart, is open for the period, is authorized for the GL × supplier combination, has budget remaining, and that any multi-line allocations are consistent. It is distinct from cost-center coding (which proposes the code) and from invoice approval (which validates the spend decision). See more in our glossary entry on cost center invoice routing.

What's the difference between GL coding and cost-center validation?

GL coding assigns the general ledger account and the cost center to an invoice. Cost-center validation checks that the assigned cost center is currently valid for posting (exists, open, authorized, has budget). The two are usually done by different parts of the pipeline: coding by an AI engine at intake, validation by a separate control layer before ERP entry. Confusing them is the most common reason invoices post to incorrect cost centers.

Why is budget validation needed before posting rather than during reporting?

Catching a budget breach during the month-end variance report means the money is already committed and the cost center is already overspent. Catching it during pre-posting validation means the budget owner can authorize the overrun explicitly, or redirect the spend to a different cost center. The decision is the same, but the timing changes whether the variance is a managed exception or a discovered surprise.

How does multi-line allocation validation work?

For invoices that split across multiple cost centers (shared services, multi-site overhead, project allocations), the validation control checks two things: an allocation rule exists for this supplier or expense type, and the declared percentages sum to 100%. Both checks fail in production more often than expected, often due to typos in the rule setup or new suppliers onboarded without a rule. The control catches the failures before posting rather than during the close.

How do AI agents differ from rule-based coding tools for this?

Rule-based coding tools handle existence and status checks well (these are simple lookups). They struggle on authorization (combinatorial rules that are hard to encode exhaustively), budget validation (requires real-time integration with the ERP budget data), and multi-line allocations (requires context that rule engines don't carry). AI agents handle the semantic and contextual layer, run on every invoice rather than samples, and produce an audit trail of every validation decision. See more in our analysis of agents beyond RPA.

Validation is the layer between coding and posting

The question "how can finance teams validate invoices against cost centers before ERP entry?" is really a question about which layer owns the validation work. Coding tools own the prediction. ERPs own the posting. The validation layer between them is usually missing, and that's where wrong cost centers slip through, budgets get breached silently, and the chart of accounts slowly drifts.

The fix is six controls that run between coding and posting: existence, status, authorization, budget, allocation consistency, and audit trail. Run all six on every invoice and cost-center coding stops being a guessing game. Skip them and the AP layer keeps producing plausible-looking postings that need controller review months later.

Phacet customers typically deploy the accounting inbox agent first (for intake and initial coding), the analytical mapping table agent and the budget vs actual agent next (for the validation layer), and the standardization agent to close the loop on multi-entity consistency. The first agent is in production in under two weeks. The validation layer becomes meaningful across all six controls within one to two quarters, depending on the chart complexity.

Coding tells you what cost center the invoice probably belongs to. Validation tells you whether it should actually post there.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.