How can finance teams detect transaction anomalies before they impact cash or audits?

Published on :

March 23, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

Every financial anomaly that reaches an audit finding or a cash loss was, at some earlier point, a detectable signal in a transaction. An IBAN that changed three days before a wire was approved. An invoice amount that matched no purchase order in the system. A journal entry posted at 11:47 PM on the last day of the quarter by a user whose normal working hours end at 6:30 PM. A bank flow that arrived from an entity that has never transacted with the company before.

Each of these signals was present in the data. None of them were caught in time, not because the finance team was negligent, but because the transaction volumes, the number of systems involved, and the speed of financial flows made systematic real-time detection impossible without automation.

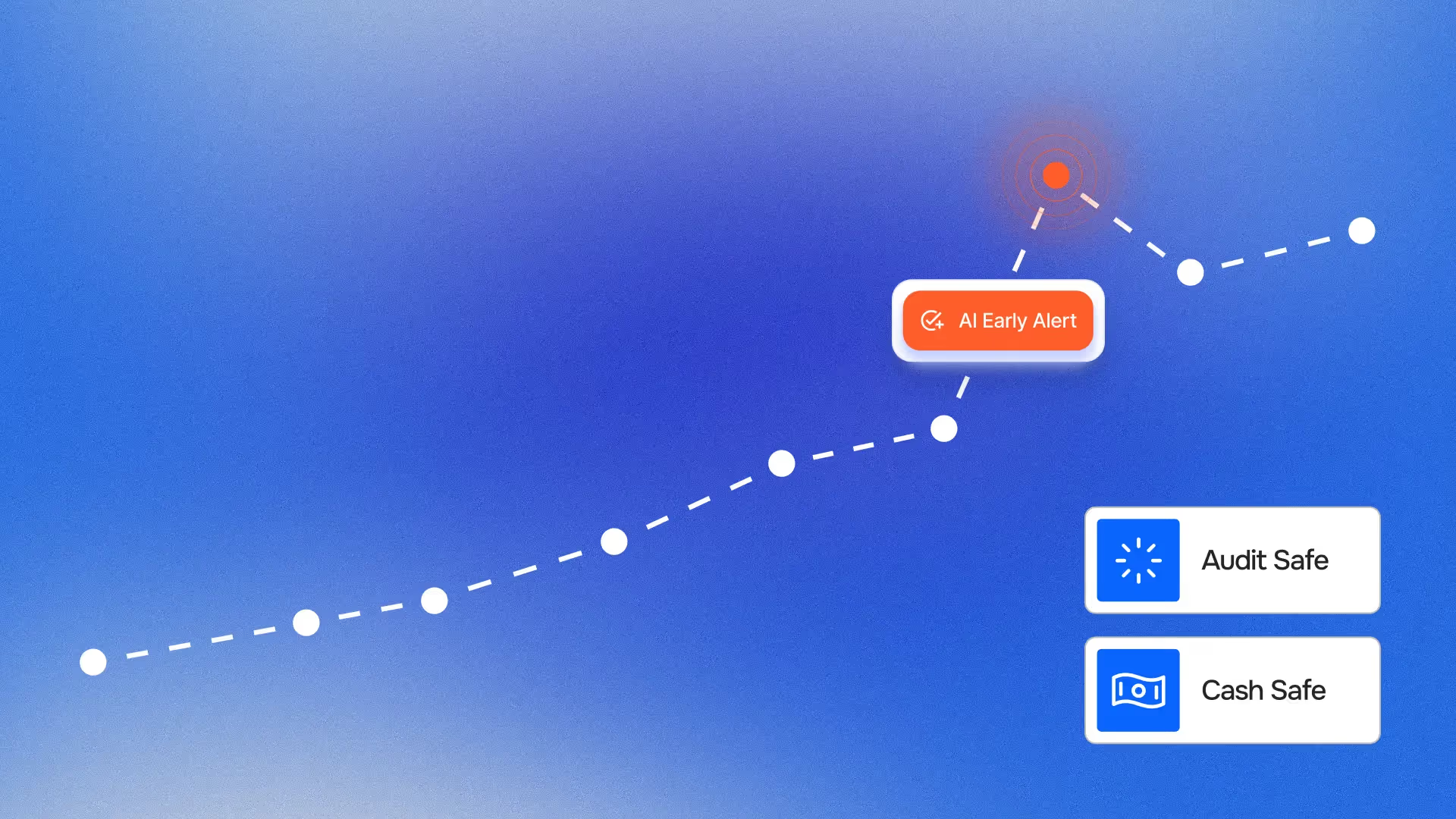

Financial anomaly detection AI, the application of machine learning and pattern-recognition to financial transaction streams, changes this constraint. It does not replace human judgment about whether an anomaly represents a genuine problem. What it does is ensure that the signals worth judging are surfaced before the payment clears, before the period closes, and before the auditor arrives. The window between signal and consequence is where AI detection creates its value: not by eliminating anomalies, but by shrinking the time between their occurrence and a human decision about them.

This article explains why rule-based detection systems fail at financial transaction scale, what AI adds that static threshold rules cannot provide, and how finance teams have deployed AI-powered anomaly detection to protect both cash position and audit readiness simultaneously.

Why rule-based detection fails at financial transaction scale

Most finance teams already have some form of anomaly detection in place. ERP systems flag invoices above approval thresholds. Bank platforms alert on transactions exceeding predefined amounts. AP workflows require dual approval for payments above a certain value. These rule-based controls are necessary, and insufficient.

Static rules cannot detect dynamic patterns

A rule that flags any invoice above €50,000 for additional review will catch the obvious outliers. It will not catch a supplier who increments their invoiced unit prices by 0.8% per month across a portfolio of low-value invoices, a pattern that produces €60,000 in annual overcharges without ever triggering a single threshold alert. The cumulative anomaly is real and financially significant; the individual transaction is invisible to any static rule.

Rule-based detection is effective for anomalies with known, fixed characteristics: amounts above a threshold, duplicate invoice numbers within the same entity, payments to blacklisted counterparties. It fails for anomalies that are defined by their deviation from a behavioural baseline, patterns that require knowledge of what "normal" looks like for a specific supplier, a specific GL account, a specific payment flow, and a specific period, before a deviation from that normal can be identified.

AI-powered anomaly detection builds and continuously updates these behavioural baselines from historical transaction data. What constitutes a normal invoice amount for Supplier X in the produce category in November differs from what constitutes normal in January. A machine learning model that has processed twelve months of billing data for that supplier knows this distinction. A static threshold rule does not.

The volume problem: humans cannot review everything

A multi-site organisation processing 2,000 invoices per month, receiving 500 bank transactions weekly, and posting several hundred journal entries per period faces a detection problem that human reviewers cannot solve through effort alone. Manual review at sufficient depth to catch pattern anomalies is simply not possible across transaction volumes of this magnitude, not without sampling, and sampling leaves most of the transaction population unreviewed.

AI detection operates on 100% of transactions simultaneously. It does not tire, does not sample, and does not apply different levels of attention to high-value versus low-value transactions. The pattern signal that exists in a sequence of €200 invoices from the same supplier across forty locations is as visible to an AI detection layer as the single €200,000 payment that a human reviewer would catch immediately.

The cross-system visibility gap

Financial anomalies rarely confine themselves to a single system. A fraudulent payment scheme may involve an invoice in the AP system, an IBAN change in the supplier master data, and a payment instruction in the bank platform, three events in three systems that only reveal their connection when viewed together. A journal entry anomaly may involve a GL posting, a bank transaction, and a period-end reconciliation record, again, across separate systems.

Rule-based detection that operates within a single system cannot identify anomalies whose signal is distributed across multiple systems. AI detection that aggregates data from invoice intake, bank flows, ERP postings, and supplier master data creates the cross-system view where these distributed signals become visible as connected patterns rather than isolated data points.

The dual cost of a missed financial anomaly: cash and audit

Financial anomalies that go undetected produce two distinct categories of consequence, each operating on a different timeline and requiring different remediation.

The cash consequence: immediate and often irrecoverable

The cash consequence of a missed anomaly is felt at the moment of payment. A fraudulent invoice that clears payment without triggering review has converted a billing anomaly into a cash loss. Recovering that loss, through supplier dispute, insurance claim, or legal process, is expensive, slow, and uncertain. According to PwC's Global Economic Crime and Fraud Survey, 46% of organisations reported experiencing fraud in the previous 24 months, with payment fraud consistently identified as the most common vector.

The cash consequence category includes:

- Payment fraud: altered IBAN details in supplier records or invoice documents, directing legitimate payments to fraudulent bank accounts. Detection must occur before the payment instruction is executed, which means before the invoice reaches the payment approval workflow.

- Duplicate payment: the same invoice paid twice, either within the same entity through process error or across entities through missing cross-entity controls. Each duplicate payment is a cash outflow that requires supplier negotiation and credit recovery.

- Overpayment from billing deviation: accumulated supplier overcharges that, once paid, are recoverable only through credit notes, and only if the overcharge is documented with sufficient precision to support a claim. Phacet's supplier billing control agent operates specifically at this pre-payment boundary, the last point where the cash consequence is still preventable rather than recoverable.

The audit consequence: delayed but structurally significant

The audit consequence of a missed anomaly operates on a longer timeline but produces structurally different damage. An anomaly that is not caught before payment may still be visible to an auditor months or years later, in an unexplained journal entry, a reconciliation break that was closed without documentation, a pattern of transactions that fall just below approval thresholds, or a supplier relationship that cannot be supported by business records.

The audit consequence category includes:

- Unexplained variance: transactions that produced P&L or balance sheet movements that cannot be traced to a business event with documentation. Auditors treat unexplained variance as a control weakness indicator regardless of the financial materiality of the individual item.

- Incomplete audit trail: payment approvals without the documentation chain that should accompany them, invoice, delivery confirmation, matching record, approval rationale. An audit trail gap is a control failure regardless of whether the underlying transaction was correct.

- Period-end anomalies: journal entries, adjustments, and reclassifications posted in the final days of a reporting period that lack the business justification documentation that characterises routine postings. These are the entries auditors examine most closely, because they are the most common vehicle for earnings management and misstatement.

AI-powered anomaly detection addresses both consequences simultaneously, by operating at pre-decision control points that prevent cash consequences, and by generating a complete, searchable audit trail of every transaction reviewed, every anomaly flagged, and every resolution outcome recorded.

What AI adds to financial anomaly detection: 4 capabilities rule-based systems cannot replicate

The value of AI in financial anomaly detection is not speed or scale alone, though both matter. It is four specific capabilities that static rule systems structurally cannot provide.

1. Behavioural baseline learning

AI detection builds a dynamic model of what normal looks like for each financial entity in the system: each supplier, each GL account, each payment destination, each user who posts journal entries. This model updates continuously as new transactions are processed, so that seasonal variation, growth-stage changes, and legitimate pricing evolution are incorporated into the baseline rather than generating false positives.

The result is anomaly detection that distinguishes between "this transaction is unusual for this supplier in this period" and "this transaction is simply different from the annual average". A supplier who doubles their invoice frequency during the holiday season is not exhibiting an anomaly, they are operating normally for that period. A supplier who doubles their invoice frequency in February, outside any seasonal pattern, is exhibiting a genuine deviation worth flagging.

2. Multi-dimensional pattern recognition

Each transaction has multiple attributes: amount, date, supplier, payment destination, GL account, posting user, entity, product category, currency. Rule-based systems typically monitor one or two of these attributes at a time. AI detection monitors all of them simultaneously, identifying anomalies that only exist in the combination, a transaction that is individually unremarkable on every single dimension but is anomalous in the combination of who posted it, when, to which account, and at what amount.

This multi-dimensional pattern recognition is what makes AI detection effective against sophisticated fraud schemes that are specifically designed to evade single-dimension threshold checks. A payment that is below the dual-approval threshold, from a supplier that has an established relationship, to a bank account that has received payments before, but posted by a user with no prior history of posting supplier payments, at an unusual hour, is invisible to any rule-based system monitoring these dimensions independently. AI detection that monitors the combination surfaces it as an anomaly worth reviewing.

3. Cross-entity and cross-system correlation

AI detection operates across the full transaction population simultaneously, all entities, all systems, all suppliers, all time periods. This cross-dimensional view enables the detection of patterns that are invisible within any individual slice of the data.

The bank reconciliation agent that Phacet deploys for multi-entity groups performs exactly this cross-system correlation, matching bank transaction records against invoice data and GL postings simultaneously, flagging flows that appear in one system but are absent or inconsistent in the others. An unmatched bank debit, a payment that left the account but corresponds to no approved invoice in the AP system, is a signal that requires immediate investigation regardless of its amount.

4. Explainable flagging with audit-ready rationale

This is the capability that distinguishes AI detection in finance from AI detection in other domains. A fraud detection model that outputs a probability score without explanation is operationally incomplete in a finance context. The finance team member who receives a flag needs to know why the transaction was flagged, which specific attributes deviated from which baseline, by how much, and with what frequency of prior occurrence, to make a rapid, well-informed resolution decision.

AI citation and explainability, the capacity of an AI system to provide transparent, traceable rationale for each detection output, is not optional in financial anomaly detection. It is the feature that makes detection output usable in an audit context. An auditor who asks why a transaction was flagged needs to receive a coherent, documented answer. An AI detection system that cannot provide that answer cannot support audit readiness regardless of its detection accuracy. Phacet's detection layer produces structured rationale for every flagged transaction, including the baseline parameters used, the magnitude of the deviation, and the historical frequency of similar patterns, creating an audit trail that is searchable, attributable, and auditor-ready.

The 5 transaction categories where AI detection delivers the highest return

AI-powered financial anomaly detection is most valuable in the transaction categories where pattern complexity exceeds what rule-based systems can handle and where the cost of missed anomalies, in cash or audit terms, is highest.

Supplier invoice flows

Invoice anomaly detection covers price compliance deviations, quantity mismatches, duplicate submissions, and pattern shifts in supplier billing behaviour. This category is the highest-frequency source of financial anomalies for product-purchasing businesses, and the category where the cumulative cost of undetected deviations is most significant. Jinchan Group's experience illustrates the scale: a 5x increase in anomaly detection rate when moving from manual spot-checking to systematic AI-powered validation across the full invoice population. The anomalies were not new, they had always been present in the billing data. What changed was the detection coverage. See the full Jinchan case study for the implementation detail.

For a comprehensive treatment of supplier invoice anomaly detection specifically, see our dedicated article on spend anomaly detection, which covers the five supplier billing anomaly categories in depth.

Bank transaction flows

Bank transaction anomaly detection identifies unmatched flows, timing anomalies, unexpected payment destinations, and patterns in cash movement that deviate from established operational baselines. This is the category where cash consequences are most immediate, a fraudulent outflow that clears the bank cannot be reversed through a credit note process.

Key anomaly types in bank transaction flows include:

- Unmatched outflows: payments that left the account but correspond to no approved invoice or payment instruction in the AP system. These may represent unauthorised payments, processing errors, or timing mismatches between the payment platform and the AP workflow.

- IBAN anomalies: changes to bank account details in the supplier master data within a short window before a payment run. This is the most common vector for payment fraud, the fraudulent bank change occurs just before the legitimate invoice is due for payment, capturing the payment into a controlled account.

- Frequency and timing patterns: a payment destination that receives payments at unusual frequency, at unusual hours, or in unusual amount patterns relative to its established relationship history with the entity.

La Nouvelle Garde's finance team encountered the practical reality of this category: a €28,000 payment almost reached a fraudulent account after a sophisticated IBAN-change phishing attempt. The anomaly was detected at the pre-payment validation stage by Phacet's accounting inbox automation, which flagged the IBAN change as an anomaly requiring human verification before the payment was approved. See the La Nouvelle Garde case study for the detection mechanism detail.

GL journal entry flows

Journal entry anomaly detection is the category most directly connected to audit exposure. Unusual GL postings, entries posted by unexpected users, at unexpected times, to unexpected account combinations, in unexpected amounts, are the transaction category that auditors examine most intensively, because they are the most common vehicle for concealing errors, misstatements, and deliberate manipulation.

AI detection applied to journal entry flows identifies:

- Off-hours postings: entries posted outside normal working hours for the user who posted them, particularly in the final days of a reporting period when period-end pressure provides legitimate cover for unusual activity.

- Account combination anomalies: debit-credit combinations that are unusual for the account types involved, a debit to revenue against a credit to cash that lacks the corresponding documentation chain expected for such an entry.

- Round-number patterns: concentrations of journal entries at amounts just below approval thresholds, or at suspiciously precise round amounts that are inconsistent with the transaction source they purport to record.

- Reversal patterns: recurring cycles of posting and reversal to the same account combination, which may indicate an account being used as a temporary parking location for transactions awaiting proper classification.

Supplier master data changes

Changes to supplier master data, bank account details, address, contact person, payment terms, are a transaction category that most anomaly detection systems do not monitor, because they are administrative events rather than financial transactions. But supplier master data changes are the upstream trigger for many downstream payment fraud events: the fraudulent bank account that receives a legitimate payment was entered into the master data at some earlier point, often by exploiting change management processes that lack systematic review.

AI detection applied to master data change logs identifies unusual change patterns: multiple changes to the same supplier record in a short window, changes made outside normal business hours, changes made by users who do not normally manage supplier relationships, and changes that precede scheduled payment runs for the affected supplier.

AI anomaly detection and audit readiness: the explainability requirement

The connection between AI anomaly detection and audit readiness is direct but depends on one critical capability: the AI system must produce detection rationale that is transparent, traceable, and documentable.

Why black-box detection fails the audit test

An AI model that flags a transaction as anomalous without explaining why is operationally limited in a finance context. The human reviewer who receives the flag cannot make a rapid, well-informed decision without knowing what anomaly pattern triggered it. More significantly, if the transaction is subsequently reviewed in an audit, the fact that "the system flagged it" is not an acceptable audit trail entry. The auditor needs to know what the system saw, what baseline it compared the transaction against, and what the specific deviation was.

AI citation and explainability, the structured output of detection rationale alongside each flag, transforms anomaly detection from a black-box alert system into an audit-ready control layer. Every flagged transaction carries a documented explanation: which parameters triggered the flag, what the baseline values were, what the transaction values were, and what the deviation magnitude was. This documentation is the audit evidence that an anomaly detection system was operating, functioning correctly, and generating rational outputs.

The human-in-the-loop review as audit documentation

The human-in-the-loop review step that follows each AI flag serves a dual purpose: it is the operational decision point where a human determines whether the flagged transaction requires action, and it is the audit documentation event where that decision, approve, dispute, escalate, or dismiss, is recorded with timestamp, reviewer identity, and rationale.

This review record is what makes the detection system auditor-ready. An internal auditor or external auditor examining the period's transaction population has access to: every transaction reviewed by the AI layer, every anomaly flagged with its detection rationale, every human review decision with its timestamp and reviewer, and every resolution outcome. This is the control environment documentation that demonstrates systematic, defensible financial oversight, not a manually assembled collection of email approvals and spreadsheet sign-offs.

Astotel's reduction of invoice error rates from 7% to 2% represents the direct outcome of systematic detection. But the audit trail generated by the detection and review process, documenting that 100% of invoices were processed through a consistent control sequence, is equally valuable to the finance function's audit preparation. See the Astotel case study for the implementation context.

Implementing AI financial anomaly detection: a practical sequence

Finance teams implementing AI-powered anomaly detection do not need to replace existing systems or undertake multi-year IT projects. The detection layer operates alongside existing ERP, bank, and AP infrastructure, processing transaction data from existing sources without requiring those sources to change.

Step 1 — Connect transaction data sources (weeks 1–2).

The AI detection layer connects to the accounting inbox for invoice data, to the bank platform or bank statement exports for transaction flows, and to ERP GL data for journal entry monitoring. Connection is via API or structured data export, no ERP modification required. Phacet's no-code automation interface allows finance teams to configure these connections without IT involvement.

Step 2 — Establish behavioural baselines (weeks 2–4).

The AI model processes historical transaction data, typically twelve months of invoice, bank, and GL history, to establish the behavioural baselines for each supplier, account, user, and payment destination. This baseline period is the foundation for all subsequent anomaly detection. The longer and cleaner the historical data, the faster the model converges on accurate baselines.

Step 3 — Configure detection sensitivity by transaction category (weeks 3–5).

Detection sensitivity thresholds are configured by transaction category, reflecting the different anomaly risk profiles of invoice flows, bank transactions, GL entries, and master data changes. High-frequency, low-value transaction categories (produce invoices, petty cash) may use broader tolerance parameters; high-risk, low-frequency categories (bank IBAN changes, period-end journal entries) use tighter parameters with immediate escalation protocols.

Step 4 — Operate the exception review workflow (from week 4).

The finance team reviews the exception queue generated by the AI detection layer, typically 3 to 5% of total transactions. Each exception includes the detection rationale, the specific transaction data, and the recommended action. Review decisions are recorded in the audit trail. The accounts payable automation and reconciliation workflows continue to operate as before; the AI detection layer adds a systematic review filter without changing the downstream processing workflow.

Step 5 — Iterate on detection quality (ongoing).

False positive rates and missed anomaly rates are monitored continuously. Detection parameters are adjusted based on observed outcomes, a supplier category that generates excessive false positives has its tolerance thresholds widened; a transaction type where confirmed anomalies are appearing below the current detection threshold has its sensitivity increased. The model improves with each billing cycle as the historical baseline grows.

FAQ

What is financial anomaly detection AI?

Financial anomaly detection AI refers to the application of machine learning and pattern-recognition algorithms to financial transaction data, invoices, bank flows, GL entries, supplier master data changes, to identify transactions that deviate from established behavioural patterns before they are processed as committed costs or approved payments. Unlike rule-based systems that flag transactions based on static threshold criteria, AI detection builds dynamic behavioural baselines from historical transaction data and identifies anomalies relative to those baselines, enabling detection of pattern-based fraud, systematic billing deviations, and operational errors that fixed rules cannot capture.

How does AI anomaly detection differ from traditional fraud detection tools?

Traditional fraud detection tools in finance typically operate on rule-based logic: flagging transactions above threshold amounts, blocking payments to blacklisted counterparties, or requiring dual approval for specific transaction types. AI anomaly detection operates on behavioural pattern analysis: identifying transactions that deviate from the established normal pattern for their specific transaction type, supplier, account, user, or entity, regardless of whether they exceed any predefined threshold. The practical difference is that AI detection catches pattern-based anomalies that rule-based systems miss by design, while generating the explainable rationale that finance and audit teams need to act on each flag.

What financial transaction categories benefit most from AI anomaly detection?

The four highest-value categories for AI anomaly detection are supplier invoice flows (price compliance, quantity, duplicates, billing pattern shifts), bank transaction flows (unmatched outflows, IBAN anomalies, timing and frequency patterns), GL journal entry flows (off-hours postings, unusual account combinations, round-number patterns, reversal cycles), and supplier master data changes (bank detail changes, contact changes ahead of payment runs). Of these, supplier invoice flows offer the highest frequency and cumulative financial impact; bank transaction flows offer the highest per-incident cash exposure; GL entry flows carry the highest audit exposure.

Can AI anomaly detection work across multiple ERP systems?Yes. AI anomaly detection that operates at the data layer, processing transaction records from multiple sources, does not require ERP uniformity. The detection layer ingests data from each ERP instance, bank platform, and AP system separately, normalises it into a consistent analytical format, and applies detection across the unified dataset. This cross-system approach is particularly valuable for multi-entity groups where different subsidiaries run different ERP environments, because it creates group-level anomaly visibility that individual ERP instances cannot provide.

How does AI anomaly detection support audit preparation?

AI anomaly detection supports audit preparation in three ways. First, it provides evidence that 100% of transactions were processed through a systematic control sequence, demonstrating the completeness of financial oversight that auditors assess as part of control environment evaluation. Second, it generates a searchable, timestamped record of every flagged transaction, its detection rationale, the reviewer's decision, and the resolution outcome, the audit trail that makes the control process auditable. Third, it reduces the unexplained variance that auditors treat as control weakness indicators, by catching and resolving anomalous transactions before they close into the period accounts without documentation.

What is the difference between AI financial anomaly detection and spend anomaly detection?

Spend anomaly detection focuses specifically on the supplier purchasing and invoice flow, identifying billing deviations, quantity mismatches, and pricing non-compliance in the accounts payable process. Financial anomaly detection AI is the broader capability: it encompasses spend anomalies as one category alongside bank transaction anomalies, GL journal entry anomalies, and master data anomalies. The distinction matters for implementation scope: spend anomaly detection requires supplier reference data and invoice intake connection; full financial anomaly detection additionally requires bank transaction data and GL access. Most organisations implement spend anomaly detection first, then extend to broader financial transaction coverage.

How long does it take for AI anomaly detection to become accurate?

AI anomaly detection reaches meaningful accuracy within the first two to four weeks of live operation, as the model processes real incoming transactions against the historical baseline established in the setup phase. Initial false positive rates are typically higher than steady-state rates, the model is still learning the operational nuances of each supplier relationship and transaction category. By week four to six of live operation, most deployments have reached false positive rates below 5%, meaning more than 95% of flagged transactions represent genuine anomalies warranting review. Accuracy continues to improve over successive billing cycles as the historical baseline grows.

How does explainability work in AI financial anomaly detection?

Explainability in AI financial anomaly detection means that each flagged transaction is accompanied by a structured explanation of what triggered the flag, which specific transaction attributes deviated from which baseline values, by what magnitude, and with what historical frequency of prior occurrence. This explanation is generated automatically alongside the flag, providing the human reviewer with the context needed for a rapid, well-informed decision. The explanation is also recorded in the audit trail, creating the documentation that audit teams need to verify that the detection system was operating rationally and that each flagged transaction received appropriate human review.

Detection at the signal, not at the consequence

Every financial anomaly that reaches an audit finding began as a transaction-level signal. The question is not whether the signal was there, it always is. The question is whether the detection infrastructure was in place to surface it before the payment cleared, before the period closed, and before the external auditor arrived.

AI-powered financial anomaly detection is the infrastructure that closes this gap. Not by replacing human judgment about what each anomaly means, but by ensuring that human judgment is applied to every signal that warrants it, at the moment when action is still possible, with the context needed to decide quickly, and with the documentation trail that makes every decision audit-ready.

The companies that manage financial control most effectively at scale have built this infrastructure at the transaction layer, not as a reporting overlay that catches anomalies after they compound, but as a real-time detection layer that surfaces signals before their consequences become irreversible. Book a demo to see how Phacet deploys AI financial anomaly detection across your transaction flows, and what your current financial data reveals when every transaction is analysed, not sampled.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.