What is agentic finance? A plain definition for CFOs and finance leaders

Published on :

November 5, 2025

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

Agentic finance is the operating model where finance work is executed by specialized AI agents acting across systems (ERP, banking, email, contracts), each owning a specific job and exposing its reasoning, rather than by humans operating inside an ERP or by rule-based scripts wrapped around it. It is not a single technology, it is a category shift in how finance work gets done.

That distinction matters because the term is everywhere right now, and most of its uses are imprecise. Gartner reports that 57% of finance teams are implementing or planning agentic AI. The market for agentic AI overall is projected to grow from roughly $7B in 2025 to over $90B by 2032. Vendors describe their tools as "agentic" with little consistency about what that means. Some mean RPA with an LLM bolted on. Some mean a single AI workflow with one decision step. Some, including a startup called Agentic Finance, even use the term for AI agents that make payments on behalf of consumers, which is a different problem entirely.

This article gives a working definition CFOs can use, the five structural criteria that separate genuine agentic finance from "AI-flavored automation," what it looks like in production at multi-site businesses, and how the model is different from RPA, generative AI assistants, and traditional ERP modules.

A working definition of agentic finance

Agentic finance refers to the practice of running finance operations through a network of specialized AI agents, where each agent owns a defined job (intake, matching, control, classification, reconciliation), operates with a measured degree of autonomy, exposes its reasoning, and runs continuously across the company's existing finance systems. The human role shifts from executing transactions to setting policy, reviewing exceptions, and approving overrides.

The shorter version: agentic finance is the work the finance team used to do, restructured into apps that do that work themselves and explain how they did it.

Three concepts in this definition need attention because vendors often blur them.

Agent. A specialized software entity with a defined goal (process the AP inbox, match invoices to POs, validate supplier prices, reclassify journal entries), the ability to act across multiple systems, and a structured way to expose its reasoning. An agent is not a chatbot, not a single LLM call, and not a script. A working definition lives in our glossary entry on the AI agent concept.

Agentic. A behavioral property describing software that plans, executes, and adapts toward a goal using context and feedback, rather than executing predefined steps. The term emphasizes agency (the capacity to act independently within constraints), not autonomy in the absolute sense.

Agentic platform. The infrastructure that makes agents trustworthy in production: shared data layer, observability, audit trail, human-in-the-loop controls, fallback mechanisms. Without the platform, individual agents work in demos and break in production. See our glossary entry on agentic platform for the architectural pattern.

These three nest. The platform hosts the agents. The agents exhibit agentic behavior. Agentic finance is what happens when both are deployed end-to-end across the finance function.

The 5 criteria that separate agentic finance from AI-flavored automation

A finance pipeline can have AI in it without being agentic finance. The following five criteria, applied together, distinguish the real thing from the marketing version.

Criterion 1: modular by job, not monolithic by workflow

Genuine agentic finance is built as a catalog of specialized agents, each owning a discrete finance job. One agent handles the AP inbox. Another runs three-way matching. A third detects fake IBAN attempts. A fourth standardizes the GL coding. The agents compose into workflows but remain individually selectable, swappable, and observable.

The opposite pattern is monolithic AI workflows that promise to "transform AP" or "automate the close" as a single black box. The monolithic version is harder to deploy incrementally, harder to audit per job, and harder to govern when one job needs a different policy than another.

This is why the Phacet catalog is structured around 40+ named agents (built across 100+ real deployments), not around generic workflow templates. Each AI agent in the catalog is selectable, scoped, and accountable.

Criterion 2: cross-system execution, not intra-system automation

Agentic finance agents act across the existing system stack: email, ERP, banking, supplier portals, contract repositories, BI tools. They do not live inside a single ERP screen. This is the structural reason agentic finance is different from ERP automation modules: the agent's job often is the work that crosses the gap between systems.

A 3-way matching agent reads the PO from the ERP, the invoice from the AP inbox, and the goods receipt from the warehouse system, then reconciles them with justification. The work was always cross-system. What changed is that the cross-system reconciliation is now done by an agent, not by a controller copying between tabs.

This is the architectural reason Phacet positions itself as a layer over the existing finance stack rather than as a replacement: a migration to a new ERP costs hundreds of thousands of euros, an orchestration layer does not.

Criterion 3: exposed reasoning, not opaque outputs

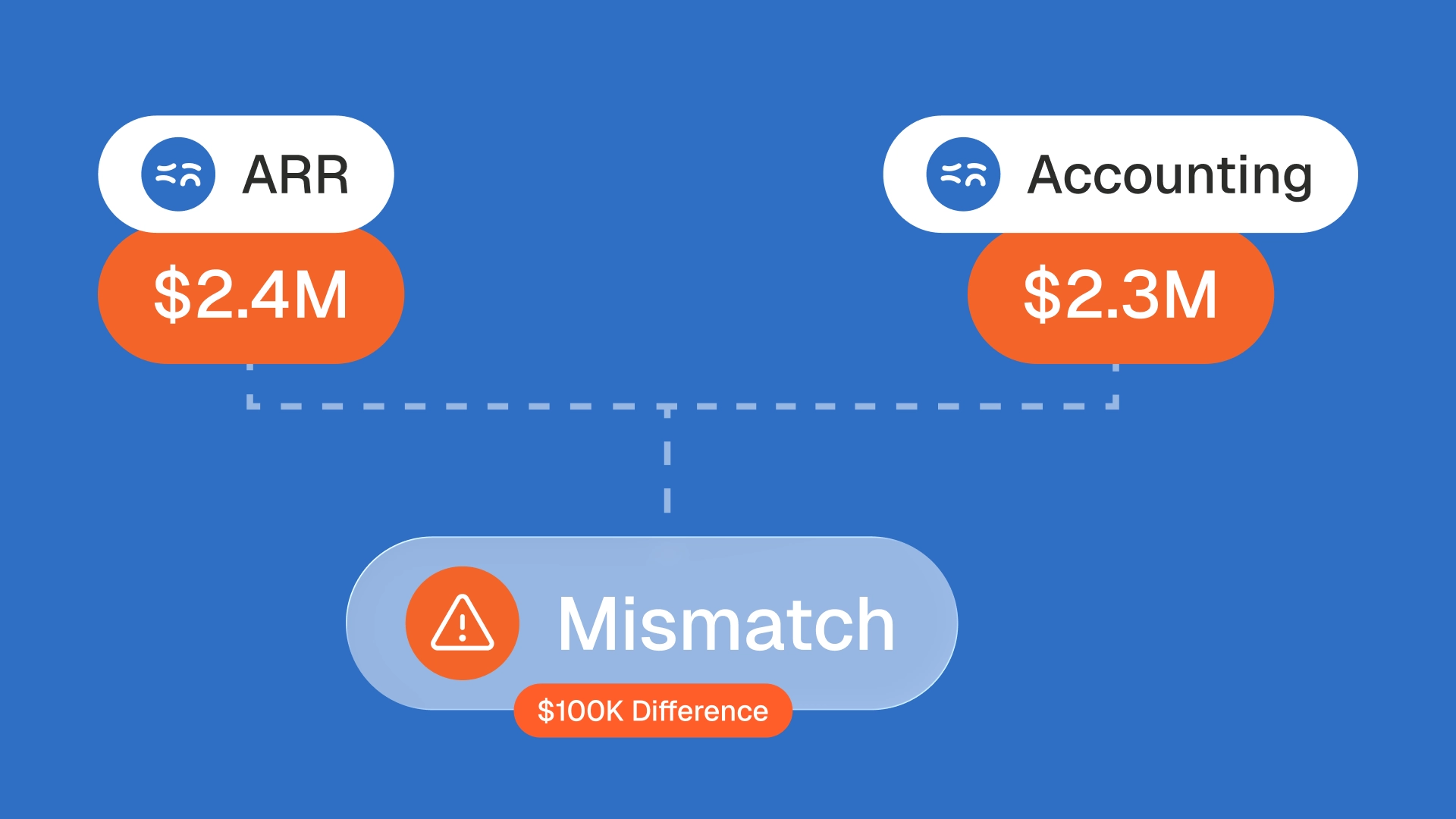

A genuine agent shows its work. For every decision (a match, a coding, a flag, a route), the agent surfaces the inputs it considered, the comparison it ran, the threshold it applied, and the confidence score it assigned. A controller can open any record in a detail view and inspect why the agent reached a particular conclusion.

This criterion fails for most consumer-grade AI tools (ChatGPT, Claude, generalist copilots), which produce answers without a structured trace of the reasoning. For finance work, exposed reasoning is non-negotiable: the controller needs to defend the entry to an auditor, the CFO needs to understand variance, the budget owner needs to see why their cost center received a charge.

This is the control layer of the structurer / controller / leverage triad that every Phacet agent follows: structure the input, control against a reference, expose the reasoning.

Criterion 4: native audit trail, not after-the-fact logging

Every agent action (every extraction, every match, every override, every routing decision) is timestamped, stored, and inspectable. The audit trail is a property of the system, not an additional reporting layer bolted on after the fact. An auditor can reconstruct what happened on any transaction at any point in time.

This is the criterion that most distinguishes finance-grade agentic AI from generalist AI tools. Generalist tools (Claude, ChatGPT, Dust) are remarkable for many tasks, but they do not produce a native audit trail of every action they take on enterprise data. For a finance function regulated by SOX, French Loi Sapin II, or any internal control framework, a native audit trail is what makes agentic finance defensible.

Criterion 5: human-in-the-loop by design, not as a fallback

The fifth criterion is the principle that the human role is built into the architecture, not patched in when something goes wrong. Every agent operates with a confidence threshold. Above the threshold, the action clears automatically. In the ambiguous middle zone, the agent surfaces the proposed action with its reasoning and waits for a human review. Below the lower threshold, the entire transaction routes to manual handling.

This is what human-in-the-loop control means in practice: not "AI does everything until it breaks," but "AI does the bulk, humans handle the judgment calls, and the system makes it obvious which is which." The team's role moves from "process every transaction" to "review the exceptions and own the policy."

Vendors that pitch full autonomy as the goal misread the finance buyer. The goal is reliable, controllable, auditable operation. Autonomy is a means, not the end.

Why agentic finance is different from RPA, generative AI, and ERP automation

A side-by-side comparison clarifies what agentic finance is not, which is often the most useful test.

ApproachWhat it does wellWhere it breaks for financeRPA (Robotic Process Automation)Repetitive deterministic tasks with structured inputsBreaks on edge cases, no semantic reasoning, no native audit trailGenerative AI assistants (Claude, ChatGPT, Dust, Langdock)Conversational summaries, draft text, quick analysesNo domain expertise, no integrations with finance systems, no audit trail, data used for trainingERP automation modules (SAP, NetSuite, Sage)Intra-system workflows tied to the ERP's data modelStops at the ERP boundary, requires migration to upgradeAgentic finance (Phacet, ChatFin, Auditoria, Safebooks, Vic.ai)Specialized agents acting across systems with exposed reasoning and audit trailRequires platform-level governance and integration discipline to scale

The operational difference is that RPA executes instructions, agentic finance executes intent. An RPA script following a fixed path will fail on a vendor name that varies in formatting. An agent reasoning about the same task will recognize that "Acme Logistics SARL" and "ACME LOGISTICS" are the same supplier and proceed. The difference is not marginal. It is what separates a pipeline that works in production from one that drowns the team in exceptions.

The difference with generalist GenAI tools matters too. Generalist tools are remarkable for ad-hoc work but they do not know your suppliers, your contracts, your chart of accounts, your ERP. They do not produce an audit trail. They do not connect to your inbox or your SFTP. And the data you give them is often used to train the next version. Agentic finance, done properly, addresses all four of those structural gaps.

What agentic finance looks lmike in production

Three customer outcomes illustrate what agentic finance delivers when the five criteria are met:

The French Bastards, a Parisian artisanal bakery group, doubled its boutique count from 7 to 14 sites without adding finance headcount. The intake agent handles every invoice from the email inbox. The 3-way matching agent reconciles against orders. The standardize-and-reclassify agent applies consistent coding across all entities. Marie-Céline, Head of Finance: "On voit Phacet comme un vrai partenaire. Vous nous poussez des idées auxquelles je n'aurais pas pensé." The decoupling between site count and finance team size is the operational signature of agentic finance.

Astotel, a group of 18 Parisian hotels, recovered roughly 5,000€ per year on a single supplier through line-by-line price variance checks. The supplier billing control agent runs the check on every invoice, not on samples. Valérie, Directrice Achats: "Je gagne jusqu'à deux jours par mois, et je repère des erreurs que je n'aurais jamais vues seule." The signature feature here: the agent surfaces variance the human couldn't see at sample coverage, with full reasoning exposed.

La Nouvelle Garde, a group of 10 Parisian brasseries, eliminated roughly 1,800 manual operations per year and intercepted 28,000€ of attempted fraud, while reducing the time spent in Gmail and Pennylane by 70%. Théo Richard, CFO: "Phacet est comme un membre de l'équipe, qui opère 24h/24." The 24/7 operation is the practical expression of continuous agent execution, vs. human-paced batch processing.

A fourth proof point on transparency: at Jinchan, the operational shift came less from speed than from visibility. Alban Cacace, COO: "On voit exactement ce qui est fait. Rien n'est caché. Aucune formation. En testant, j'ai compris." That sentence is what criterion 3 (exposed reasoning) feels like in daily use.

What agentic finance demands from the organization

Agentic finance is not a software purchase. It is an operating-model change with three preconditions for it to actually deliver on the promise.

A defensible chart of accounts and supplier master. Agents are only as good as the reference data they validate against. If the chart of accounts is messy, the cost-center assignments will be probabilistic. If the supplier master is duplicated, vendor identification will be unreliable. Agentic finance assumes the underlying data is clean enough to act on, and includes agents that help keep it clean (master data fiabilization, mapping table control).

A clear policy on what humans own and what agents own. The team needs to define the confidence threshold above which an agent auto-clears, the middle zone that triggers review, and the lower zone that forces manual handling. These thresholds are not technical defaults, they are business decisions about risk tolerance.

A willingness to redesign the role of the finance team. The composition of finance work changes when agents take the transactional load. Controllers stop processing every invoice and start reviewing exceptions. Senior team members get back the time they used to spend on data entry. CFOs gain access to faster, more reliable variance analysis. None of that happens automatically. It requires the team to actively reallocate its hours toward the work the agents leave to them.

The IBM Institute for Business Value 2025 CEO Study reports that only 25% of AI initiatives have delivered the expected ROI, and only 16% have scaled enterprise-wide. The most common reason is not the technology, it is the absence of the three preconditions above.

FAQ

What is agentic finance in one sentence?

Agentic finance is the operating model where finance work is executed by specialized AI agents acting across the company's systems (ERP, banking, email, contracts), each owning a specific job and exposing its reasoning, rather than by humans operating inside an ERP. See our glossary entry on the AI agent for the building-block definition.

Is agentic finance the same as autonomous finance?

Not quite. Autonomous finance describes a vision where finance processes run with minimal human intervention. Agentic finance describes the operational model that gets you there: specialized agents, human-in-the-loop architecture, exposed reasoning. Autonomy is a degree of agentic operation, not its definition. A finance function can be agentic without being fully autonomous, and the practical sweet spot is exactly that: agents handle the bulk, humans handle the judgment.

How is agentic finance different from RPA?

RPA executes predefined steps deterministically. It works well for structured tasks with stable inputs (bulk invoice posting to an ERP, end-of-day reconciliation against fixed rules). It breaks on semantic variation (vendor names that differ in formatting, line descriptions that drift) and on cross-system tasks that require reasoning. Agentic finance handles both the semantic layer and the cross-system orchestration, with a native audit trail RPA does not produce. See our analysis on moving beyond RPA.

Is ChatGPT agentic finance?

No. ChatGPT (and Claude, Dust, Langdock, etc.) are generalist AI tools, remarkable for ad-hoc conversational work. They do not know your suppliers, your contracts, your chart of accounts, your ERP. They do not produce a native audit trail. They do not run on a schedule or react to events in your finance systems. They are useful as cockpit tools for an experienced operator, but they are not a substitute for an agentic finance platform.

What's the minimum setup to start using agentic finance?

A first agent in production typically takes under two weeks. Phacet customers commonly start with the accounting inbox agent (intake, classification, routing), then layer on the 3-way matching agent and the supplier billing control agent. A meaningful composition shift (50% of transactional work moved out of the human queue) takes about one quarter. Full multi-agent deployment across AP, reconciliation, and reporting takes two to three quarters depending on the entity count and integration complexity.

Is agentic finance regulated?

The agents themselves are not directly regulated as a category, but the operations they execute are. SOX, French Loi Sapin II, GDPR, ISO 27001, sector-specific accounting standards, and internal control frameworks all apply to the outputs of agentic finance the same way they apply to any other finance pipeline. The native audit trail (criterion 4) is what makes agentic finance defensible in those regulated contexts.

Agentic finance is a category, not a feature

The shortest test for whether a vendor's "agentic" claim is real: ask them to show you the audit trail of an agent's decision, ask them which specific agent owns a specific job, and ask them where the human-in-the-loop threshold sits. If they can answer all three concretely, they are doing agentic finance. If the answer drifts toward "the AI handles it intelligently," they are doing AI-flavored automation.

The category will mature in 2026 and 2027. Vendors will consolidate around platforms that meet the five criteria. The finance teams that get there first will be running 4x to 5x the volume of finance work with the same team size, because the work composition will have shifted from transactional to oversight. The teams that don't will keep hiring proportionally to volume growth, because their automation will keep breaking at the semantic layer.

Phacet operates in this category as a catalog of 40+ specialized AI agents for finance work, each one built around the five criteria above and deployed across 100+ real customer environments. The first agent goes live in under two weeks. The vision is laid out further in our agentic revolution in intelligent finance automation analysis and in the broader picture of the autonomous finance team the model enables.

Agentic finance is the work your finance team does, restructured into apps that do that work and explain how. The technology is real. The shift is structural. The hard part is not the agents. It is the operating-model change the agents make possible.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.