How to build an internal business case for finance automation

Published on :

July 6, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

At Astotel, a group of 18 Paris hotels, supplier price checks used to run on sampling. Then a Phacet agent surfaced 400€ of billing errors a month on a single supplier, close to 5,000€ a year. The agent checks every invoice line against negotiated prices, shows its reasoning at each step, and flags the gap before payment goes out. "I catch mistakes I would never have spotted on my own." (Valerie, Head of Purchasing.)

That one number is also the key to a finance automation business case that actually gets approved. Most of them never do, and the reason is almost always the same: they are built on the wrong number.

In short: to build a finance automation business case that wins budget, quantify the money your manual process leaks before payment (price drift, duplicates, mismatches, fraud), make that recovered cash your headline figure, then layer time savings underneath. Control is the line a CFO cannot argue down. Efficiency is the line they discount.

What is a finance automation business case?

A finance automation business case is the internal document a finance leader uses to justify investing in software that automates manual finance work, such as invoice processing, three-way matching, reconciliation and controls. It connects a current operational problem to a financial return, then asks for a decision: budget, sponsorship, or the go-ahead to choose a vendor.

A complete case usually covers five angles, the same five the UK Treasury Green Book uses to assess any investment: strategic (why now), economic (what value), commercial (what you buy), financial (what it costs and returns), and management (how you deliver it). You do not need a 40-page template to cover them. You need one defensible number and a plan to deliver it.

For finance leaders, the hard part is rarely the math. It is choosing the number that survives contact with a skeptical CFO.

Why most finance automation business cases fail to get approved

Most cases fail because they lead with efficiency: hours saved, cost per invoice cut, headcount avoided. On paper it looks compelling. In the room, a CFO discounts it almost on reflex.

The reason is simple. Reclaimed hours are soft. Nobody gets laid off when an agent saves the team 1,300 hours a year, so those hours quietly get reabsorbed into other work. The "saving" never shows up as cash on the profit and loss statement. A sharp CFO knows this, which is why a case built only on time savings gets nodded at and shelved.

The second failure mode is the rip-and-replace pitch. Many vendors end their business case with "migrate to our ERP." For a goods business running several disconnected systems, a 500K€ migration is a non-starter, and tying automation to it kills the proposal before the numbers are even read.

Both problems have the same fix: change the number you lead with.

The number that wins the room: money recovered before payment

Here is the return on AI in finance that a CFO cannot wave away: the cash your process recovers and protects before it leaves the company. Overpayments caught by line-level price checks. Duplicate invoices stopped before a second payment runs. PO and invoice mismatches corrected. Fraudulent bank details flagged before a transfer.

This is what "control before payment" means, and it is the part every competing business case leaves in the footnotes as a "soft benefit." It is not soft. The overpayment was real. The duplicate was real. The 3,000€ of price drift across a year was real. You are not projecting capacity, you are recovering money.

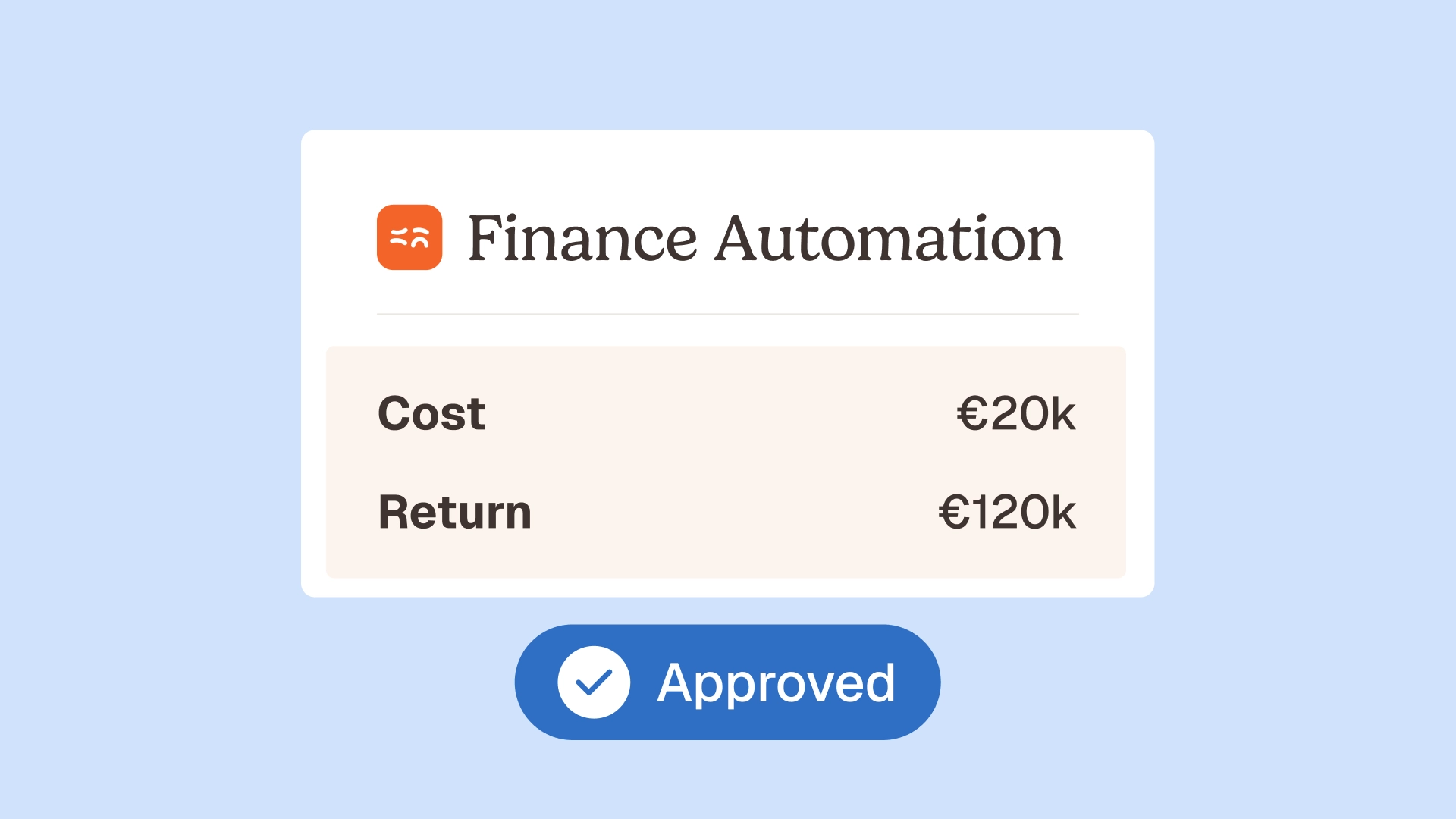

The framing matters. At Astotel, the headline was not "two hours saved a day," even though that happened too. The headline was 5,000€ recovered on one supplier, found by an agent checking invoice price compliance line by line. One is a productivity story. The other is a number the board acts on.

This is also where finance automation stops being generic. An agent that enforces pre-payment controls sits in the internal controls layer, which is where the real, defensible savings live, not in faster data entry alone.

Which control leaks can you actually put a number on?

You can quantify more than you think. Each leak below maps to a real line in your accounts payable, a method to value it, and an agent that closes it. Pull twelve months of invoices and the numbers come out fast.

A few notes on method. For price drift, run line-level price compliance against your negotiated terms and sum the overcharges by supplier. For double payments, duplicate invoice detection across channels and entities gives you a count and a value. For mismatches, 3-way matching exceptions multiplied by the average overbilled amount is your number. For fraud, the Association of Certified Fraud Examiners puts the typical loss at around 5% of revenue a year, a benchmark you can apply conservatively alongside your own incident history.

Each of these produces a figure you can defend. Stack them and you have the headline of your business case.

How to build the business case, step by step

Work in this order. The sequence is deliberate: control first, efficiency second, costs honest, and the CFO framing last.

- Quantify the control leak first. Use the table above. Total the recoverable and protectable cash across price drift, duplicates, mismatches and fraud exposure. This is your headline number.

- Layer the efficiency savings underneath. Now add reclaimed time, valued at fully loaded hourly cost, but discount it. Present it as a secondary benefit, not the headline. This signals to the CFO that you know which number is hard and which is soft.

- Build an honest total cost of ownership. Include the platform, scope, any integration work and internal change effort across three years. Underselling cost destroys credibility faster than a high number does.

- Calculate ROI and payback. Lead with the headline outputs a CFO reads first: annual benefit, payback period in months, and three-year return. Keep the assumptions conservative so the numbers hold up under questioning.

- Frame it for the decision-maker. Open with the outcome, not the problem. One line: "This recovers X in hard cash, pays for itself in Y months, and tightens control as we grow." Then show the current state, the future state, and the rollout.

The structure mirrors how senior leaders actually read a proposal: headline numbers first, evidence second, plan third.

A worked example: what the numbers look like

Numbers make it concrete. The example below is built for a mid-size goods business, the kind of 50 to 500 person company in food and beverage, hospitality, retail or construction where invoices flow in volume across several systems.

Notice the shape. Control delivers 60,000€ of hard cash, efficiency adds 30,000€ on top, and the investment pays back in under three months. The control lines carry the case. That is exactly the proof point that survives a tough budget meeting, and it is the opposite of a case built on hours alone.

Real deployments behave the same way. Smartbox, the European gift-experience leader with 800 employees across 14 countries, saw payment and invoice reconciliation reach four times the productivity, with each use case live in six weeks. La Nouvelle Garde, a group of ten Paris brasseries, recovered two days a week and deferred hires. Fast time-to-value is part of the case, because a short payback de-risks the decision.

How to present it to your CEO or board

Lead with the headline. Open the executive summary with the recovered cash, the payback period and the three-year return, then connect it to a strategic priority such as scaling without adding finance headcount. If you cannot make the case in two minutes, you do not have one yet.

Then prepare for the four objections you will hear.

"What about our people?" Automation augments the team, it does not replace it. The AI proposes, your team decides. Agents take the repetitive checks so your people move from data entry to analysis. Every output is traceable through a native audit trail, so a human stays in the loop and accountable.

"Isn't this just ChatGPT?" General tools are excellent, but they do not know your suppliers, your price lists or your accounting rules, they produce no audit trail, and they do not connect to your inbox or your ERP. A finance agent does, and it was built on real finance deployments.

"Won't it mean a painful migration?" No. This is the strongest answer in the room. Phacet sits on top of your existing ERP and works across systems, so there is no rip-and-replace and no 500K€ project. The first agent runs in production in under two weeks.

"Is it secure?" Data is hosted in Europe, the platform is ISO 27001 certified and GDPR compliant, and client data is never used to train the models.

Have backup slides with the detailed control calculations and a peer example ready. Close by asking for the specific decision you need.

Why you should start with one agent, not a platform rollout

The fastest case to approve is the smallest one. You do not need to automate the whole finance function to prove the point. You need one agent, one leak, one number.

Start where the pain is sharpest and the money is clearest. For most goods businesses that is supplier control: control supplier billing and reduce overpayments, or stop losing money on supplier mismatches. If the volume sits in the inbox, begin by automating the accounting inbox instead. With plans starting at 299€/month and a first agent live in under two weeks, the entry cost is small enough that the recovered cash funds the next agent.

This is the modular path: prove control on one supplier or one process, show the number, then expand across accounts payable, reconciliation and closing. Each step pays for the one after it. Browse the full catalogue of finance agents to map the sequence to your own leaks.

A finance automation business case is not really about buying software. It is the first step in moving finance from the team that reports on the numbers to the team that protects them, and then uses them. Build the case on control, and the budget follows.

Ready to put a number on your own control leaks? Book a demo and we will help you size them.

FAQ

How do you write a business case for finance automation?

Start by quantifying the money your manual process leaks before payment: price drift versus negotiated terms, duplicate payments, PO and invoice mismatches, and fraud exposure. Make that recovered cash your headline number, then add time savings as a secondary benefit. Build an honest three-year total cost of ownership, calculate payback, and open your presentation with the outcome.

What ROI can you expect from finance automation?

It depends on your invoice volume and control gaps, but control-driven cases often pay back in under six months because recovered overpayments and avoided duplicates are hard cash, not projected capacity. In a typical mid-size goods business, control recoveries alone can outweigh the entire investment in the first year.

What is the difference between efficiency and control in a finance automation business case?

Efficiency measures hours and cost saved on manual tasks, which a CFO tends to discount because freed time rarely converts to cash. Control measures money recovered or protected before payment leaves the company, which lands directly on the profit and loss statement. Control is the defensible headline, efficiency is the supporting benefit.

How long does finance automation take to implement?

With an agent-based platform that sits on top of your existing ERP, the first agent can run in production in under two weeks, with no migration. Additional use cases typically go live in a few weeks each, so payback starts early rather than after a long rollout.

Will finance automation replace the finance team?

No. Finance agents handle repetitive checks and data work so the team can focus on analysis and decisions. The AI proposes and the human decides, and every action is recorded in an audit trail, which keeps a person accountable for each control.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.