How to shorten month-end close without increasing risk

Published on :

April 16, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

Every finance team that has tried to shorten its close cycle has discovered the same tension: the fastest way to close sooner is to skip steps, and skipping steps means accepting errors. Compress the bank reconciliation. Defer the AP exception review. Use preliminary figures for the cut-off rather than waiting for the billing reconciliation to complete. The close finishes in four days instead of eight, and three weeks later, a restated figure, an audit observation, or a management decision made on incorrect numbers reveals what the speed cost.

The question "how do we shorten the close?" is the wrong question. It presupposes that the close itself is where the time is spent, and that speed means doing the same work faster. The right question is: "how do we reduce the work that has to happen at close?" That is a different problem, with a different solution, and critically, one that shortens the close without touching the controls that make the numbers trustworthy.

This article maps the specific actions that reduce close duration by eliminating deferred work, not by compressing or bypassing the validation that the close requires.

The speed-risk trade-off Is false, but only if you reframe the problem

The conventional wisdom on close acceleration is that it requires accepting some additional risk. Move faster, catch fewer errors. The organisations that have genuinely shortened their close cycles to three days or fewer without restatements or audit findings have done something different: they moved work out of the close window rather than removing work from the close process.

There are two distinct ways to shorten a close:

Acceleration means doing the same closing tasks faster, with better tools, more people, or more efficient workflows. This can reduce close time by a day or two, but it does not change the volume of work arriving at the close. A bank reconciliation tool that processes transactions faster still has to process all thirty days of unmatched items. A better AP review workflow still has to review all the invoices that accumulated during the month. Acceleration reaches a limit quickly, and pushing past that limit means skipping validation steps, which is where the risk enters.

Elimination means ensuring that work does not accumulate for close in the first place. A bank reconciliation that runs continuously throughout the month has only two to three days of transactions to process at close, not because it runs faster, but because it has been running all month. An AP subledger that is validated continuously arrives at close already clean, not because the review is faster, but because it happened throughout the period. Elimination does not trade speed for risk. It removes the deferred work that was both the cause of the long close and the source of the residual risk.

The finance teams that close in three to four business days do not have faster close processes. They have less close-time work, because the validation happened upstream, continuously, during the period.

Why most close acceleration efforts fail

Before mapping the elimination approach, it is worth understanding why the more common acceleration efforts consistently underdeliver.

ERP upgrades and reporting tools improve the speed at which data is extracted and formatted for reports. They do not reduce the volume of reconciliation exceptions, manual journal corrections, or intercompany mismatches that must be resolved before the numbers are presentable. The close is not slow because report generation is slow. It is slow because the underlying data requires significant reconciliation and correction before it can be reported on.

Larger close teams or extended hours add capacity to the close window but do not reduce the work entering it. A team of six can work through a month's backlog of reconciliation exceptions faster than a team of three, but the exceptions still exist, the investigation quality still degrades with volume and time pressure, and the risk of residual errors in the final figures does not materially decrease.

Close checklists and project management tools improve coordination and ensure tasks don't fall through the cracks. They do not change what the tasks are. A well-managed ten-day close with a comprehensive checklist is still a ten-day close.

"Soft close" approaches, accepting some reconciling items as immaterial and deferring resolution to the following period, do reduce close time, but they do so explicitly by accepting that some data quality problems will carry over. This is the archetype of the speed-risk trade-off: the close is shorter because less has been verified, and the numbers carry more residual uncertainty.

The elimination approach is different from all of these because it does not attempt to do close-time work more efficiently. It removes the conditions that create close-time work, specifically, the accumulation of unvalidated data during the period that arrives at the close as a backlog requiring urgent resolution.

5 actions that shorten close by eliminating deferred work

Each of the following actions addresses a specific category of work that typically accumulates during the month and creates close-time pressure. They are not process improvements within the close, they are changes to what happens during the period that determine what arrives at the close.

Action 1 - Run bank reconciliation daily, not monthly

Bank reconciliation is the foundational close task: everything else depends on a validated cash position. When bank reconciliation has been deferred throughout the month, the close-day task is to match thirty days of bank movements against thirty days of ERP records simultaneously, a task that takes two to four days and produces a backlog of exceptions with degraded investigation context.

Running bank reconciliation daily, or continuously, means that the close-day task covers only the last two to three days of transactions. The total close-time bank reconciliation work is reduced by 85-90%. The exceptions that remain are recent, well-documented, and straightforward to resolve.

The bank reconciliation automation approach Phacet deploys matches every incoming and outgoing bank transaction to its ERP counterpart as it settles. By close day, the only open items are those within the current settlement window. The agent for reconciling bank transactions and detecting unmatched flows implements this pattern, not as a faster month-end batch, but as a continuous matching process that leaves nothing to accumulate.

The time saving at close is four to six hours for a typical mid-sized organisation with significant transaction volume. More importantly, the residual exceptions at close are timing differences rather than mystery items, they carry less risk, resolve faster, and require less investigative effort.

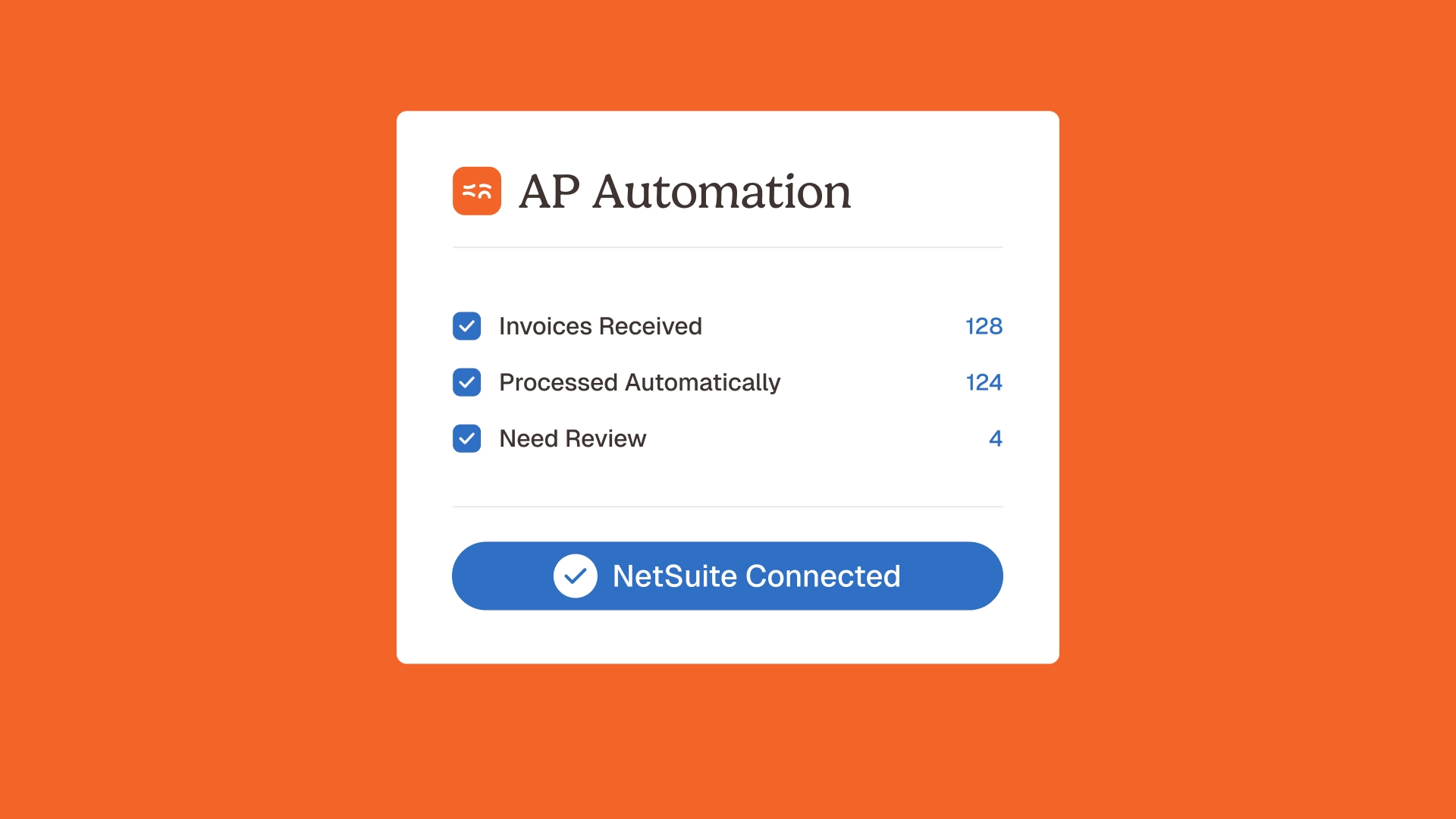

Action 2 - Validate invoices continuously, not at close

The AP subledger review is one of the most time-consuming close tasks, and the one with the most consequential cascade effects: an AP error discovered at close triggers a correction that changes the accrual calculation, which changes the P&L, which requires preliminary cost centre reports to be regenerated.

When invoice validation runs continuously throughout the month, checking each invoice against contracted prices, confirming three-way matching against purchase orders and delivery records, detecting duplicates at point of entry, the close-day AP task is a narrow confirmation that the continuous process worked correctly. The subledger entering the close is already clean.

Invoice control before payment is the practice that makes this possible. Pre-payment controls applied to every invoice as it arrives, not to a sample at month-end, eliminate the category of AP subledger errors that generate close-time cascade effects. The supplier billing control agent and the accounting inbox agent together implement this continuous AP validation, ensuring that the invoice population reaching the close has already been validated for price compliance, completeness, and duplicate status.

Astotel's experience after deploying Phacet's continuous AP validation: invoice error rate from 7% to 2%, and close-time AP review compressed to a fraction of the previous duration, not because the review process changed, but because there were far fewer errors to find.

Action 3 - Standardise accounting data classification throughout the period

A significant proportion of close-time manual journal volume comes not from transaction errors but from classification inconsistencies: transactions that were correctly processed but posted to the wrong account, cost centre, or category label. Reclassification entries at close are among the most time-consuming to trace and correct, because each one affects at least two accounts and may cascade through cost centre reports, management accounts, and sub-ledger reconciliations.

Classification errors accumulate when accounting data is processed through multiple systems with inconsistent chart of accounts mappings, or when manual categorisation decisions vary between the people processing similar transactions. The close cannot correct these at source, it can only re-categorise, which does not prevent the same errors in subsequent months.

The agent for standardising and reclassifying accounting data at scale applies consistent classification logic at the point of transaction processing, not at close. Data normalisation and data labeling applied continuously means that the data entering the close carries consistent classification across all systems and entities. The close-time reclassification workload disappears not because it runs faster, but because it has already been done, correctly, at source, throughout the period.

For organisations operating across multiple entities with different charts of accounts, the data alignment across systems layer that maintains classification consistency across entities is what makes the intercompany elimination at close tractable. Consistent classification during the period means that intercompany transactions match on both sides without the manual reclassification adjustments that typically extend the close by one to two days.

Action 4 - Build the accrual estimate from validated data, not working memory

Month-end accruals, provisions for expenses incurred but not yet invoiced, are among the most error-prone close tasks because they combine estimation (predicting the value of uninvoiced obligations) with data quality dependence (the estimate's accuracy depends on how much of the period's actual spend has been reliably captured).

When the AP validation has been running continuously during the period, the accrual estimate has a clean foundation: the actual spend recorded in the subledger is accurate, the open purchase orders represent committed but uninvoiced spend correctly, and the estimate for goods received but not invoiced (GRNI) is built on confirmed delivery records rather than assumptions.

When AP validation has been deferred to close, the accrual estimate is being built on top of a subledger that may contain unresolved errors, price deviations, unmatched deliveries, uncaptured invoices. The estimate is compounding uncertainty on top of uncertainty.

The practical implication is that actions 1 and 2 above, continuous bank reconciliation and continuous AP validation, are prerequisites for a reliable, lower-effort accrual process at close. The accrual is not shortened independently; it is shortened as a consequence of the upstream data being clean when the accrual estimate is made.

For organisations with significant contract obligations, the agent for extracting key terms from contracts at scale ensures that the contracted obligation data feeding the accrual, payment schedules, volume commitments, renewal terms, is current and correctly reflected in the systems used to prepare the estimate. Accrual errors driven by contracts whose terms haven't been correctly captured in the ERP are a common source of close-time corrections that this addresses directly.

Action 5 - Automate cash flow and transaction labelling for treasury reporting

The treasury reporting component of the close, confirming the cash position, classifying cash movements for the cash flow statement, validating the bank position against the ERP, is a task that many finance teams still complete manually, working through bank statement lines and assigning categories against the chart of accounts.

This labelling and classification work is typically one of the first tasks in the close sequence (because treasury reporting feeds other close tasks) and one of the most tedious, not because it requires difficult judgment, but because there is a large volume of routine categorisation to work through before the genuinely ambiguous items become visible.

The agent for automatically labelling cash movements to prepare treasury dashboards applies this classification continuously throughout the month, using learned categorisation logic to assign each bank movement to the correct cash flow category as it occurs. By close day, the cash flow statement components are already classified, the close-time treasury task is reviewing the edge cases and confirming the totals, not working through the full population.

Combined with continuous bank reconciliation (action 1), this means the close-time treasury workload, which for many organisations represents a full day of close time, compresses to a two to three hour review of the exceptions and confirmations.

The risk profile: why eliminating deferred work reduces risk, not just time

The intuitive concern about shortening the close is that speed trades against thoroughness. If the close takes less time, presumably less has been checked.

The elimination approach inverts this logic completely. The close takes less time because more has already been checked, during the period, at the point of transaction, with better context and lower correction cost. The close window itself contains only confirmation and edge-case resolution, not the bulk discovery and correction work.

Under the elimination approach, the risk profile at close is lower than under the deferred validation model, even though the close is shorter. The reasons are structural:

Higher coverage. Continuous validation covers 100% of transactions throughout the period. Monthly close reviews cover a sample. The errors that reach the close under continuous validation are genuine exceptions that the continuous process identified and routed for resolution, not the statistical residual of a sampling approach.

Better context for resolution. Exceptions identified within days of a transaction carry more context than exceptions identified thirty days later. The bank item that didn't match last Thursday is straightforward to investigate. The bank item that didn't match on the third of the month, three weeks ago, may require reconstructing the circumstances from memory and incomplete documentation.

No cascade amplification. Under the deferred validation model, a single error discovered at close can cascade: an AP correction changes an accrual, which changes the P&L, which invalidates preliminary reports. Under continuous validation, corrections happen during the period when their scope is narrow, a single transaction corrected individually, with no downstream reports depending on it yet.

Complete audit documentation by construction. The audit trail generated by continuous validation agents covers the full transaction population, timestamped and linked to source documents. This documentation exists before the close begins, it is not assembled during the close under time pressure. The audit-ready finance processes posture is maintained throughout the period, not reconstructed at close or during audit preparation.

The finance team that runs a four-day close using continuous pre-validation does not take on more risk than the team running an eight-day close using periodic validation. It takes on less, because the data entering the close has been validated more thoroughly, with better context, across the full transaction population, with complete documentation. The difference in duration reflects the difference in upstream work done, not a difference in control quality.

This is the core principle of continuous finance control: a shorter close is a consequence of better controls during the period, not a replacement for them.

Implementation Sequence: Where to Start

Finance teams that have successfully shortened their close cycles without increasing risk typically follow a similar sequencing logic: start with the highest-volume, highest-cascade-risk task, validate the impact, then expand.

Month 1 - Continuous bank reconciliation. Connect the bank feeds to the reconciliation agent and run daily matching. This is the fastest to implement (typically one to two weeks of configuration) and the most visible in terms of close impact. The close-time bank reconciliation task compresses immediately in the first cycle after deployment. Baseline the time saving before moving to the next domain.

Month 2 - Continuous AP invoice validation. Deploy the invoice control and accounting inbox agents. Configure the exception categories and resolution workflows. This takes slightly longer to configure (three to four weeks) because it requires connection to both the invoice ingestion channel and the ERP's purchase order records. The close-time AP review compresses in the first full cycle. The accrual estimate improvement follows as a secondary effect.

Month 3 - Accounting data standardisation. Deploy the classification and reclassification agent. This requires mapping the target classification scheme across all connected data sources, a configuration step that takes two to three weeks but produces permanent close-time savings in the reclassification and intercompany elimination workloads.

Month 4 - Cash flow labelling and treasury automation. Deploy the cash movement labelling agent, configured for the organisation's cash flow statement categories. The treasury close task compresses in the first cycle.

By month four, the five actions described above are operating continuously. The close workload has been reduced by the cumulative effect of each domain, and the total close duration is typically three to four business days, compared to eight to twelve before the programme began.

Phacet's no-code automation platform makes this sequencing practical without dedicated IT resource. Each agent connects to existing systems through standard integrations, configured through Phacet's agent builder interface rather than custom ERP development. For a comprehensive view of how this implementation fits into a broader finance automation programme, see the AI financial data automation and end-to-end transparency article and the AI purchase-to-pay automation piece, which covers the AP workflow integration in detail.

FAQ

What is the fastest way to shorten month-end close without increasing risk?

The fastest risk-free path is daily bank reconciliation, it can be deployed in one to two weeks, produces an immediate and measurable reduction in close-time bank reconciliation work, and carries no additional risk because it is covering the same transactions more frequently rather than skipping any. The cumulative impact of adding continuous AP validation, classification standardisation, and cash flow labelling in subsequent months typically delivers a total close reduction of four to six business days over a three to four month implementation sequence.

Is it possible to close in three to four days without accepting more risk?

Yes, but only through the elimination approach rather than acceleration. Organisations that close in three to four days reliably have moved the bulk of validation and reconciliation work to the period rather than the close window. The close itself contains confirmation tasks (verifying that the continuous validation worked correctly) and edge-case resolution (the genuine exceptions that couldn't be resolved automatically). The data quality of the resulting financial statements is higher than in an eight-day close that uses periodic validation, because more of the transaction population was checked, with better context, before the close began.

Why does adding more people to the close team not reliably shorten the close?

Adding close-team capacity helps when the close is constrained by review bandwidth, the team can't process the exception volume fast enough. But for most organisations, the close is constrained by resolution complexity, not review bandwidth. A large backlog of bank exceptions, AP errors, and intercompany mismatches takes time not because there aren't enough people to look at them, but because investigation and correction require context that degrades with time, cascade tracking that requires sequential iteration, and manual journal volume that propagates through the trial balance. More people speed up the review; they don't simplify the investigation or eliminate the cascades.

How does continuous AP validation affect the quality of month-end accruals?

Continuous AP validation improves accrual quality by ensuring that the subledger position on which the accrual is based reflects validated transactions rather than a mix of validated and unreviewed items. When every invoice has been checked against contracted prices and delivery records before entering the subledger, the "goods received not invoiced" (GRNI) estimate is built on confirmed receipt records and a clean subledger, not on a partially validated data set with unknown error distribution. The accrual is more accurate and takes less time to prepare, because the foundation is clean.

What does human-in-the-loop control look like in a shortened close?

In a shortened close supported by continuous pre-validation, human review concentrates on genuine exceptions rather than routine scanning. The close team reviews the bank exceptions the reconciliation agent identified as requiring judgment (ambiguous descriptions, missing documentation), the AP exceptions the invoice control agent flagged as needing resolution (price disputes, missing PO references), and the classification edge cases that couldn't be resolved by the standardisation logic. This is more intensive, more consequential work than routine scanning, and it is what the close team should be doing. The volume is lower; the quality of judgment applied per item is higher.

How does shortening the close affect external audit preparation?

A close supported by continuous validation generates audit documentation as a by-product of the control process, not as a separate preparation exercise. The audit trail covering every transaction processed during the period, with timestamps and resolution records, exists before the audit begins. External auditors can trace any transaction to its source document, the validation performed, and the resolution path taken, without the finance team needing to reconstruct this information. Audit preparation time typically decreases in parallel with close preparation time, because both are downstream benefits of the same continuous validation infrastructure.

A shorter close is proof of better controls, not fewer

The finance team that closes in three days has not cut corners. It has front-loaded the validation work that the close requires, spreading it across the full period at the point where context is richest, correction costs are lowest, and coverage can be complete rather than sampled.

The eight-day close is not more rigorous. It is more compressed, all the same validation work, done under worse conditions, with higher residual error risk and less time to catch the cascade effects before the deadline.

Shortening the close without increasing risk is not a process optimisation question. It is a question of when and how validation happens, and whether the finance function has the infrastructure to move that validation upstream, into the period, where it belongs.

Phacet's continuous validation agents, bank reconciliation, AP invoice control, accounting data standardisation, cash flow labelling, and customer cash-in reconciliation, implement this infrastructure across the domains where close-time work accumulates. The close becomes shorter because the month becomes more controlled. Book a demo to map which domains are driving your current close duration and what the elimination approach looks like for your transaction environment.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.