Continuous finance control: how finance teams move from monthly checks to pre-decision control

Published on :

April 6, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

Most finance teams run their control processes on a calendar. Bank reconciliations happen at month-end. Invoice reviews happen when the payment run is due. Expense reports are checked in the week before the close. The rhythm of control is set by the reporting cycle, not by the flow of transactions.

This is not a design choice. It is an inheritance, the residue of a time when checking every transaction manually was physically impossible, so teams sampled and scheduled instead. Monthly checks were never the right answer to the control problem. They were the best available answer given the resources that existed.

Those resources have changed. The question now is whether finance teams will change with them, or continue running a legacy control model on modern infrastructure.

What monthly checks actually protect against (and what they don't)

Monthly control cycles provide a specific kind of assurance: that the errors visible at the end of a period have been identified and addressed before numbers are published. That is genuinely valuable. But it is a much narrower assurance than most finance teams assume when they describe their controls as "robust."

Consider what monthly checks cannot provide:

Protection at the point of decision. By the time a monthly review catches a supplier invoice that was paid at the wrong price, the payment has already been made. The recovery process, disputing the invoice, requesting a credit note, chasing the fournisseur, takes time, generates friction, and frequently results in partial rather than full recovery. Pre-payment controls applied before payment authorisation intercept the error when reversal is costless. Monthly checks catch it after the cost has been incurred.

Protection across the full transaction population. Monthly reviews involve sampling. Even a rigorous finance team cannot manually check every invoice, every bank transaction, and every expense claim in a month of volume. Sampling misses the errors that don't appear in the sample, and anomalies systematically occur in the transactions that look ordinary enough to be excluded from detailed review. Continuous pre-decision control covers 100% of the transaction population, not a representative subset.

Actionable error signals while resolution is still feasible. A discrepancy identified 28 days after it occurred is harder to investigate than one identified 28 minutes after it occurred. The context is stale. The people involved may not remember. The documentation may be incomplete. Early detection is not just better, it is qualitatively different, because the errors that surface immediately are still correctable with full information.

Reliable data for decisions made during the period. Board decisions, payment approvals, purchasing commitments and cash management choices made during a month are all based on unreconciled data. The monthly close validates the data retrospectively. The decisions have already been made. Continuous control means that the data supporting mid-period decisions reflects the best available verified state, not the state as of the last close.

The pattern is consistent: monthly checks protect against reporting errors. Continuous finance control protects against decision errors. For a finance function that sees itself as a strategic partner rather than a reporting function, the distinction matters enormously.

The 4 characteristics that define pre-decision control

Moving from monthly checks to continuous pre-decision control is not simply a matter of running existing checks more frequently. It requires a different control architecture, one designed around transactions rather than periods, exceptions rather than samples, and prevention rather than detection.

Four characteristics define this architecture:

1. Event-driven, not calendar-driven

In a monthly control cycle, controls run when the calendar says they should. In continuous control, controls run when transactions occur. An invoice arrives, the control runs immediately, comparing the line items against contracted prices and flagging deviations before the invoice enters the approval queue. A bank transaction posts, the reconciliation runs immediately, matching the movement against its ERP counterpart and surfacing unmatched items in real time.

This shift from calendar-driven to event-driven control is the foundational change. Everything else follows from it. When controls run continuously rather than periodically, the error population at any point in time is limited to transactions that have occurred since the last control ran, measured in hours, not weeks.

2. Transaction-level, not sample-based

Monthly control processes are bounded by human bandwidth. An AP team of three can review a few hundred invoices in a week, not the few thousand that may have been processed. The selection of what to review is necessarily an approximation.

Continuous AI-powered control has no such bandwidth constraint. Every transaction is checked. Every invoice is compared against contracted prices. Every bank movement is matched against its ledger counterpart. Every expense claim is validated against policy. The exception-based finance review model means that human attention is reserved for the transactions that genuinely require it, not distributed across a sample that may or may not represent the population.

This changes the accuracy guarantee from "we checked a representative sample and found no significant errors" to "we checked every transaction and here are the specific exceptions that require review."

3. Before commitment, not after payment

The most consequential shift in pre-decision control is temporal: moving the control point upstream of the financial commitment, not downstream of it.

A supplier invoice verified before payment approval is interceptable without cost. A supplier overpayment discovered in a monthly review costs time to recover and may not be fully recovered. An expense claim validated before reimbursement is correctable at zero friction. An expense claim flagged after reimbursement requires a conversation, a credit, and a process.

Pre-payment controls are not just earlier monthly controls, they are controls positioned at the point where interception is free. This is what the term "pre-decision" means in practice: the control runs before the decision that is difficult or expensive to reverse.

4. Documented by design, not reconstructed retrospectively

Monthly control processes generate documentation as a side effect, the spreadsheet that was used, the email that flagged the issue, the approval that was signed. Audit-ready finance processes require assembling this documentation into a coherent record when an auditor asks for it.

Continuous control generates documentation as a primary output. Every comparison performed, every exception identified, every resolution path taken, and every human decision made is recorded automatically, timestamped, and linked to the underlying transaction. The audit trail is not a by-product of the control process, it is the control process.

When an auditor asks to see the controls applied to a specific invoice, the answer is not "let me reconstruct what happened", it is "here is the complete record of every check performed, every result returned, and every decision made, in sequence."

The 5 operational shifts: from periodic to continuous

The transition from monthly checks to continuous pre-decision control involves five distinct operational changes. They do not need to happen simultaneously, most organisations implement them progressively, starting with the highest-value control domain and expanding from there.

Shift 1: replace sampling with population-level control on priority transaction flows

The first shift is the most impactful: moving the highest-value transaction flows, typically supplier invoices and bank reconciliation, from sampled monthly review to continuous transaction-level control.

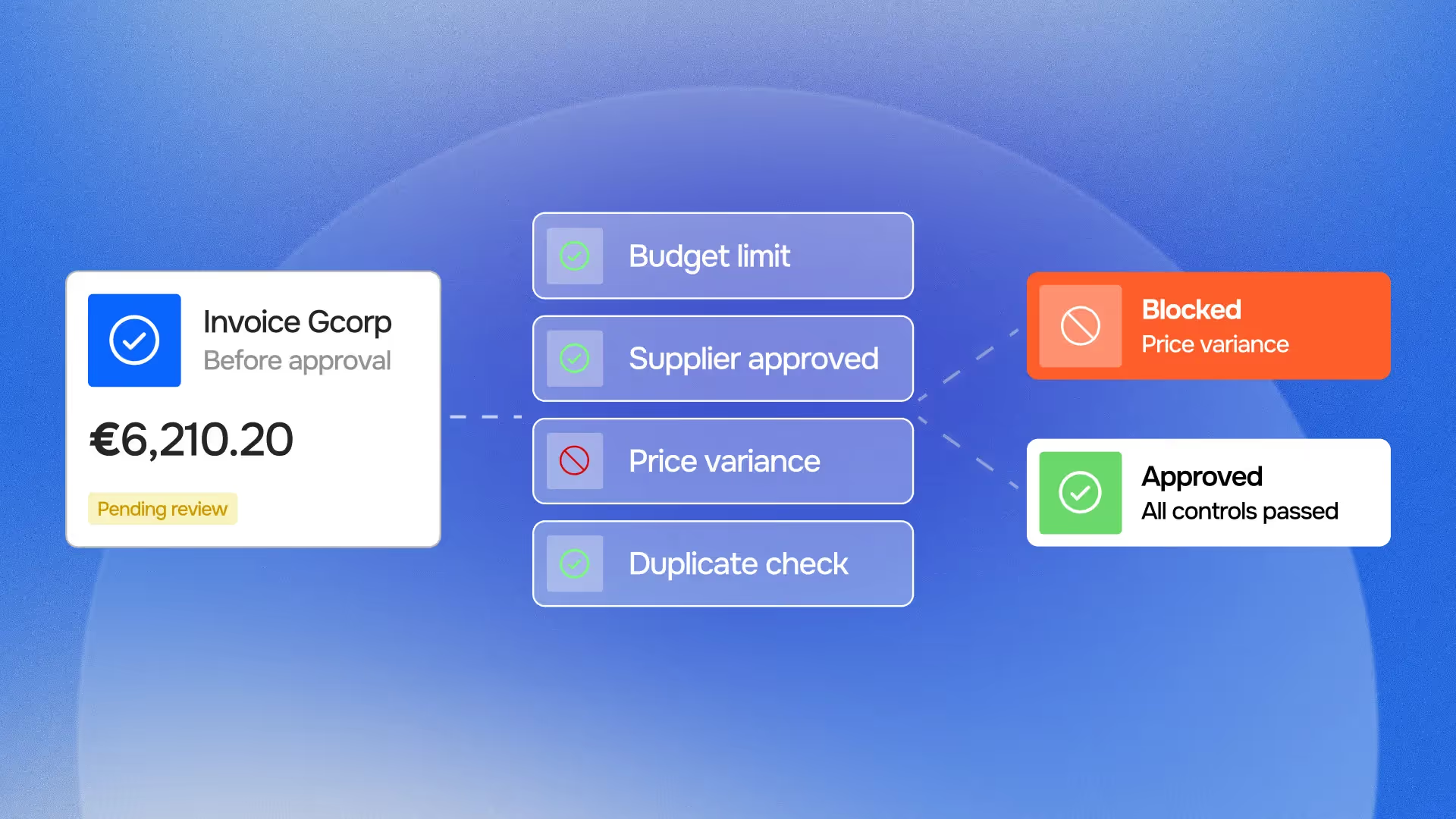

For supplier invoices, this means deploying an AI agent for invoice control that checks every invoice against contracted prices, identifies duplicates, and validates payment terms before the invoice reaches the approval queue. The AP team stops reviewing invoices that are correct and focuses exclusively on the exceptions that the agent surfaces, the price deviations, the duplicates, the invoices with missing PO references.

For bank reconciliation, this means running daily rather than monthly matching of bank transactions against ERP records, surfacing unmatched items within hours rather than accumulating them into a month-end backlog. The bank reconciliation agent does not replace the finance team's judgment about how to resolve unmatched items, it eliminates the work of identifying which items need that judgment.

The Astotel hotel group illustrates the impact: after deploying continuous invoice control with Phacet, their invoice error rate dropped from 7% to 2%, and the finance team's time on AP review was reduced by over 80%. The errors that remained were genuine exceptions, not noise from the control process.

Shift 2: connect controls to approval workflows, not reporting workflows

In a monthly control cycle, the output of controls feeds reporting. Errors found in the month-end review inform the accuracy of the monthly close. The control and the reporting cycle are synchronised.

In continuous pre-decision control, the output of controls feeds approval workflows. When the invoice control agent identifies a price deviation, the deviation blocks the invoice from progressing to payment approval until it is resolved. The control is embedded in the transaction flow, not appended to the reporting flow.

This connection to the approval workflow is what makes the "pre-decision" characterisation accurate. The decision validation layer sits between the transaction and the commitment, structurally positioned to prevent incorrect decisions, not just detect them after the fact.

Embedding controls in approval workflows requires integration with the systems where approvals happen, the ERP, the AP platform, the expense management tool. Phacet's agents connect to these systems through standard integrations, without requiring custom ERP modifications or dedicated IT projects.

Shift 3: standardise exception categories and escalation paths

Monthly reviews handle exceptions in an ad hoc fashion, the AP analyst decides what to escalate and how, based on judgment and experience. Continuous control at transaction volume requires a more structured approach: defined exception categories, defined resolution paths, and defined escalation criteria.

The practical framework distinguishes between exceptions that the agent can resolve automatically (timing differences in bank reconciliation, known classification mappings), exceptions that require AP team action (invoice price deviations below a materiality threshold), and exceptions that require management escalation (deviations above threshold, suspected fraud patterns, supplier master data changes).

This categorisation is what makes exception-based finance review operationally viable at continuous volume. Without it, the finance team receives a continuous stream of exceptions and must triage them manually, replicating the workload problem that continuous control was designed to eliminate.

With it, the finance team's workload is bounded by the volume of genuine exceptions, not the volume of transactions. For most organisations, genuine exceptions represent 3-8% of transaction volume. Continuous control with structured exception management means the finance team handles 3-8% of transactions intensively rather than 100% of transactions superficially.

Shift 4: build continuous control into the closing process, not parallel to it

Monthly closes are frequently extended because the reconciliation that was supposed to happen during the month didn't, and the close is where the accumulated discrepancies get resolved. A finance team that runs continuous reconciliation throughout the month arrives at month-end with a very different starting position: most of the reconciling items have already been resolved, and the close focuses on period-end adjustments and review rather than catching up on a month of unreconciled transactions.

The financial reporting automation benefit of continuous control is not that reporting becomes automatic, it is that the data that feeds reporting is continuously validated, so the preparation work for each close is a fraction of what it would be if reconciliation had accumulated for a full month.

Organisations that have implemented continuous reconciliation consistently report a 40-60% reduction in close preparation time, not because the close process itself changed, but because most of the work that used to happen at the close now happens continuously throughout the month.

Shift 5: make the control record the primary output, not the summary report

In a monthly control model, the primary output is the month-end report, the summary of what was checked, what was found, and what was corrected. The underlying control record (the spreadsheet, the emails, the approvals) is a working document that may or may not be retained.

In continuous control, the primary output is the transaction-level control record, the documented evidence that every transaction was checked, how it was checked, and what happened as a result. The summary report is derived from the control record, not the other way around.

This inversion matters for data governance and audit readiness. An organisation that can produce a complete, timestamped control record for every transaction processed in a period is in a fundamentally different audit position than one that can produce a summary report of the checks performed on a sample.

What changes for the finance team and what doesn't

The transition to continuous pre-decision control is sometimes described as automating the finance team's work. This is an inaccurate characterisation that creates unnecessary resistance to what is, in practice, an elevation of the team's role.

What continuous control automates is the detection work, the task of identifying which transactions in a large population contain errors or anomalies. This is the work that consumes the majority of the time in monthly review processes: scanning invoice line items looking for discrepancies, comparing bank transactions against ledger records, reviewing expense claims line by line.

What continuous control does not automate is the resolution work, the judgment calls about how to handle a specific exception, the supplier conversation about a disputed invoice, the management escalation for a pattern that requires a policy decision. These are the activities that benefit from human expertise, relationship context, and situational judgment. Human-in-the-loop control is not a compromise in the system design, it is where the finance team's value is concentrated.

In practice, finance teams that have transitioned to continuous control describe the operational change as a shift from detection to resolution. Before: "I spend Tuesday reviewing last month's invoices looking for problems." After: "I spend Tuesday resolving the specific problems that the agent surfaced this week." The total time on invoice review typically decreases by 70-80%. The proportion of that time spent on genuine judgment calls typically increases from around 20% to nearly 100%.

The AI agents for finance teams article covers this role evolution in depth. The important point here is that continuous control does not reduce the finance team, it concentrates its effort on the work that actually requires human expertise, while automating the work that doesn't.

The implementation path: where to start

The transition from monthly checks to continuous pre-decision control does not require replacing existing systems or running a multi-year transformation programme. Most organisations implement it incrementally, starting with one control domain and expanding based on the results.

A practical starting sequence:

Week 1-3 - Connect and baseline.

Connect Phacet to the two or three systems most relevant to the priority control domain (typically the ERP, the invoice ingestion channel, and the banking portal). Run the continuous control agents in shadow mode, processing transactions and generating exceptions without blocking any approvals. This baselining phase reveals the actual exception rate in the current population, which is typically higher than the monthly sampling process indicated.

Week 4-6 - Activate exception routing.

Connect the exception output to the AP team's review workflow. Establish exception categories and resolution paths. The AP team begins handling continuous exceptions rather than monthly batches, typically with a significantly lower workload per transaction, because the exceptions are already categorised and the relevant context is pre-populated.

Month 2-3 - Embed in approval workflows.

Configure the pre-decision control layer to block invoices with unresolved exceptions from progressing to payment approval. This is the point at which the control becomes genuinely pre-decision rather than parallel-to-decision.

Month 3-6 - Expand to additional control domains.

Apply the same approach to bank reconciliation, expense controls, or intercompany reconciliation, depending on priority. Each additional domain follows the same connect-baseline-activate-embed sequence.

Phacet's no-code finance automation approach means this implementation sequence does not require dedicated IT resource or ERP customisation. The configuration is handled through Phacet's agent builder interface, with standard connectors to common ERP and banking platforms.

For finance leaders considering this transition, the implementing AI in finance guide covers the strategic sequencing and change management dimensions in detail.

FAQ

What is continuous finance control and how does it differ from monthly checks?

Continuous finance control is a control architecture where every transaction is checked against defined rules and reference data as it occurs, rather than in batched periodic reviews. Monthly checks validate a sample of transactions after a period has closed and the decisions have been made. Continuous control validates 100% of transactions before the decisions are committed, before payment, before approval, before booking. The difference is not just frequency: it is the position of the control relative to the decision it is designed to protect.

Is continuous finance control the same as real-time monitoring?

They overlap but are not identical. Real-time monitoring typically means dashboards and alerts that surface data as it changes, it is observational. Continuous finance control includes monitoring but adds a validation layer: every transaction is compared against contracted prices, reference data, and control rules, and exceptions are routed to a defined resolution workflow. The distinction matters for the pre-decision requirement: a dashboard that shows a discrepancy after the payment has been made is real-time monitoring. A control that blocks the payment until the discrepancy is resolved is pre-decision control.

What does "human-in-the-loop" mean in continuous control?

Human-in-the-loop means that the automated control agents do not make final decisions, they make recommendations and surface exceptions that require human review. The agent identifies that invoice line 3 is priced 12% above the contracted rate and flags it as an exception requiring resolution before payment approval. The AP analyst reviews the exception, contacts the supplier if necessary, and makes the resolution decision. The agent handles the detection; the human handles the judgment. This model applies to all genuine exceptions, the agent does not approve or reject payments autonomously.

How does continuous pre-decision control affect the monthly close?

It significantly reduces the preparation workload. Most of the reconciliation work that typically accumulates in the close, matching bank transactions, resolving invoice discrepancies, clearing open items, has already been handled continuously throughout the month. The close focuses on period-end adjustments, review of the exception resolution record, and preparation of the financial statements, rather than catching up on a month of unreconciled transactions. Finance teams consistently report 40-60% reductions in close preparation time after implementing continuous reconciliation.

Which transaction types benefit most from continuous pre-decision control?

The highest-value applications are typically: supplier invoice control (price compliance, duplicate detection, 3-way matching), bank reconciliation (matching bank movements to ERP records, detecting unmatched items), and expense control (policy compliance, duplicate claims, approval routing). For SaaS and subscription businesses, revenue and billing reconciliation, ensuring that CRM, billing platform, and accounting records are consistent, is a fourth high-value domain. The priority sequence depends on the organisation's transaction volumes and the materiality of errors in each domain.

Can continuous control be implemented without replacing existing systems?

Yes. Phacet's agents connect to existing ERP, banking, invoice management, and expense systems through standard integrations, they do not replace any existing system. The agents sit as a control layer between data ingestion and decision points, operating on the data that flows through existing systems rather than requiring those systems to be replaced. Implementation typically takes three to six weeks using Phacet's no-code configuration interface, without dedicated IT project resource.

What is the ROI of moving to continuous pre-decision control?

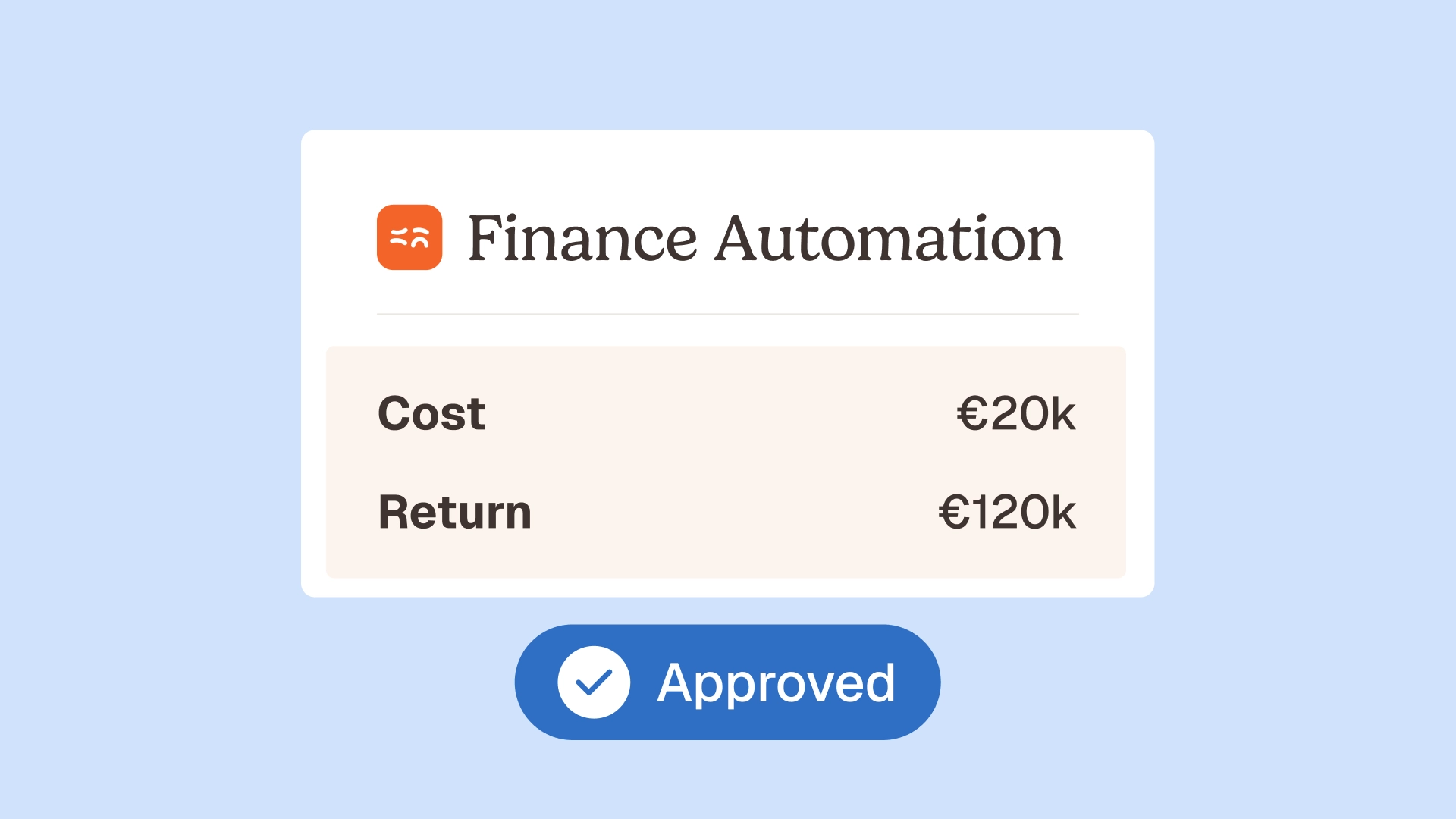

The ROI comes from three sources: direct error prevention (the incorrect payments intercepted before being made, quantified as the sum of price deviations and duplicates blocked at the pre-payment stage), time savings (the reduction in AP and finance team time on manual review, typically 70-80% in the controlled domains), and close efficiency (the reduction in close preparation time, typically 40-60%). For a mid-sized organisation processing 2,000 invoices per month with a 3-5% error rate, the direct error prevention alone typically covers the cost of implementation within the first quarter.

From calendar control to transaction control: the practical shift

Monthly checks are a tool for managing a resource constraint that no longer exists. They were the right answer when checking every transaction required a human analyst for every transaction. They are the wrong answer when AI agents can check every transaction continuously, at a fraction of the cost, with complete documentation.

The shift to continuous pre-decision control is not a transformation project, it is an operational upgrade. The same control objectives, applied at a different point in the transaction lifecycle, with complete coverage rather than partial sampling, and with documentation that builds itself rather than requiring reconstruction.

Phacet's finance control agents implement this upgrade across the domains where pre-decision control matters most: supplier invoice control, bank reconciliation, 3-way matching, cash flow labelling, and accounting inbox management. Each agent connects to your existing systems, processes transactions as they occur, surfaces genuine exceptions for human review, and generates a complete audit trail by design.

The finance team that runs this system does not do less work, it does different, more valuable work. Detection is automated. Resolution is human. Control is continuous. Book a demo to see what continuous pre-decision control looks like applied to your transaction environment.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.