How finance teams can detect and block duplicate invoices before payment approval

Published on :

March 3, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

A duplicate invoice is not a rare event. According to the Association of Certified Fraud Examiners, duplicate payments represent one of the top three billing fraud schemes, and even when they are not fraudulent, they occur in every accounts payable environment with enough frequency to be material. Finance teams processing 300 invoices per month with a 1% duplicate rate are making 36 unnecessary payments annually before anyone catches the pattern.

The problem is not that duplicates are difficult to identify once flagged. It is that they are designed, whether by accident or intent, to avoid being flagged in the first place. A resubmitted invoice with a slightly different reference number, a document that arrives on two separate channels in a multi-entity group, a vendor that resends an "unpaid" invoice 47 days after the original was paid: none of these look obviously wrong to a reviewer processing 50 documents in a morning. They look like normal invoices, because in most of their fields, they are.

Blocking duplicates before payment approval requires detection logic that operates systematically across the full invoice history, not reviewer attention applied to the invoices that happen to raise a question. This article explains where duplicates come from, why they slip through manual and ERP-level controls, and what a reliable pre-payment detection system actually needs to catch them.

Where duplicate invoices actually come from

Understanding the origin patterns of duplicate invoices is the first step toward detecting them reliably. Not all duplicates share the same mechanism, and a detection system that only catches the most obvious variant, identical document submitted twice, misses most of what finance teams actually encounter.

Accidental resubmission by the supplier

The most common source. A supplier invoices in October, does not receive payment by their expected date, and resubmits the invoice in November with a follow-up email. The accounts payable team processes the second submission without checking whether the first was already in the payment queue or had been paid. No fraud was intended, the supplier genuinely believed the invoice was outstanding.

This scenario multiplies in multi-entity environments, where the first submission and the second submission may have gone to different inboxes, been processed by different team members, or been routed to different ERPs. Neither person saw the other's document.

Reference number variants

Suppliers occasionally modify invoice reference numbers between the original submission and the resubmission: INV-2024-0892 becomes INV2024-892, or a trailing digit increments from 0892 to 0893. These minor variants defeat exact-match duplicate detection, which checks whether an identical invoice number already exists in the system. They do not defeat fuzzy-match detection, which checks whether a near-identical reference exists within a defined amount and date tolerance.

Exact-match detection alone fails on the majority of real-world duplicate submissions, because genuine duplicates rarely arrive with identical reference numbers. A supplier who knows their original invoice was rejected due to a formatting issue will correct the reference before resubmitting, creating a document that looks new to any system that matches on reference number alone.

Cross-period submission

An invoice submitted in late December, after month-end processing has closed, gets picked up and processed in January. The December payment runs close, the January run opens, and the same invoice re-enters the pipeline as though it were a new document. Without a detection window that spans across accounting periods, cross-period duplicates bypass period-end controls entirely.

Month-end close time pressure makes this variant particularly common. Teams rushing to clear invoice queues before cut-off process documents quickly, and the first submission of an invoice that arrived late may not be logged clearly enough for the January team to recognize it.

System migration duplicates

When companies migrate from one ERP to another, or consolidate multiple systems into a single platform, historical invoice data is imported into the new environment. Documents that were in a "pending" state at the time of migration may be reprocessed automatically or manually, generating payments that were already made in the legacy system. This is not a recurring pattern, but it can generate a concentrated volume of duplicate payments in a short period, and it occurs at exactly the moment when finance teams are already stretched managing the transition.

Intentional vendor fraud

The deliberate variant. A supplier submits the same invoice twice with minor modifications, or submits two invoices for the same delivery under different reference numbers, relying on the volume of incoming documents and the limits of manual review to avoid detection. According to ACFE data, billing fraud schemes, which include duplicate submission, account for the most common form of occupational fraud in organizations with fewer than 100 employees, with median losses of $150,000 per incident.

Why ERP-level duplicate detection is not enough

Most ERP systems include some form of duplicate invoice checking, typically a warning that triggers when an invoice number already exists in the vendor ledger. Finance teams often assume this control is sufficient. In practice, it catches a narrow subset of actual duplicates and misses the rest for predictable structural reasons.

ERP duplicate checks run on already-entered data. The check happens after the invoice has been keyed into the system, which means it occurs after the document has consumed staff time for data entry and after any OCR processing cost has been incurred. Even when the duplicate is caught, the workflow has already been initiated.

ERP checks rely on exact field matching. Standard ERP duplicate logic checks whether the vendor ID, invoice number, and amount are identical to an existing record. A resubmission with a different invoice number, even one that differs by a single character, passes the check cleanly. A document with a correctly formatted header but a line-item adjustment passes. A cross-entity submission that hits a different company code passes, because the duplicate check runs within entity scope, not across the group.

ERPs do not see documents that haven't been entered yet. If a duplicate arrives in the accounting inbox but hasn't been keyed in, the ERP cannot detect it. Pre-entry duplicate checking requires a control layer that operates at the inbox level, before documents are processed, not after they are recorded.

This is the structural gap that pre-decision control addresses: moving the detection point upstream, to the moment the document arrives, rather than downstream, after it has entered the accounting system. For a broader look at how this upstream validation layer works across multiple control types, see our article on AI-powered invoice reconciliation and smart finance.

The four parameters that reliable duplicate detection requires

Building a pre-payment duplicate detection system that catches the full range of duplicate variants, not just exact matches, requires checking against four parameters simultaneously on every incoming invoice.

Supplier identity + amount + date window

The most reliable detection combination for accidental resubmission and cross-period duplicates. Rather than checking whether an identical invoice number exists, this check asks: has the same supplier submitted an invoice for approximately the same amount within a defined time window? The time window is configurable, typically 30 to 90 days, and the amount tolerance can accommodate minor differences in VAT rounding or currency conversion without generating false positives.

This combination catches the category of duplicates that reference-number matching misses: the supplier who resubmits with a new reference, the document reprocessed after month-end, the cross-period submission that entered at different points in the payment cycle.

Fuzzy reference number matching

Applied in parallel with the supplier-amount-date check, fuzzy matching on invoice reference numbers catches documents that have been modified to avoid exact-match detection. The algorithm checks for near-identical strings: transposed digits, incremented trailing numbers, removed separators, format changes between INV-0892 and INV0892. A human reviewer might notice these variants when reviewing two documents side by side; automated fuzzy matching notices them systematically across the full invoice history without requiring anyone to happen to look at both documents at the same time.

Cross-entity scope in multi-entity environments

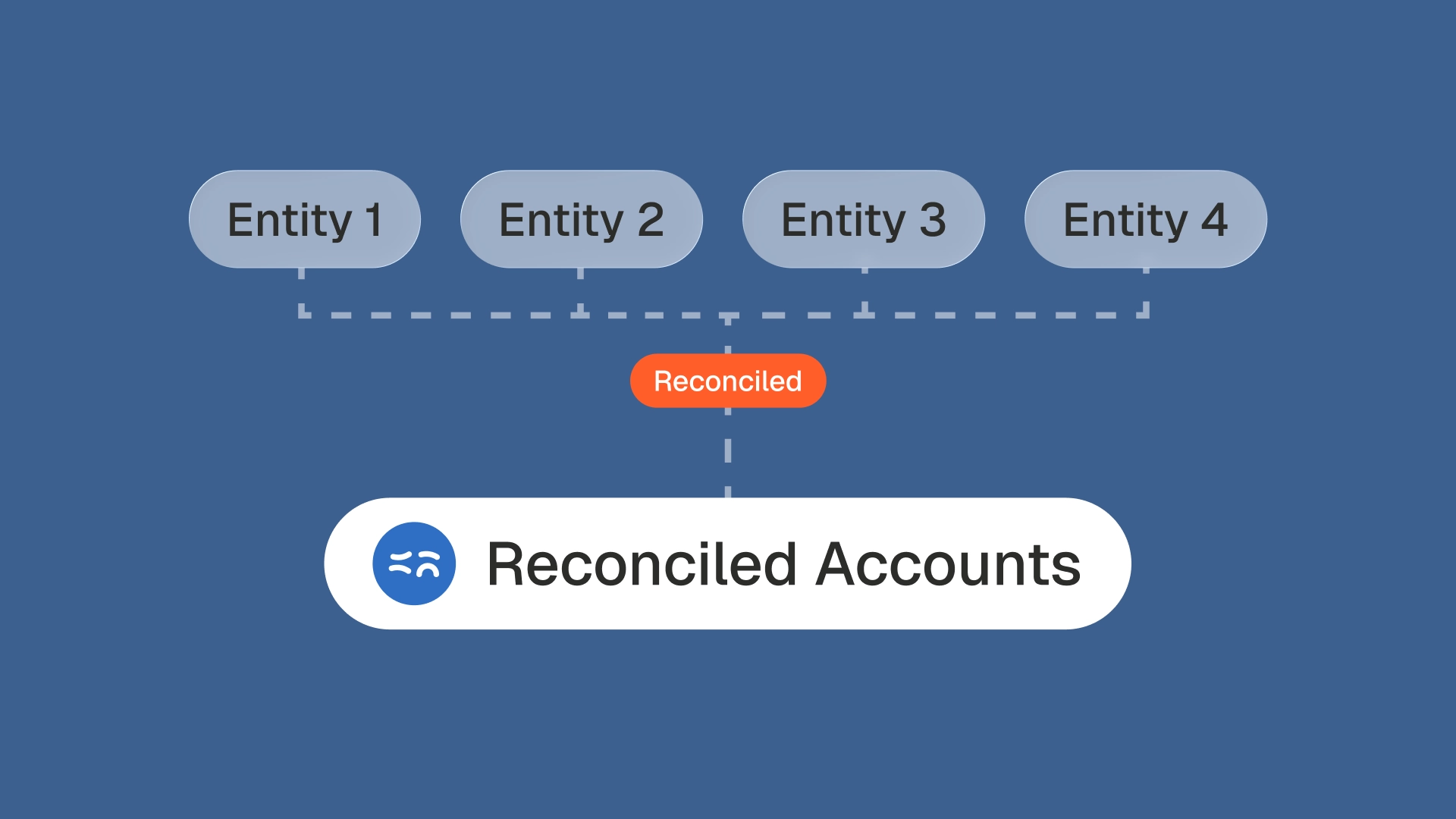

For groups with multiple legal entities, holding companies, subsidiaries, multi-site operations, multi-brand structures, duplicate detection must operate across entity scope, not within it. A supplier invoice submitted to Entity A and the same invoice submitted to Entity B are not duplicates within either entity's ERP. They are duplicates only when viewed across the group's full invoice dataset.

This is where ERP-level detection fails most completely. Each entity's ERP checks its own records; none of them see the other's. Cross-entity duplicate detection requires a layer that sits above the individual ERPs and checks incoming documents against the combined invoice history of the entire group. La Nouvelle Garde, managing 14 restaurant locations each with its own supplier relationships and invoice streams, implemented exactly this architecture to prevent the cross-location duplicate submissions that had previously gone undetected within individual site-level processing. Read more about their implementation in the La Nouvelle Garde case study.

Full history search, not current-period scope

Duplicate detection limited to the current accounting period misses cross-period submissions. A reliable duplicate check searches the full available invoice history, not just the last 30 days, not just the current month, but all records in the system, when evaluating whether an incoming document has been previously submitted and paid.

The lookback window matters most for detecting the slow-resubmission variant: a supplier who waits 60 days before resubmitting, after a payment dispute or a genuine belief that the original was lost, will bypass any detection logic limited to the current period. Full-history search makes the resubmission date irrelevant, any document that matches across the four parameters triggers a review, regardless of when the original was submitted.

The multi-entity problem: why growing companies face higher duplicate risk

Duplicate invoice risk scales with organizational complexity in a non-linear way. A single-entity company processing invoices through a single ERP with a single finance team has manageable duplicate exposure. A group with five entities, three ERPs, separate accounting teams per subsidiary, and a shared supplier base has a structural duplicate detection problem that no individual team can solve on its own.

The complexity compounders are predictable:

Shared supplier base across entities. When the same supplier delivers to multiple sites and invoices separately for each, the supplier holds the complete picture of what they've submitted. The finance team does not, unless it has cross-entity visibility. A supplier who accidentally duplicates a submission across two entities will be paid twice, not because either entity's team was careless, but because neither had visibility into the other's invoice history.

Different invoice receipt channels per entity. In practice, multi-entity groups often have separate accounting email addresses per entity, with documents routed manually or semi-automatically. The same invoice can arrive in two different inboxes on the same day without the teams processing each inbox ever being aware of the overlap.

Volume pressure during growth. The French Bastards expanded from 7 to 14 locations while managing invoice volume that grew proportionally, but finance headcount did not. At higher volumes, the probability that a duplicate arrives within the same processing batch as the original drops, making manual detection even less reliable. The automated accounting inbox that Phacet deployed for their growth phase handled cross-location routing and duplicate detection as part of the same intake process. Read the full The French Bastards case study for the detail.

The structural answer to multi-entity duplicate risk is not adding headcount or increasing review thoroughness per entity. It is moving duplicate detection to a layer that operates above entity-level processing, at intake, across the full group, before any document is entered into any ERP.

How Phacet's pre-payment duplicate detection works

Phacet's detection logic runs at the point of invoice intake, when documents arrive in the accounting mailbox, before they are forwarded to any ERP or payment workflow. Every incoming invoice is checked against the full group invoice history across all four detection parameters simultaneously.

The process works in four steps.

Step 1 — Extraction and normalization.

Each incoming document is parsed via OCR to extract supplier identity, invoice reference, line amounts, invoice date, and entity routing information. The extracted data is normalized to a standard structure, removing formatting variants that would defeat exact-match detection.

Step 2 — Four-parameter cross-check.

The normalized invoice data is checked against the full invoice history: exact and fuzzy reference matching, supplier-amount-date window matching, and cross-entity scope. The check runs in real time, at intake, before the document advances in any workflow.

Step 3 — Flag and queue for review.

Documents that trigger a match on any of the four parameters are flagged and routed to a structured review queue rather than the normal processing flow. The flag includes the specific match that triggered the alert, which prior invoice was matched, what the reference variant was, whether the match was cross-entity, giving the reviewer the context to resolve the case in seconds rather than needing to investigate from scratch.

Step 4 — Audit trail.

Every detection result is logged: documents that passed without flagging, documents that were flagged, the specific detection parameter that triggered the flag, and the resolution decision. This record constitutes the audit trail for duplicate detection decisions, available for CAC audits, internal governance reviews, and any supplier dispute where the payment history needs to be reconstructed.

The result is what Phacet's supplier billing control agent delivers as part of the broader pre-payment validation layer: systematic detection coverage on 100% of incoming invoices, without requiring reviewer attention on the 95%+ that are clean. Human-in-the-loop review applies only to flagged documents, with the context needed to make a fast and well-informed decision.

For a full picture of how duplicate detection integrates with price validation, fraud checks, and three-way matching in a single pre-payment control layer, see our article on AI supplier invoice verification and cost compliance.

What duplicate detection saves: the full cost picture

The direct cost of a duplicate payment is the amount paid twice. But the full cost of a duplicate invoice that isn't caught before payment is higher, and it accumulates across three dimensions.

Recovery overhead.

Once a duplicate has been paid, recovering the funds requires identifying the error, contacting the supplier, obtaining a credit note or refund, and reconciling the correction in the ERP. Finance teams report 2 to 4 hours of recovery work per identified duplicate payment. At scale, that labor cost often exceeds the value of the original duplicate payment for low-value invoices, making prevention not just financially preferable, but the only economically rational approach.

Cash timing cost.

A duplicate payment occupies cash from the moment it is made until the credit note is processed or the refund received. For a company processing €2M in monthly supplier payments with a 1% duplicate rate, that represents €20,000 in cash that is unnecessarily deployed at any given time, cash that could be working elsewhere.

Reporting distortion.

Every undetected duplicate creates a discrepancy between what the ERP records and what was actually owed. Cost center reports, margin calculations, and budget variance analyses all contain noise proportional to the duplicate rate. Cleaning up duplicate payments after month-end close takes time and introduces restatement risk in financial reporting. Catching duplicates before ERP entry keeps the data clean from the start, which is exactly what accounts payable automation built around pre-payment detection delivers, rather than post-entry reconciliation.

Astotel reduced its overall invoice error rate from 7% to 2% by deploying systematic pre-payment validation across its hotel portfolio, a reduction that included duplicate detection alongside price compliance and fraud checks. The Astotel case study details how the implementation worked across multiple properties with shared supplier relationships.

Frequently Asked Questions

What is a duplicate invoice?

A duplicate invoice is a supplier invoice that has already been submitted and paid, or is in the payment queue, that is submitted again, either accidentally or deliberately. It may be an identical copy of the original, a resubmission with minor reference modifications, or the same delivery billed under two separate documents. The financial impact is a double payment: the same obligation paid twice, requiring a credit note or refund to recover the excess.

How common are duplicate invoices?

Industry benchmarks suggest duplicate invoices represent 0.1% to 1% of processed invoices in typical accounts payable environments. In higher-volume environments, multi-entity groups, companies during rapid growth, organizations that have recently undergone ERP migrations, the rate can be higher. Even at 0.5%, a company processing 500 invoices per month makes 30 duplicate payments annually before detection.

Why does ERP duplicate detection miss so many duplicates?

ERP systems check for duplicate invoice numbers within the same vendor account. They miss duplicates when the invoice reference has been modified (even slightly), when the same document arrives via different entities in a multi-entity group, when the duplicate falls outside the period being checked, or when the document hasn't yet been entered into the ERP at all. Pre-payment duplicate detection, running at the inbox level before ERP entry, closes each of these gaps.

What detection parameters are most effective for catching duplicates?

The most reliable duplicate detection combines four checks: supplier identity paired with invoice amount and a date window (catching resubmissions with new references), fuzzy matching on invoice reference numbers (catching near-identical reference variants), cross-entity scope (catching submissions that land in different entity inboxes), and full-history lookback (catching cross-period resubmissions beyond the current accounting period). Exact-match reference checking alone, what most ERP systems provide, reliably catches only the most obvious subset.

How should duplicate detection handle minor invoice differences?

Not every near-match is a true duplicate. A supplier may legitimately issue two invoices for similar amounts in a short period. Effective detection uses configurable tolerance thresholds: an amount tolerance (typically 1–3% or a fixed minimum) and a date window (typically 30–90 days) within which near-matches trigger a review flag rather than an automatic block. The reviewer then confirms whether the match is a genuine duplicate or a legitimate separate transaction, with the context surfaced by the system rather than requiring the reviewer to investigate from scratch.

Can duplicate detection work when invoices arrive in different formats?

Yes, provided the detection system includes document normalization before comparison. A PDF invoice and a scanned image of the same invoice may look identical to a human reviewer but have entirely different file structures. Effective duplicate detection extracts and normalizes the data fields, supplier, reference, amount, date, from every document format before running cross-checks, so the comparison operates on structured data rather than raw file content.

What happens when a duplicate is incorrectly flagged?

A false positive, a legitimate invoice flagged as a potential duplicate, is resolved through the exception review process. The reviewer examines the specific match that triggered the flag, confirms that the two invoices represent separate legitimate obligations, and approves the document for normal processing. The resolution is logged in the audit trail. Well-calibrated detection systems achieve false positive rates below 5%, meaning the vast majority of flagged documents are genuine duplicates or near-duplicates warranting review.

How does duplicate detection integrate with other pre-payment controls?

Duplicate detection is most effective when it runs as part of a broader pre-payment validation layer, alongside price compliance checks, supplier identity verification, IBAN fraud detection, and three-way matching. Running all controls at intake, on every document, before ERP entry, means a single validation pass covers the full range of invoice error and fraud vectors simultaneously. Phacet's platform runs this complete control sequence as part of the same intake workflow, so duplicate detection is not a standalone check but one of several that run together on each incoming document.

The duplicate that nobody saw coming

Duplicate invoices share a characteristic that makes them particularly costly in manual-review environments: they don't announce themselves. They look like normal invoices, because they are normal invoices, just ones that have already been submitted. The only way to know they are duplicates is to check them against everything that has already been processed.

That check, systematic, cross-entity, full-history, fuzzy-matched, cannot be performed reliably by human reviewers processing invoice queues under time pressure. It can be performed reliably by a detection system that runs automatically on every incoming document, at intake, before payment approval.

The 1% duplicate rate that looks small in percentage terms translates to concrete cash losses, recovery overhead, and reporting distortion that compound over time. The companies that eliminate duplicate payments aren't the ones that review invoices more carefully. They are the ones that moved the detection check before the payment, not after. Book a demo to see how Phacet's duplicate detection works across your invoice volume and entity structure.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.