Beyond RPA: AI agents reshape finance automation

Published on :

January 13, 2026

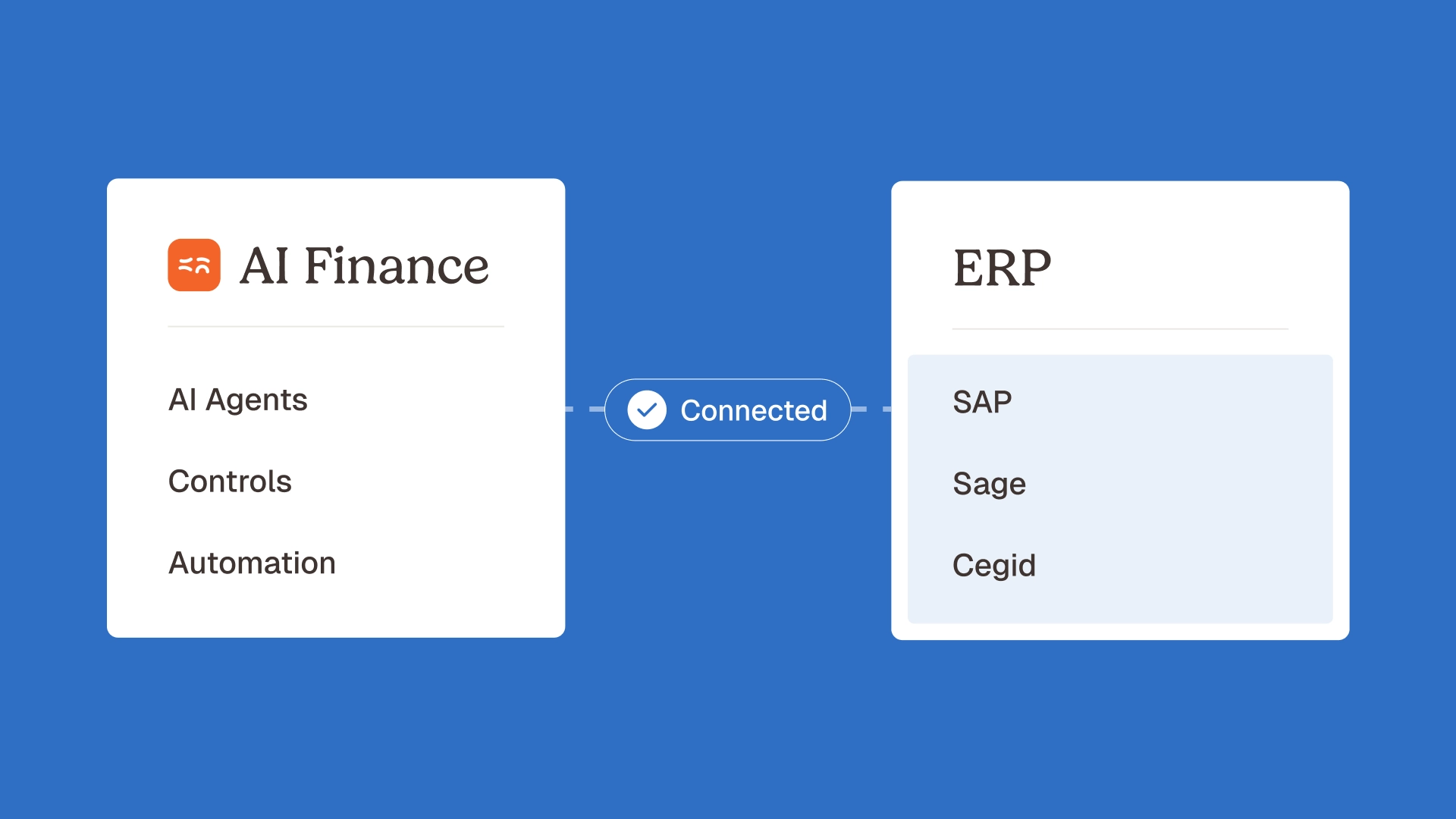

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

The key takeaway: traditional RPA’s rigid, rule-based automation struggles with modern finance’s complexity and hidden costs, while AI agents provide adaptive, context-aware solutions. They reduce manual work with unstructured data (invoices, compliance checks), freeing teams for strategic analysis. Unlike fragile RPA bots, AI agents cut long-term costs by adapting to regulatory/IT changes without reprogramming.

Stuck in endless manual data entry and error-prone workflows that robotic process automation in finance promised to fix but still fall short? This article reveals how modern AI agents are redefining automation by overcoming RPA’s rigid rules and fragile scalability. Discover how finance teams slash operational costs by 40%, automate complex exceptions like unstructured invoice formats or dynamic regulatory updates, and unlock strategic value, drastically reducing human intervention while adapting to evolving regulations, extracting insights from PDFs/emails, and scaling seamlessly across ERP systems. Real-world applications like intelligent 3-way matching and self-learning reconciliation prove automation is no longer just about efficiency, but about reinventing how finance teams operate.

- What is robotic process automation in finance?

- Why traditional RPA is reaching its limits in modern finance

- The shift toward intelligent automation and AI agents

- Key advantages of AI agents over traditional RPA

- Real-world use cases: AI agents in action

- From RPA to AI agents: the next step in finance automation

What is robotic process automation in finance?

Robotic Process Automation (RPA) in finance involves software bots that replicate human actions to handle repetitive, rules-based tasks across existing systems. These bots perform data entry, transaction processing, and report generation with predefined logic, eliminating manual effort in workflows like invoice matching or bank reconciliation. Unlike AI-driven solutions, RPA strictly follows static instructions without adaptive decision-making.

RPA’s value lies in its ability to reduce operational costs by 25–50% while minimizing human errors in high-volume processes. Finance teams use it to automate tasks such as supplier data validation or monthly closing reports, freeing employees for strategic analysis. It ensures consistent compliance by maintaining audit trails and accelerating tasks like regulatory filing. Though transformative in efficiency gains, its rigid framework struggles with complex, evolving scenarios, setting the stage for next-gen solutions. This structured approach laid the groundwork for automation but highlights limitations that modern finance leaders must address.

Why traditional RPA is reaching its limits in modern finance?

Traditional RPA relies on rigid, rule-based logic to automate repetitive tasks in finance. Fragile by design, these systems break when even minor changes occur in user interfaces, such as a button’s position or field name. These bots use screen-scraping techniques that depend on fixed coordinates or pixel positions. A Salesforce update shifting a "Submit" button’s location by 10 pixels can crash bots, forcing teams to spend maintenance hours fixing workflows that should run autonomously.

Financial processes rarely follow a one-size-fits-all format, yet RPA struggles with unstructured data like varied invoice layouts or handwritten notes. When exceptions arise, such as missing fields or conflicting data, the system halts, requiring manual intervention. A global bank processing supplier invoices might find 20% of documents arrive in non-standard formats, creating bottlenecks. This dependency on human oversight undermines automation’s core promise: reducing labor-intensive workflows. Teams end up managing bots instead of focusing on strategic tasks like fraud detection.

Scaling RPA across finance operations reveals hidden pitfalls:

- High maintenance overhead: 70-75% of RPA costs stem from upkeep, not software licenses. A 50-bot deployment might require 250+ weekly hours to repair broken workflows, with 30-50% of projects failing to move beyond pilot phases.

- Lack of adaptability: Regulatory changes or system upgrades demand reprogramming, making long-term scalability costly and slow. Adapting RPA to new IFRS standards might require rewriting hundreds of rules across multiple bots, a process taking weeks.

- Hidden operational costs: Complexity grows exponentially as bots interact across systems, creating cascading failures when one bot malfunctions. A broken reconciliation bot can halt month-end closing for an entire organization.

The shift toward intelligent automation and AI Agents

Intelligent automation represents the next phase in financial process optimization, merging rule-based automation with adaptive intelligence. Unlike RPA’s rigid workflows, this approach integrates machine learning and natural language processing to interpret context, adapt to exceptions, and evolve with new data. The focus shifts from merely replicating human actions to enabling systems that learn, prioritize tasks, and resolve ambiguities autonomously.

AI agents redefine automation by operating as self-directed entities capable of end-to-end process ownership. While RPA bots execute predefined scripts, AI agents leverage real-time data analysis to handle unstructured inputs like handwritten invoices or dynamic supplier contracts. They continuously refine their decision-making through feedback loops, reducing reliance on human intervention. This adaptability is critical for complex financial tasks such as reconciling cross-border transactions or flagging anomalies in audit trails.

The transition from scripted to cognitive automation aligns with finance teams’ need for agile, compliant solutions. Modern AI agent platforms for finance empower users to configure workflows without coding, ensuring rapid deployment as regulations evolve. By embedding human validation at key decision points, these systems maintain transparency while scaling intelligently. This marks a part d'une transformation where financial operations move from reactive fixes to proactive, data-driven strategies.

Key advantages of AI agents over traditional RPA

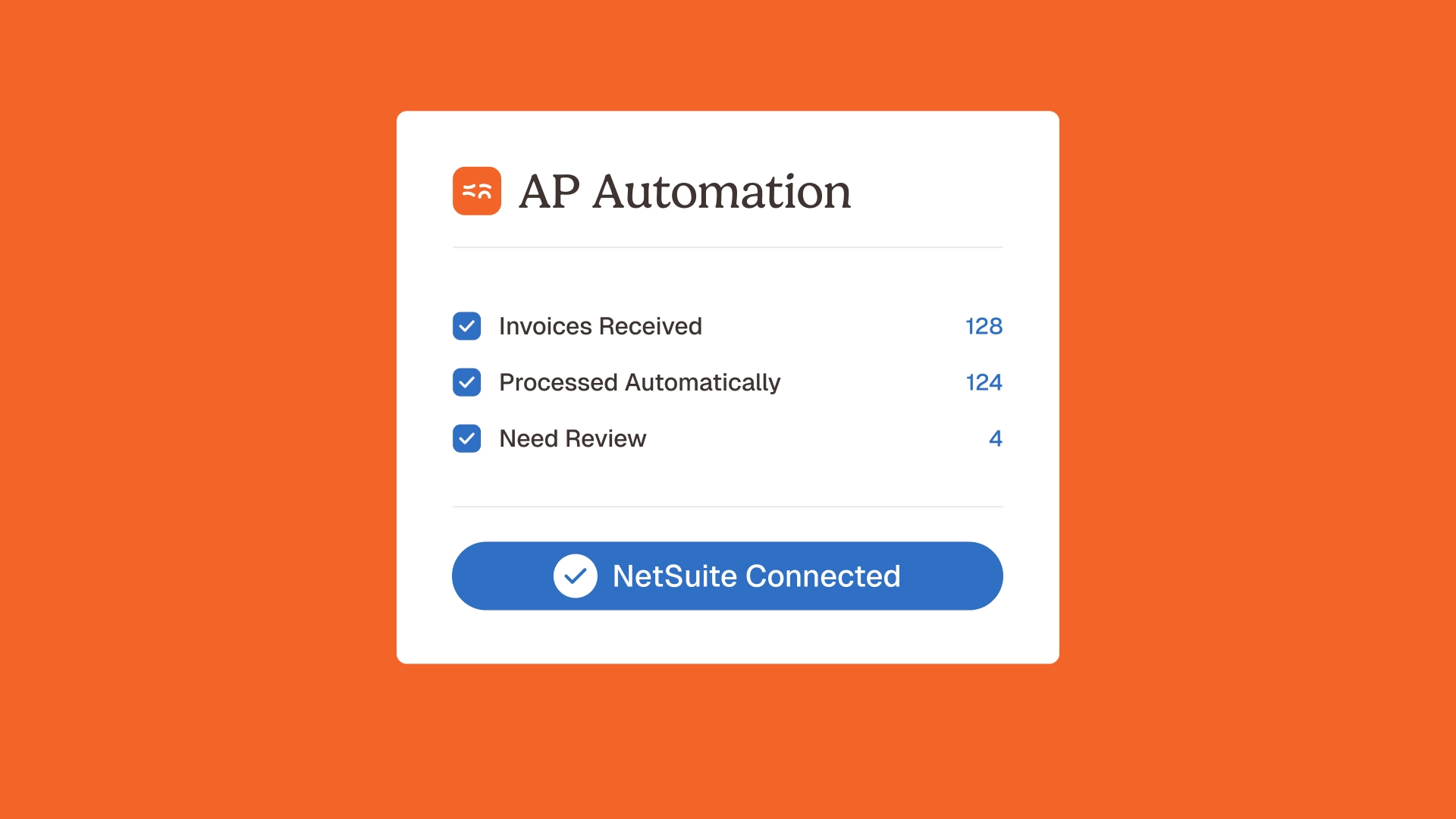

Traditional RPA tools operate through rigid, pre-programmed rules requiring constant maintenance as processes evolve. AI agents, by contrast, use machine learning to adapt dynamically. They refine performance through every transaction and human correction, enabling automation of workflows previously needing manual intervention due to exceptions or shifting data formats. A multinational corporation handling vendor invoices across multiple currencies reduced manual review time by 70% after implementing Phacet’s AI agents, which adjusted to format variations automatically while maintaining compliance with regional tax regulations.

AI agents excel at interpreting unstructured financial data sources like non-standard invoices or handwritten notes. Unlike RPA’s pattern-matching approach, these agents understand context, recognizing that an "invoice total" field might be labeled "amount due" in one document and "total payable" in another. This contextual interpretation extends to mapping invoice line items against purchase orders and contracts, catching discrepancies invisible to rule-based systems. This enables:

- Adaptability: Adjusts to process variations without reconfiguration, handling new document types seamlessly through semantic understanding

- Context awareness: Interprets financial data nuances beyond template recognition, linking invoice line items to purchase orders and contract terms

- Scalability: Processes 10,000+ documents daily while maintaining performance, scaling automatically with cloud infrastructure

Phacet’s AI-first approach integrates human validation via "human-in-the-loop" architecture. While AI handles 95% of tasks like bank reconciliation, exceptions trigger human review. This workflow lets finance professionals focus on strategic decisions while the system learns from each validation. When an accountant corrects a misclassified expense, the AI applies this learning across future transactions, reducing recurrence by 85% within three months. This continuous learning loop ensures compliance with evolving standards like IFRS 18 or ASC 606 without manual rule updates.

Finance teams deploy capabilities through a no-code interface, eliminating IT dependency. With drag-and-drop configuration, controllers set rules for supplier control or journal validation. This empowers direct implementation of solutions like No-Code AI for business workflow automation, accelerating deployment from weeks to days with audit trails intact. A manufacturing company streamlined month-end closing in two days using Phacet’s visual builder, achieving 98% automation for reconciliations that once required manual work, while maintaining Sarbanes-Oxley compliance through built-in validation checkpoints.

Real-world use cases: AI agents in action

Automated bank reconciliation

Traditional RPA tools struggle with minor discrepancies in transaction labels or amounts, often requiring manual intervention. AI agents, however, adapt to variations by learning from past corrections made by finance teams. For example, a slight mismatch in supplier names or decimal places no longer stalls reconciliation. Even inconsistencies in date formats or currency symbols are resolved autonomously. This adaptability drastically reduces manual effort, with the AI refining its accuracy over time. Automated bank reconciliation with AI makes this possible without rigid rule-based systems, enabling month-end closures to accelerate by up to 60% in high-volume environments.

Advanced 3-way matching for invoices

Invoice matching demands comparing purchase orders, goods receipts, and invoices, a process prone to errors with RPA if formats vary. AI agents extract data from any document type (PDF, scanned images) and align fields intelligently, even in unstructured layouts. When minor pricing differences or missing data arise, the AI flags exceptions for human review rather than halting the workflow. 3-way matching automation for finance teams ensures seamless processing while maintaining audit readiness, even when handling handwritten notes or multilingual documents.

- Data Extraction: Captures invoice details from diverse formats without predefined templates.

- Smart Matching: Cross-references invoice data with purchase orders and receipts autonomously.

- Exception Handling: Identifies mismatches and escalates them for targeted resolution.

- System Update: Integrates validated data into ERP systems without manual input.

Supplier control and compliance

Ensuring supplier compliance through KYC/AML checks is resource-intensive when done manually. AI agents automate validation of business licenses, contract terms, and tax documentation, flagging anomalies for human validation. This reduces compliance risks by cross-referencing real-time data against regulatory databases. Continuous learning ensures the system adapts to evolving requirements like GDPR updates or industry-specific standards, providing an auditable trail for regulatory reviews. The result? A 72% reduction in manual verification time, with zero tolerance breaches slipping through. Teams now focus on strategic risk mitigation rather than repetitive checks, while automated reporting ensures up-to-date compliance documentation for audits.

From RPA to AI agents: the next step in finance automation

Robotic Process Automation (RPA) revolutionized finance by automating repetitive tasks, boosting speed and accuracy. However, its rigid, rule-based logic falters with unstructured data, regulatory shifts, or complex risk scenarios demanding adaptability.

AI agents represent a shift from rigid bots to adaptive systems that learn, collaborate with humans, and handle exceptions autonomously. Phacet’s AI-first approach integrates human validation and real-time adjustments via no-code tools, avoiding RPA’s brittleness. This ensures compliance while accelerating deployment.

The future demands finance teams transcend transactional tasks. AI agents shift focus to insights and risk mitigation, creating value beyond productivity. Phacet’s adaptive intelligence transforms finance into a proactive, data-driven force. The question isn’t whether to evolve past RPA, it’s how quickly teams will act.

The shift from robotic process automation in finance to AI agents marks a new era. While RPA streamlined repetitive tasks, its rigidity and maintenance demands limit agility. AI agents, combining contextual understanding and scalability, empower finance teams to focus on strategic decisions. The future merges efficiency and innovation.

FAQ

How is robotic process automation applied in the finance sector?

In financial institutions, RPA centralizes and automates repetitive tasks that employees traditionally handled manually. Bots simulate human actions like data entry, clicks, and system navigation, following predefined rules. This approach drastically reduces errors in high-volume operations such as invoice processing and account reconciliations, allowing teams to focus on strategic analysis. The immediate effect is a shift from routine tasks to value-driven activities.

By handling structured data from standardized forms or digital interfaces, RPA streamlines processes like KYC verification and compliance reporting. This technology part of a transformation where precision and efficiency replace manual interventions, ensuring consistent outcomes while lowering operational costs significantly.

What defines process automation in financial operations?

Process automation in finance refers to using software to handle repeatable, rule-based tasks that previously required manual effort. It’s designed for activities like data migration, transaction categorization, and report generation. The goal is to centralize and automate actions that are high-volume yet low-complexity, such as accounts payable workflows or regulatory filings.

By creating a system where predefined rules govern task execution, automation ensures accuracy across processes. For example, a bot might automatically match invoice details with purchase orders or flag anomalies in transaction logs, enabling teams to focus on exception handling rather than routine validation.

What distinguishes robotic process and intelligent automation in finance?

Robotic Process Automation (RPA) follows rigid, rule-based programming to replicate human interactions with financial systems, think of bots that extract data from structured templates or populate ERP fields. Intelligent Automation builds on this by adding AI capabilities. It understands unstructured data from documents or emails, learns from corrections, and makes context-aware decisions.

For instance, while RPA might struggle with varied invoice formats, intelligent automation adapts through machine learning. It interprets irregular layouts, connects data points across systems, and even suggests resolution pathways for discrepancies. This evolution transforms automation from task execution to cognitive problem-solving in financial workflows.

How does robotics redefine financial workflows?

Robotics in finance involves software bots that handle repetitive tasks with precision, from reconciling accounts to processing loan applications. These digital workers follow strict instructions to perform actions like data entry or payment routing, eliminating manual effort in standardized processes such as month-end closing or regulatory reporting.

By centralizing and automating data-intensive functions, robotics establishes a foundation for efficiency. A single bot might process hundreds of transactions in the time it takes a human to complete a handful, creating an immediate effect on throughput while maintaining audit-ready documentation for compliance purposes.

What are the core automation categories in banking?

Automation in finance spans four primary models: Basic Task Automation handles single-function actions like data extraction from forms. Process Automation coordinates multi-step workflows, such as end-to-end invoice processing. Cognitive Automation adds AI capabilities for unstructured data interpretation, like reading handwritten documents. Finally, Autonomous Decisioning systems make independent choices within defined parameters, such as approving low-risk loan applications.

These categories create a progression from simple task replacement to strategic decision-making. While early implementations focused on rule-based efficiency, modern financial institutions increasingly adopt cognitive and autonomous systems to handle complex scenarios like dynamic risk assessment or regulatory compliance monitoring.

What phases does process automation typically follow in finance?

Financial automation typically evolves through four stages: First, organizations identify repetitive tasks suitable for automation. Second, they implement rule-based RPA for high-volume activities like bank reconciliations. Third, they scale automation across departments while integrating with existing infrastructure.

The fourth stage involves enhancing systems with intelligent capabilities. At this point, automation systems begin handling exceptions autonomously, analyzing data patterns, adapting to format changes in financial documents, and making contextual decisions that previously required human intervention.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.