How companies prevent supplier overpayments without relying on invoice sampling

Published on :

February 23, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

Supplier overpayments are not rare events. They are a predictable consequence of a control method, invoice sampling, that was never designed to catch systematic billing errors at scale. The average company overpays between 0.5% and 1.5% of its total supplier spend annually, according to accounts payable benchmarks. For a business with €10M in supplier purchases, that range translates to €50,000 to €150,000 leaving the door every year, invoice by invoice, undetected.

The standard response, sample 10–20% of invoices, review them manually, extrapolate conclusions, works well enough when invoice volumes are manageable and supplier relationships are stable. It stops working the moment volumes grow, suppliers multiply, or pricing agreements become complex. At that point, sampling does not reduce overpayments. It reduces the visibility of overpayments while they continue to accumulate.

This article explains why sampling fails as a prevention strategy, what the structural causes of supplier overpayments actually are, and how companies replace sample-based review with systematic controls that work on 100% of invoices before any payment is approved.

Why invoice sampling is an overpayment strategy, not a prevention strategy

Sampling feels like a control. In practice, it is a prioritization mechanism, a way of deciding which invoices to check when checking all of them seems impossible. The fundamental problem is that the invoices most likely to contain errors are not randomly distributed. They concentrate in specific patterns: high-frequency suppliers, recently renegotiated contracts, invoices submitted by new billing contacts, multi-entity documents routed across shared supplier bases.

Random or systematic sampling at 10–20% coverage misses most of these patterns. A supplier billing 2% above negotiated rates on every invoice will pass undetected through a 20% sample in most cycles, not because the sample was poorly chosen, but because the error appears consistently across all documents rather than randomly in a subset.

The math is unforgiving. A company processing 400 invoices per month at 20% sampling reviews 80 invoices and leaves 320 unchecked. If 5% of invoices carry pricing discrepancies, 16 errors pass through every month, 192 per year. Not because anyone failed to do their job. Because the method structurally cannot catch what it does not examine.

Accounts payable automation built around systematic pre-payment validation replaces this structural gap with 100% coverage, applied before, not after, payment approval.

The four structural causes of supplier overpayments

Preventing overpayments requires understanding where they come from. They are not random. They follow consistent, predictable patterns that systematic controls are designed to intercept.

Price drift against negotiated contracts

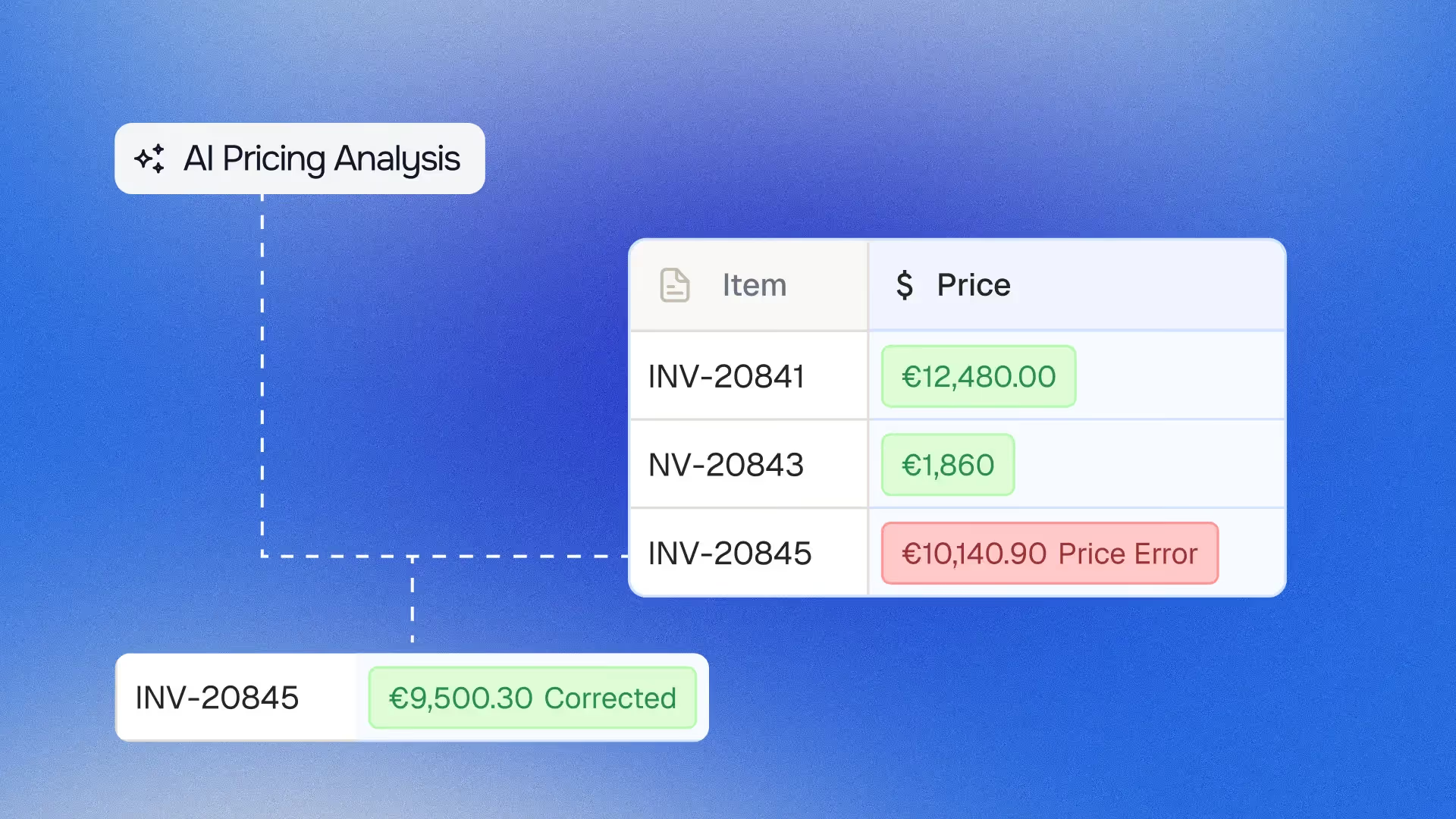

This is the most financially significant and most underdiagnosed source of overpayments. Procurement negotiates pricing agreements, catalog rates, volume discounts, framework contracts. Suppliers invoice against those agreements. Over time, small discrepancies accumulate: a unit price updated in the supplier's billing system but not reflected in the contract, a promotional rate that expired but continued to be applied in reverse, a rounding convention that consistently favors the supplier by fractions of a percent.

No single invoice reveals the pattern. The overpayment only becomes visible when invoice data is systematically compared to the applicable contract version at line-item level, across all invoices, in every billing cycle.

Vivason identified and stopped exactly this pattern. Before deploying systematic price compliance controls, billing drift across its supplier base was absorbing €180,000 annually in undetected overpayments. The invoices were not obviously wrong, they were subtly wrong, consistently, across hundreds of lines. Spot-checking caught occasional outliers. Systematic comparison at 100% coverage caught the drift.

The supplier billing control agent Phacet provides runs this comparison automatically, cross-referencing every invoice line against the applicable contract or catalog before payment approval.

Duplicate invoice submissions

Duplicate invoices are among the most commonly cited causes of accounts payable overpayments, and among the most preventable. They occur in predictable circumstances: a supplier re-sends an unpaid invoice with a modified reference, the same document is received across multiple inboxes in a group structure, or an invoice submitted during a system migration is reprocessed in the new environment.

The challenge is detection range. A duplicate submitted in the same week is easy to catch manually. A duplicate submitted 47 days after the original, with a reference number incremented by one digit and a slightly different date format, passes most manual review processes, especially under month-end pressure.

Systematic duplicate detection runs cross-checks across the full invoice history on configurable parameters: supplier, amount range, invoice reference variants, and date windows. It catches what periodic manual review misses because it does not depend on reviewer memory or available time.

Quantity and delivery variances

Invoices reflect what suppliers claim was delivered. Delivery records reflect what was actually received. When these two documents tell different stories, overbilled quantities, invoiced items not included in the delivery, services billed for periods outside the contract term, the difference becomes an overpayment if no systematic check reconciles them before payment.

Three-way matching is the standard control for this scenario: reconciling the purchase order, delivery note, and invoice before any payment proceeds. Jinchan Group, a multi-brand F&B operator, multiplied its anomaly detection rate by 5x after automating this process. The anomalies had always existed, they were simply invisible because manual matching covered only a fraction of incoming documents.

For a detailed breakdown of how automated 3-way matching works at scale, see our article on AI-powered 3-way matching and payment traceability.

Multi-entity routing errors

In group structures operating multiple legal entities, holding companies with subsidiaries, restaurant groups with individual locations, retail chains across sites, invoices frequently arrive in a shared inbox and require routing to the correct entity before ERP entry.

When routing is manual, allocation errors generate their own overpayment dynamic: an invoice charged to the wrong entity is paid by the wrong cost center, the correct entity may pay the same invoice again when the supplier follows up, and month-end consolidation becomes unreliable because entity-level costs are structurally misstated. Systematic entity validation at intake eliminates this class of error before it reaches the ERP.

What systematic prevention looks like in practice

Replacing invoice sampling with systematic overpayment prevention requires repositioning the control checkpoint. The current model, review what you can find time for, post-ERP, during month-end close, needs to shift to a model where every invoice passes through a defined set of controls before it enters the ERP and before payment approval is triggered.

The practical architecture has four components working in sequence.

Automated intake and extraction. Every incoming supplier document, regardless of format, channel, or originating entity, is captured and structured in real time. OCR extraction produces machine-readable invoice data: supplier identity, line items, unit prices, quantities, dates, banking details. This structured data is what all subsequent controls operate on.

Rule-based validation against reference data. The extracted data is compared to the applicable reference set: negotiated price lists, active contracts, purchase orders, delivery records. This comparison runs on 100% of documents, applying the same rules consistently, without the fatigue and attention variance that affects manual review. Discrepancies above defined thresholds generate flags; clean documents proceed automatically.

Exception-based human review. The finance team does not review clean invoices, the system validates them automatically. Human attention goes to flagged documents: the invoice where the unit price is 3.2% above the contracted rate, the duplicate reference submitted from a new contact, the delivery quantity that doesn't match the PO. Phacet clients typically achieve 95%+ automatic validation rates, with fewer than 5% of documents requiring human decision.

Full audit traceability. Every validation decision is logged: which rule applied, what the outcome was, whether a flag was raised, who reviewed it and what they decided. This trace matters for CAC audits, internal governance, and the post-incident analysis that follows any overpayment that does slip through. Explore what a complete audit trail looks like in practice on Phacet's platform.

This is the architecture that moves finance teams from reactive recovery, finding overpayments in audit, negotiating credit notes weeks after payment, to preventive control. The pre-decision control moment is before payment approval, not after.

The compounding cost of delayed detection

The financial case for systematic prevention is stronger than the headline overpayment figures suggest, because overpayment costs compound over time in ways that invoice-level analysis understates.

Recovery costs are high. Identifying an overpayment after payment requires contacting the supplier, documenting the discrepancy, negotiating a credit note, and tracking its application against future invoices. Finance teams report 2–4 hours of recovery work per identified overpayment. At 192 undetected errors annually, the figure for a 400-invoice-per-month company at 20% sampling and 5% error rate, the recovery overhead reaches 400–800 hours per year, before accounting for the working capital cost of funds that have already left the business.

Fraud recovery is almost impossible. When an overpayment results from a fraudulent IBAN change or a fabricated invoice rather than a billing error, the recovery timeline extends from weeks to months, and the funds may not be recoverable at all. Prevention, in these cases, is not just more efficient than recovery, it is the only financially viable option.

Reporting distortion persists until correction. Every overpayment that enters the ERP degrades the accuracy of cost reporting, margin analysis, and budget variance until the correction is processed. The downstream cost of unreliable data, decisions made on distorted figures, is difficult to quantify but real.

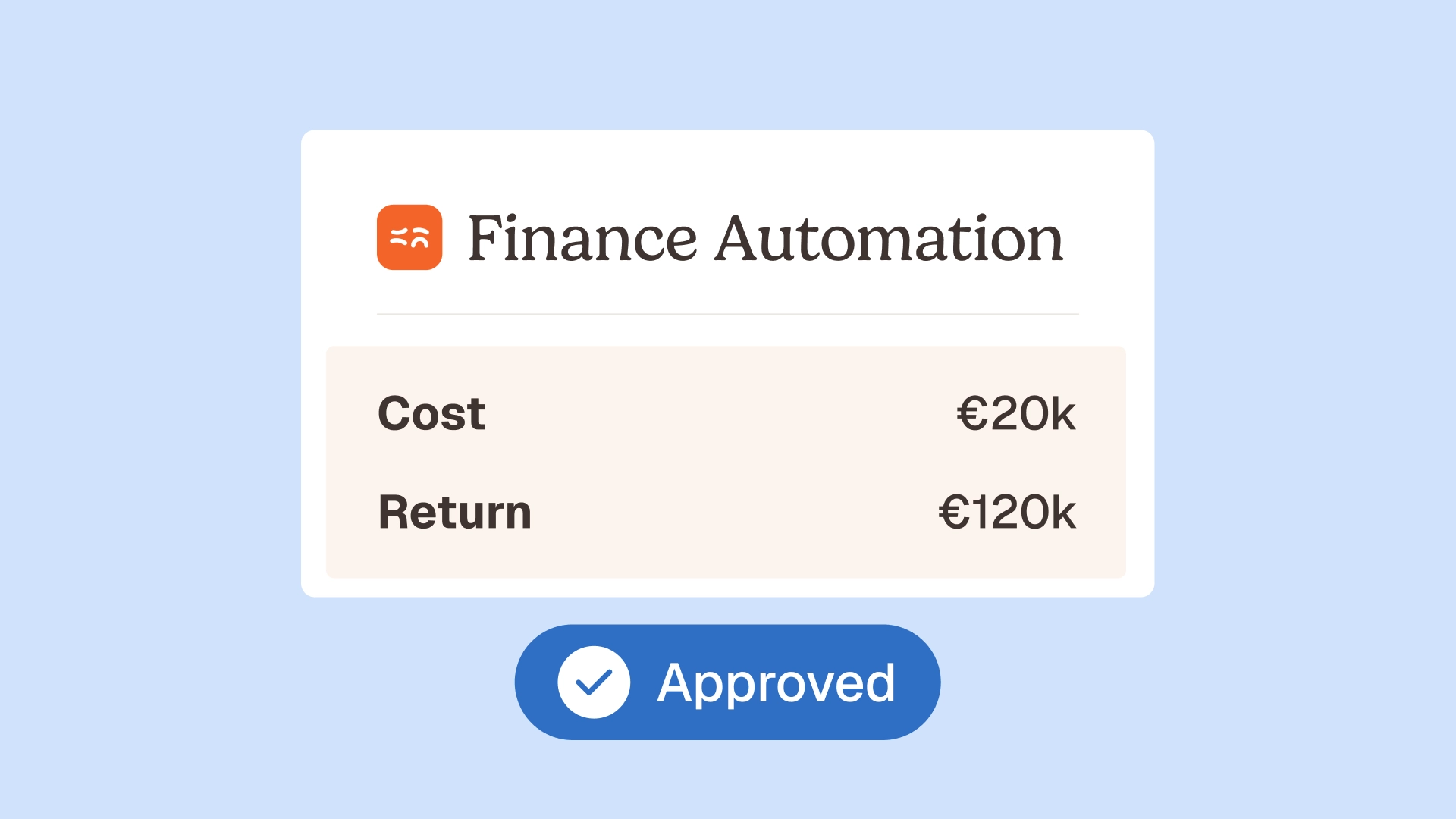

The ROI of AI in finance calculation for systematic overpayment prevention therefore includes three figures: the direct overpayment amount prevented, the recovery cost avoided, and the improvement in reporting reliability. Most Phacet deployments reach payback within four months on the direct prevention figure alone.

Phacet in practice: from sampling to systematic prevention

Phacet's platform acts as the control layer that sits between supplier document receipt and ERP entry. For each Phacet client that has moved from sample-based review to systematic prevention, the transition follows a consistent pattern.

Week 1–2: Intake configuration.

The platform connects to the accounting inbox, maps the supplier base, and imports applicable reference data, contracts, catalog prices, purchase orders. Entity routing rules are configured for multi-entity environments.

Week 2–4: Calibration.

Validation rules are tuned against live invoice data. Price tolerance thresholds, duplicate detection windows, and approval escalation amounts are adjusted based on real traffic. Validation accuracy reaches 95%+ within the calibration period.

Ongoing: Exception operations.

The team reviews only flagged documents, typically fewer than 5% of total volume, with full context for each flag. Every document reviewed or auto-validated is logged in the audit trail.

Astotel, a multi-property hotel group, moved through this transition and reduced its invoice error rate from 7% to 2% while covering 100% of incoming documents rather than the sampled subset it had relied on previously. The Astotel case study details the implementation and outcomes.

The French Bastards, a fast-growing bakery chain, deployed Phacet's inbox validation as it scaled from 7 to 14 locations, absorbing doubled invoice volume without doubling finance headcount. The French Bastards case study covers how systematic controls made that growth trajectory financially manageable.

For teams earlier in evaluating their options, Phacet's AI agents overview maps the specific agents available for supplier billing control, invoice reconciliation, and accounts payable automation.

FAQ

What causes supplier overpayments?

The four primary causes are price drift against negotiated contracts, duplicate invoice submissions, quantity and delivery variances between invoices and delivery records, and multi-entity routing errors that result in the same document being paid by the wrong entity or paid twice. These causes are systematic, they repeat across billing cycles, which is why point-in-time sampling fails to control them reliably.

Why doesn't invoice sampling prevent overpayments?

Sampling reviews a subset of invoices and extrapolates conclusions to the rest. But overpayments caused by systematic pricing errors or consistent billing patterns are not randomly distributed, they appear on every invoice from a specific supplier or in a specific category. A 20% sample will miss 80% of those errors, not by chance but by design. Sampling is a triage tool, not a prevention tool.

How does 100% invoice validation work at scale?

Automated validation applies rule-based checks to every incoming invoice as it arrives, before it enters the ERP. The system compares invoice data against reference data, contracts, catalogs, POs, delivery records, and flags discrepancies automatically. Clean invoices pass through without human intervention. Flagged invoices go to a reviewer queue with full context. This model scales to any invoice volume without proportional increases in review time.

What's the difference between preventing overpayments and recovering them?

Prevention intercepts an overpayment before payment is made, a billing discrepancy is flagged, the payment is held, the supplier is contacted for correction. Recovery happens after payment has been made, an overpayment is identified, a credit note is requested, funds are reconciled against future invoices. Prevention costs almost nothing beyond the validation system. Recovery costs 2–4 hours per incident, takes weeks to complete, and does not recoup the working capital cost of funds already advanced.

Which types of companies are most exposed to supplier overpayments?

Exposure is highest in companies with large supplier bases, complex pricing agreements, high invoice volumes, multi-entity structures, and rapid growth that outpaces finance team capacity. Growth-stage companies in food service, retail, distribution, and hospitality consistently appear in this profile, high transaction volumes, thin margins where overpayments are materially significant, and supplier relationships where billing complexity is high.

How quickly can systematic overpayment prevention be implemented?

Most Phacet deployments are operationally live within 2–4 weeks. The first week covers intake connection and supplier data import. The second and third weeks calibrate validation rules against real invoice data. By the end of the calibration period, the system achieves 95%+ automatic validation accuracy. The first prevented overpayments typically surface within the first billing cycle after go-live.

Can overpayment prevention integrate with existing ERP workflows?

Yes. Phacet sits upstream of the ERP, validated invoices are routed to the correct ERP (Pennylane, Sage, Odoo, and others) with pre-filled, clean data. The ERP continues to manage payment runs and accounting records. The prevention layer ensures that what it receives has already been checked, so ERP-level controls operate on data that has already passed a systematic validation step.

What happens when the validation system identifies a potential overpayment?

The flagged invoice enters a review queue with the specific discrepancy identified: the invoice unit price, the contracted rate, the variance amount, and the rule that triggered the flag. The reviewer can approve the exception, reject the invoice, or request a corrected document from the supplier, all logged in the audit trail. This exception-based model means finance teams spend their review time on actual discrepancies, not on confirming that clean invoices are clean.

The question sampling cannot answer

Invoice sampling answers a reasonable question: "Of the invoices I reviewed, how many had errors?" It cannot answer the question that actually matters: "Of all the invoices I paid this month, how many were correct?"

That second question requires systematic control, a process that checks every invoice against every applicable rule before every payment. Not because finance teams are incapable of catching errors manually, but because the volume, frequency, and pattern-dependence of supplier billing errors make systematic automation the only method that consistently works at scale.

Vivason's €180,000. Astotel's error rate cut from 7% to 2%. Jinchan's 5x detection improvement. These outcomes share a single structural shift: validation moved from periodic and sampled to systematic and pre-payment.

The companies that prevent supplier overpayments at scale are not the ones that sample more carefully. They are the ones that stopped sampling altogether. Book a demo to see how Phacet's systematic validation works against your invoice volumes and supplier structure.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.