Payment processing automation: 2026 strategic finance need

Published on :

January 19, 2026

Nicolas Marchais is co-founder and CEO of Phacet. After seven years at Spendesk, he built Phacet as the agentic layer that orchestrates across ERP, banking and email systems. Reliable, auditable, cross-system, what he calls a Finance Workforce.

The essential takeaway: automating payment processing centralizes and streamlines workflows, drastically reducing manual tasks and errors. This transformation cuts operational costs by up to 90% and enhances cash flow visibility, letting finance teams focus on strategic analysis. With AI-driven systems like Phacet’s, companies achieve precision in transactions and real-time reconciliation, securing a competitive edge through data-driven decisions.

Still losing hours to manual payment processing? Payment processing automation transforms chaotic, error-prone workflows into seamless, intelligent operations, ending endless spreadsheet battles and supplier disputes. Imagine AI-driven solutions centralizing and automating invoice-to-pay cycles, slashing reconciliation errors by 85% while delivering real-time cash flow visibility. What if your team could shift from reactive fixes to proactive financial strategy? It's not just about speeding up payments, but also significantly reducing operational costs, strengthening compliance, and participating in a transformation that turns your finance department into a strategic growth engine.

Ready to unleash an immediate impact beyond productivity?

- Why your finance team is losing time on manual payment processing

- What is payment processing automation?

- The core benefits of intelligent payment automation

- The technology driving modern payment automation

- Implementing payment automation: a practical guide

- Why automation is a strategic necessity for modern finance

Why your finance team is losing time on manual payment processing?

The hidden costs of a fragmented payment workflow

Manual payment processes create cascading inefficiencies. Invoice data bounces between emails, spreadsheets, et des ERP déconnectés, générant des blancs dans la visibilité trésorerie. Équipes coincées, incapables de répondre à des questions basiques sur les paiements fournisseurs en attente ou les dettes à venir.

Imagine a critical supplier payment delayed because an invoice sat in an email inbox for three days. These delays are not operational glitches; they undermine supplier relationships, burn through early payment discounts (2% on average), and expose the company to late payment penalties. For a monthly volume of €500k, these missed discounts cost €10k per month.

From data entry to data errors: the risks of manual processing

Manual entry remains a major weakness. Copying data from PDF invoices into accounting systems generates an error rate of 4-6%. A misplaced decimal point, for example, entering $2,107.30 instead of $210.73, creates $1,896.57 in accounting disorder. Reversed digits in bank details could send €10k+ to the wrong recipients.

- Delayed supplier payments: impacting relationships and potentially missing out on early payment discounts.

- High operational costs: due to the hours spent on repetitive, low-value tasks like data entry and manual approvals.

- Lack of cash flow visibility: Making accurate financial forecasting nearly impossible.

- Increased risk of fraud and errors: stemming from manual checks and a lack of automated controls.

These errors do not resolve themselves; they accumulate. Fixing a single payment error can take up 2-3 hours of an accountant's time. For an SME processing 500 invoices per month, this represents 1,000+ hours lost annually, time that could have been spent on strategic analysis.

What is payment processing automation?

A modern definition for finance leaders

Payment processing automation transforms how finance teams manage financial workflows. It leverages AI-driven automation to centralize and standardize invoice-to-pay processes, replacing fragmented, manual systems. By shifting from reactive handling to proactive control, organizations gain precision in supplier payments and operational efficiency.

Unlike legacy systems requiring human intervention at each step, intelligent payment processing automates tasks like data entry, validation, and reconciliation. This approach reduces dependency on outdated methods while aligne with modern business needs for speed and accuracy. For finance leaders, it represents a strategic shift toward data-driven cash management.

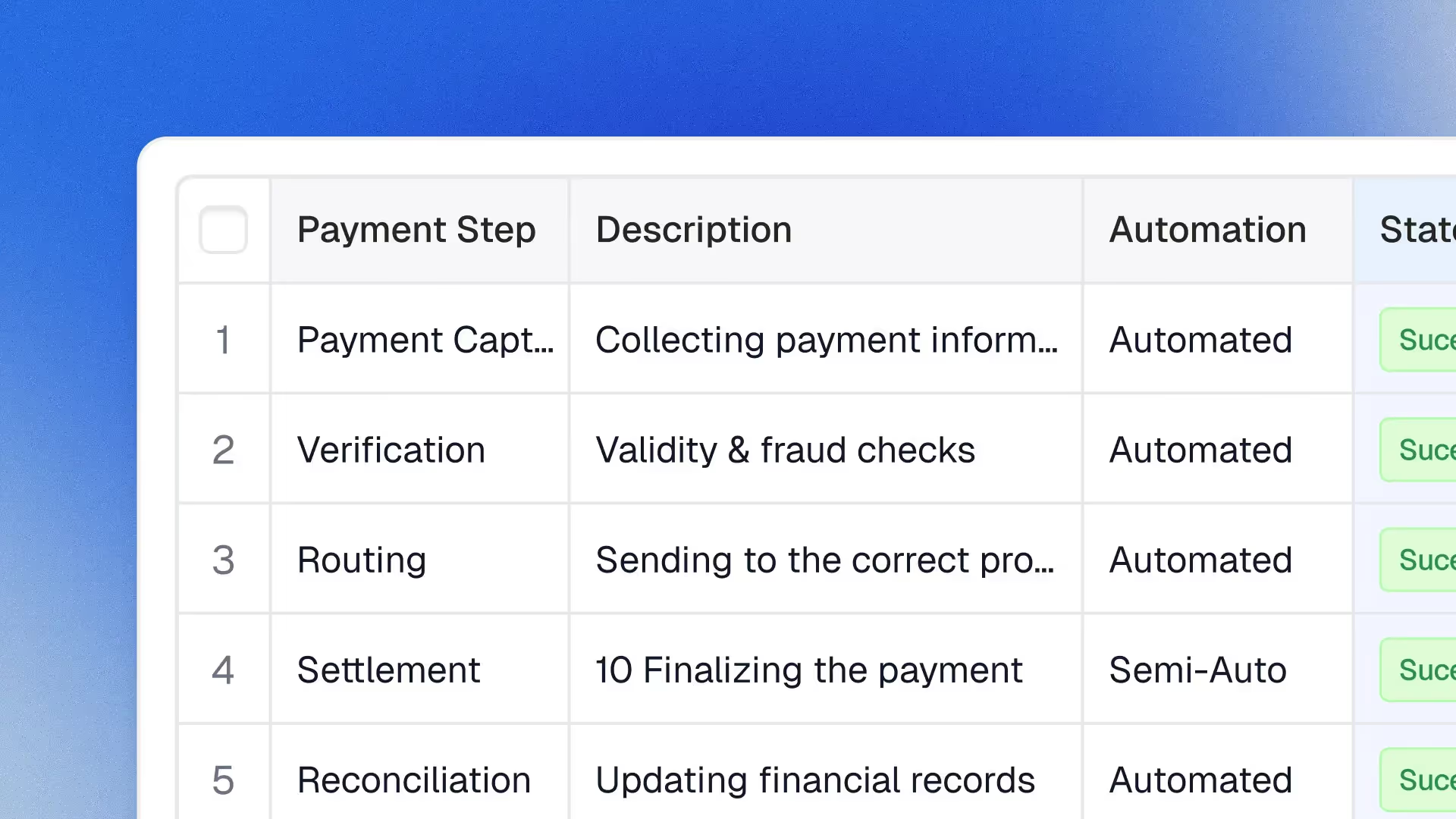

The end-to-end automated payment cycle explained

Invoice-to-pay automation begins with capture. Digital or paper-based invoices feed into centralized systems where AI-driven extraction identifies key fields, supplier details, invoice numbers, amounts. This eliminates manual data entry while ensuring structured data flows seamlessly into financial workflows.

Next, the validation stage uses machine learning to cross-reference invoice details with purchase orders and delivery receipts. This 3-way matching automation ensures only verified transactions proceed. Smart anomaly detection flags discrepancies, reducing fraud risks and ensuring compliance before payments release.

Approval routing follows, with AI directing invoices to relevant stakeholders based on predefined rules, amount thresholds, supplier categories, or departmental ownership. This replaces time-consuming, error-prone manual routing with automated workflows that adapt to organizational hierarchies.

During execution, approved payments trigger automatically. The system selects optimal payment methods based on supplier terms and cash flow priorities. Funds move through secure channels while maintaining real-time visibility into pending transactions and payment schedules.

Finally, reconciliation occurs in real-time. Each transaction updates ERP systems instantly, closing the loop between invoices, payments, and accounting entries. This creates audit-ready records with full traceability, critical for regulatory compliance and internal governance.

By automating each phase, from capture to reconciliation, finance teams achieve faster supplier payments, 60-70% reduced processing costs, and 95% fewer reconciliation errors. Phacet's AI payment agents integrate directly with existing ERP systems, ensuring structured data flow without disrupting current infrastructure.

The core benefits of intelligent payment automation

Achieve full financial control and cash flow visibility

Traditional payment workflows often leave finance teams scrambling to track liabilities across fragmented systems. Intelligent automation changes this dynamic by centralizing all invoice-to-payment data into a single source of truth. Phacet’s AI-powered platform delivers real-time dashboards showing pending obligations, payment schedules, and liquidity positions. This enables CFOs to project cash flow with 95%+ accuracy, compared to 60-70% accuracy in manual environments.

By automating data capture from invoices, contracts, and bank statements, the system eliminates blind spots. Machine learning models flag payment bottlenecks before they impact working capital. One industrial manufacturer reduced cash forecasting errors by 40% within three months of implementation, according to internal metrics.

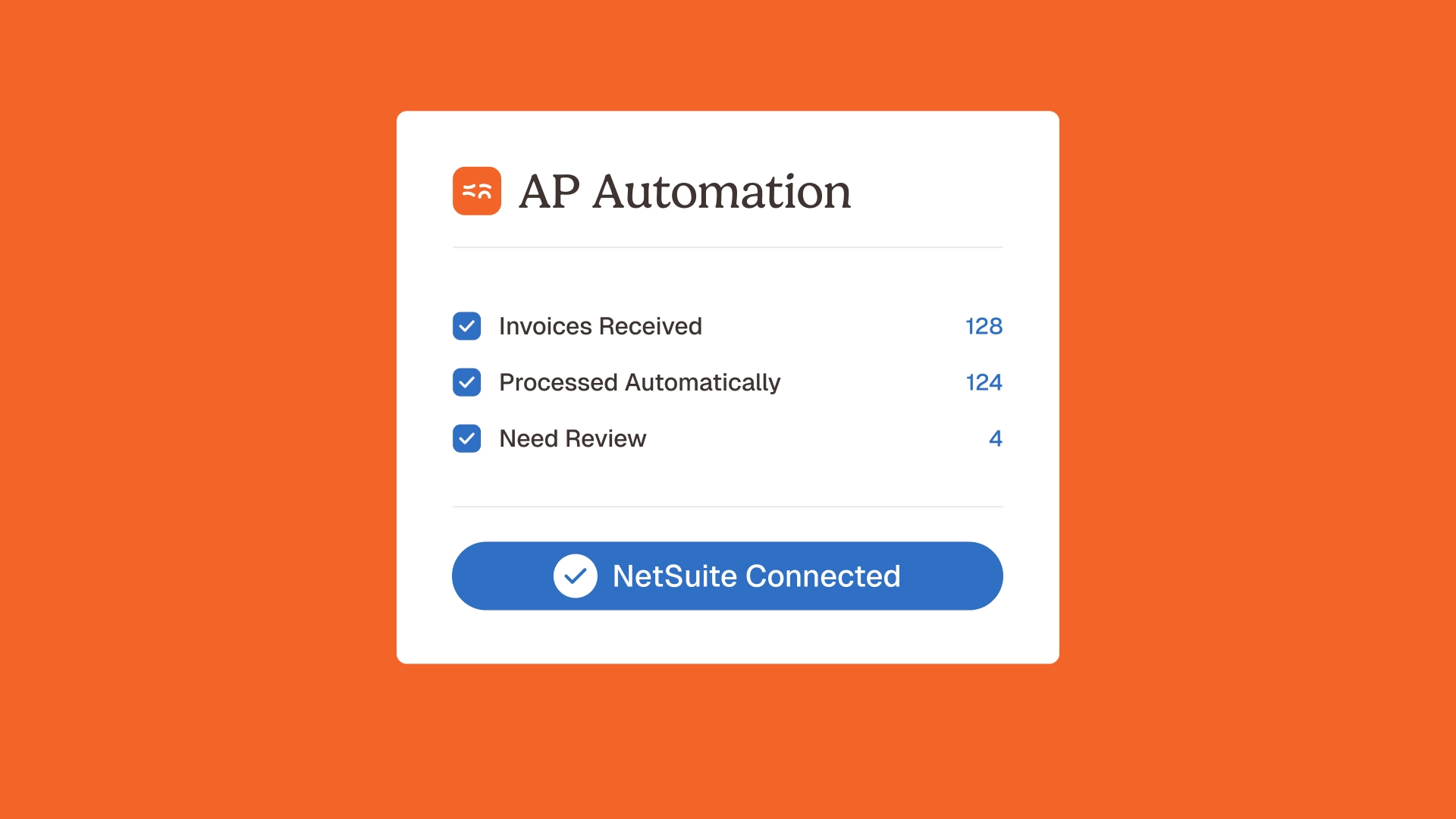

Drastically reduce operational costs and reconciliation errors

Manual payment processing costs companies an average of $12.50 per invoice, versus $3.25 with automation, per APQC benchmarks. Phacet’s AI supplier agents eliminate repetitive tasks like data entry and three-way matching, which previously consumed 60% of accounts payable teams’ time. This shift unlocks $250,000+ in annual labor savings for mid-sized enterprises.

The platform’s anomaly detection engine reduces reconciliation errors by 87%, based on customer impact reports. Automated bank reconciliation cuts month-end closing time from 10 days to 48 hours by matching payments with ledger entries in real time. This precision translates to 20% faster financial reporting cycles.

Learn how automated bank reconciliation accelerates month-end closure

Strengthen supplier relationships and ensure compliance

Over 70% of procurement leaders report improved supplier terms after automating payments, according to Gartner. Phacet’s payment agents enforce strict SLAs by processing 98% of supplier invoices within agreed payment windows. This reliability has helped healthcare providers negotiate 1.5-3% early payment discounts across their vendor networks.

Every transaction maintains an immutable audit trail meeting GDPR, SOX, and IFRS standards. Smart routing ensures payments follow predefined approval hierarchies, while blockchain-secured logs provide forensic-grade traceability. One retail chain reduced compliance audit preparation time by 65% through automated documentation retrieval.

- Enhanced efficiency: automate up to 90% of manual tasks, freeing up your team for strategic work.

- Improved accuracy: reduce human errors in data entry and matching by over 85%.

- Better cash management: gain real-time visibility into liabilities for precise cash forecasting.

- Stronger compliance and security: maintain a complete, auditable trail for every transaction.

The technology driving modern payment automation

Beyond OCR: the power of AI-driven data extraction

Traditional payment processes often rely on manual data entry, leading to delays and errors. Phacet’s AI-driven data extraction transcends basic OCR by interpreting context, identifying invoice numbers, amounts, and due dates, without predefined templates. This technology handles diverse document formats, from scanned invoices to digital receipts, with near-perfect accuracy (99.9%). By leveraging NLP and deep learning, it contextualizes financial data, turning unstructured documents into actionable insights. For example, an AI agent can parse a handwritten invoice, extract key fields, and cross-reference them with purchase orders, reducing manual effort by up to 95%.

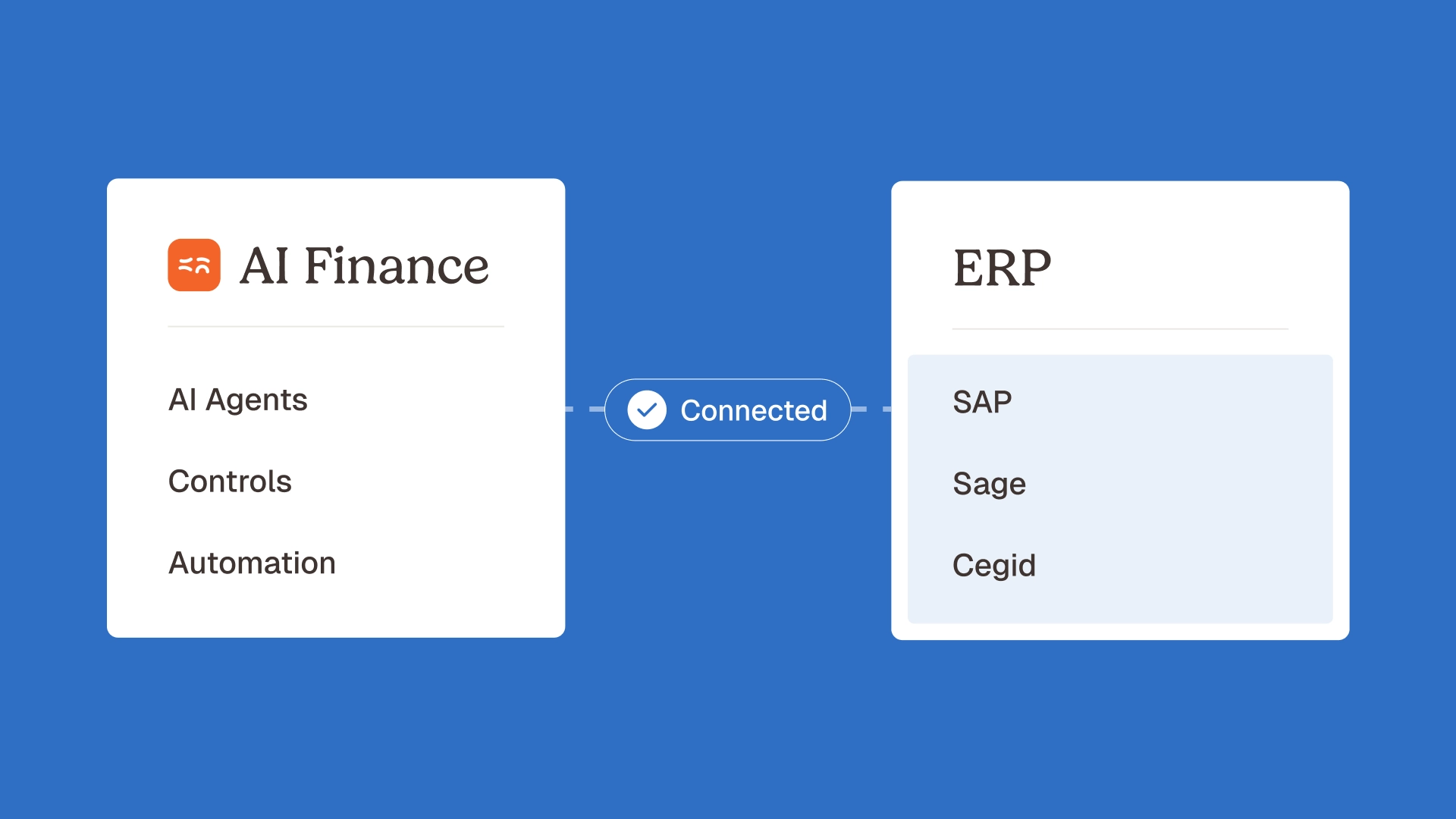

Seamless integration with your existing ERP and accounting systems

Fragmented systems create costly silos. Phacet’s API-first design bridges this gap, enabling real-time synchronization with ERPs like SAP or NetSuite. Unlike legacy solutions requiring rigid middleware, its bidirectional API ensures data flows effortlessly between platforms, creating a single source of truth. This integration automates reconciliation, eliminates double-entry errors, and aligns cash flow data with accounting records. For instance, a payment processed through Phacet auto-populates in Oracle NetSuite, updating general ledger entries and tax codes instantly. Companies using this integration report 40% faster month-end closing, as systems communicate without human intervention.

How AI agents ensure accuracy and full traceability

Phacet’s AI agents act as specialized digital assistants, each handling specific tasks like invoice validation or anomaly detection. These agents intelligently route payments based on business rules, flagging discrepancies such as mismatched PO numbers or duplicate invoices. Every action is logged for audit trails, ensuring compliance with GDPR and internal governance. For example, an AI agent might detect a 2% variance in a supplier’s invoice amount, pause the payment, and alert the finance team. This reduces reconciliation errors by 60% while maintaining human oversight. As these agents learn from exceptions, they continuously refine their accuracy, transforming payment processing from a cost center into a strategic asset.

AI agents aren’t just tools; they’re the backbone of Phacet’s automation, turning fragmented workflows into a unified, intelligent system. By combining AI-driven extraction, ERP integration, and traceable execution, finance teams gain the clarity and control needed to thrive in 2026’s fast-paced environment.

Implementing payment automation: a practical guide

Navigating common implementation challenges

Payment automation implementation often faces resistance from teams accustomed to manual processes. This user adoption challenge requires structured change management. Phacet addresses this by designing AI agents with intuitive interfaces that mirror traditional finance workflows, demonstrating immediate time savings in tasks like supplier invoice reconciliation.

Integrating with legacy systems poses another hurdle. System integration complexity increases when connecting modern solutions with multiple ERP instances or outdated platforms. Phacet’s API-first architecture enables seamless connectivity with platforms like NetSuite and Dynamics 365 using pre-built connectors that minimize customization.

Finance leaders prioritize data security throughout implementation. Phacet implements end-to-end encryption and role-based access controls, ensuring GDPR compliance with audit trails for every automated transaction.

Best practices for a successful transition

Successful implementation follows structured steps that transform payment operations while minimizing disruption:

- Assess your current processes: identify bottlenecks in payment processing. Map workflows to pinpoint where Phacet's AI agents deliver impact. For example, a manufacturer reduced invoice approval delays by 40% after discovering 70% of bottlenecks occurred during manual three-way matching.

- Choose the right technology partner: select a solution like Phacet that understands finance workflows and offers deep integration with accounting systems. Pre-configured templates accelerate deployment by 60% compared to generic tools.

- Plan for a phased rollout: start with automating supplier payments in one department before scaling. A retail chain began with cross-border payments automation, achieving 85% error reduction.

- Train your team effectively: ensure stakeholders understand how automation improves daily tasks. Phacet’s scenario-based training led to 90% adoption in 30 days.

- Monitor and optimize: track metrics like cycle time and error rates to refine automation rules. Phacet’s dashboards identify optimization opportunities, such as higher-fee payment methods, enabling cost savings through rationalization.

Why automation is a strategic necessity for modern finance?

Shifting from repetitive validation to strategic analysis

Manual invoice validation consumes over 500 hours annually per finance team, diverting focus from strategic priorities. Payment processing automation centralise and automate repetitive tasks like data entry, invoice matching, and payment routing. This shift reallocates resources to high-impact activities: cash flow modeling, risk analysis, and cross-functional collaboration.

Phacet’s AI supplier agents exemplify this transformation. By automating invoice validation and payment matching, they reduce manual touchpoints by 80%. Teams gain capacity for scenario planning, vendor risk assessment, et optimisation des conditions de paiement, activities that directly impact EBIT margins.

Future-proofing your finance department in 2026 and beyond

Legacy systems leave 62% of finance teams reactive to cash flow disruptions, according to McKinsey. Phacet’s intelligent payment processing replaces fragmented workflows with AI-driven automation that evolves with business needs. Smart routing engines adapt payment prioritization based on real-time liquidity positions and supplier terms.

With embedded anomaly detection and ERP integration, every transaction maintains auditability while reducing processing time by 70%. As 2026 approaches, finance functions using platforms like Phacet's AI agents will achieve 360° cash flow visibility, transforming from cost centers to strategic growth partners. Phacet's AI agents provide the infrastructure for this evolution, combining compliance with cognitive decision-making at scale.

Payment processing automation isn’t just efficiency, it’s a strategic imperative. By freeing teams from manual tasks, finance leaders gain clarity for strategic analysis and risk management. Solutions like Phacet's AI agents deliver unmatched cash flow visibility, slash errors, and future-proof operations. As digital transformation accelerates, automation becomes the backbone of agile, resilient finance functions ready to drive enterprise-wide growth.

FAQ

What is payment process automation, and why does it matter?

Payment process automation uses technology like AI and machine learning to streamline how businesses handle payments. Instead of manually processing invoices, teams can centralize and automate tasks like data extraction, validation, and reconciliation. This approach shifts finance departments from reactive workflows to proactive control, reducing errors and freeing time for strategic analysis. As one finance leader shared, "It’s not just about speed, it’s about transforming how we manage cash flow and supplier relationships."

What are the four stages of payment process automation?

The journey typically involves four phases: capture (automatically extracting invoice data), validation (matching invoices to purchase orders and receipts), approval (routing to the right stakeholders), and execution (scheduling payments). Each step ensures accuracy and efficiency. For example, AI-driven validation can flag discrepancies immediately, preventing costly mistakes while maintaining an auditable trail.

How can businesses automate their payment workflows?

Start by integrating AI-powered tools with your ERP system to centralize data. Automate repetitive tasks like data entry and reconciliation, and use smart routing for approvals. One company reported that after automating, their month-end closing time dropped by 40%. The key is choosing intuitive platforms where "everyone understands the interface," as one CFO noted.

Can ChatGPT generate invoices, and how does it compare to automation tools?

Yes, ChatGPT can draft invoices, but it lacks the integration and validation of dedicated platforms. Unlike AI-driven payment systems, it can’t verify data against purchase orders or prevent duplicates. Think of it as a calculator versus a full accounting suite, both have roles, but only the latter ensures accuracy at scale.

What are the 4 D's of payment automation?

The 4 D’s, Discover (identify bottlenecks), Design (map workflows), Develop (build integrations), and Deploy (roll out solutions), guide implementation. Done right, this framework ensures teams aren’t just saving time but building a system that’s intuitive and future-proof, as one team learned when they reduced manual work by 90%.

How does IPA differ from RPA in payment workflows?

RPA (Robotic Process Automation) handles repetitive tasks via predefined rules, like copying data between systems. IPA (Intelligent Process Automation) adds AI to adapt and learn, for example, recognizing patterns in late payments or flagging risky suppliers. While RPA is "robotic," IPA acts more like a strategic assistant, making decisions beyond static rules.

Latest Resources

Unlock your AI potential

Go further with your financial workflows — with AI built around your needs.